In an extract from March’s edition of the Preqin Infrastructure Spotlight, Stephen Yates examines the latest data on African infrastructure, including deal flow, notable deals in recent years and the growing number of investors targeting investment in Africa.

Preqin’s Infrastructure Deals feature on Infrastructure Online includes extensive information on almost 11,000 completed transactions in infrastructure assets globally. These deals involve a variety of investors, ranging from infrastructure fund managers and direct institutional investors to industry players such as developers, contractors and other industry-specific trade investors. In excess of 7,200 transactions have been completed since 2007, with an estimated deal value well over $1.5tn. Within this space, the African market has until recently remained relatively untouched, representing under 3% of the total number of deals completed since 2007. However, the need for new infrastructure in this area has become apparent in recent years, and with competition for assets growing in the traditional markets of Europe, North America and Asia, investors have begun seeking investment opportunities within emerging markets, namely Africa.

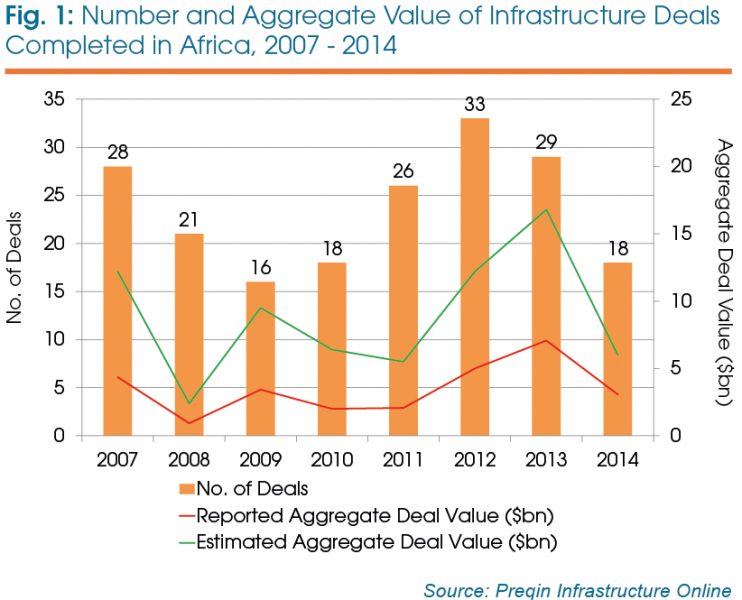

Number and size of deals

As a result, the last few years have witnessed an increase in the annual number and estimated aggregate value of deals completed within the African infrastructure market. As shown in Fig. 1, the annual number of completed African deals declined to its lowest point in 2009 of 16, at an estimated aggregate deal value of $9.5bn. Preqin’s estimated deal value is calculated using the total reported value of all deals where this is known, along with estimates for deals where a deal size has not been disclosed. 2012 and 2013, however, witnessed an improvement in the market, with the estimated aggregate deal value reaching a peak in 2013 of $17bn from 29 completed transactions. Although only 18 transactions have been recorded for 2014, at an estimated deal value of $6bn, this number is expected to grow substantially in the next 12 months as more deals come to light.

Average deal size has shifted in recent years, with infrastructure deals becoming larger. In 2011, deals valued at less than $100mn accounted for the majority of transactions completed, representing 57% of all completed deals in that year, with only 7% of deals being valued above $500mn in the same year. However, transactions completed with a value above $500mn have grown in significance, representing 31% of completed Africa-based deals in 2014, compared to just 7% in 2011.

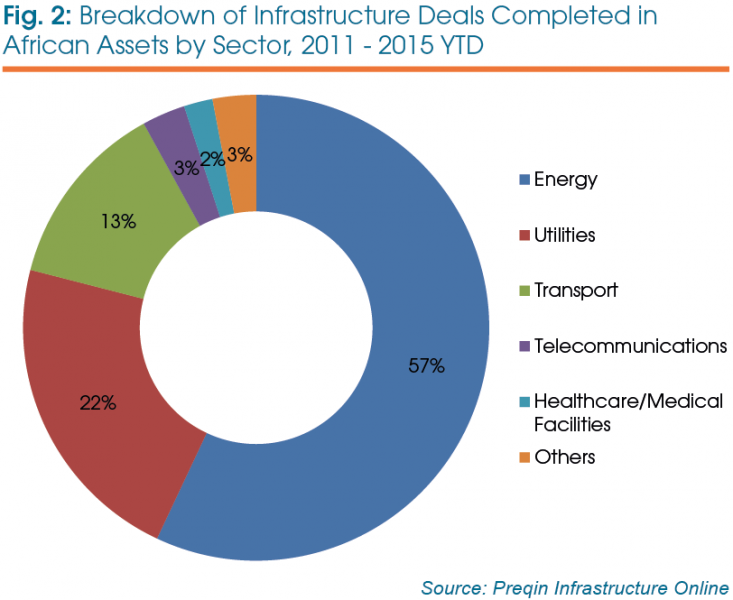

Location and industry

The largest proportion of Africa-based infrastructure deals take place in South Africa, which represents 34% of Africa-based transactions between 2011 and 2015 YTD, followed by Morocco (7%). Cameroon and Nigeria each account for 6% of transactions during the same period, with Uganda and Ghana accounting for a further 5% apiece.

In terms of specific industry, energy assets are the most prominent, representing 57% of Africa-based infrastructure deals completed since 2011, as shown in Fig. 2. Utilities is the next most prominent industry, with such assets accounting for 22% of all Africa-based transactions during the same period, followed by transport (13%), telecommunications (3%) and healthcare/medical facilities (2%).

African infrastructure market

Several notable deals have taken place within Africa in the last 12 months. In South Africa, a consortium including Abengoa, Industrial Development Corporation and Public Investment Corporation acquired Xina Solar Power Plant, a 100 MW concentrating solar power project located in Pofadder, in a deal worth $908mn. Other notable deals include the acquisition of Nigeria-based Azura-Edo IPP, a 450MW Independent Power Plant facility being developed near Benin City in Edo state, by a large consortium of investors including African Infrastructure Investment Managers, Aldwych International, Amaya Capital Partners, American Capital Energy & Infrastructure and ARM-Harith Infrastructure Investments.

With African deal flow improving significantly in recent years, it is perhaps unsurprising that the current African fundraising market remains healthy. The largest Africa-focused fund in market is Pan African Infrastructure Development Fund II, which is looking to raise $1.2bn to acquire Africa-based infrastructure projects in the telecommunications, energy, transport, water and sanitation sectors. If the fund successfully reaches its target size, it would be the second largest Africa-focused vehicle of all time, behind Abraaj Infrastructure and Growth Capital Fund, which closed in December 2007 having attracted a significant $2bn in institutional commitments. Other prominent Africa-focused funds on the road include COMESA Infrastructure Fund, managed by PTA Bank, which targets investment in trade-related infrastructure projects within COMESA member states.

This article is an extract from the Preqin Infrastructure Spotlight | March 2015.

Click here to read the full Spotlight newsletter for free, or visit our Research Center for more information.