Fund performance and industry dry powder is analysed in this extract from the Preqin Quarterly Update: Private Debt, Q3 2015.

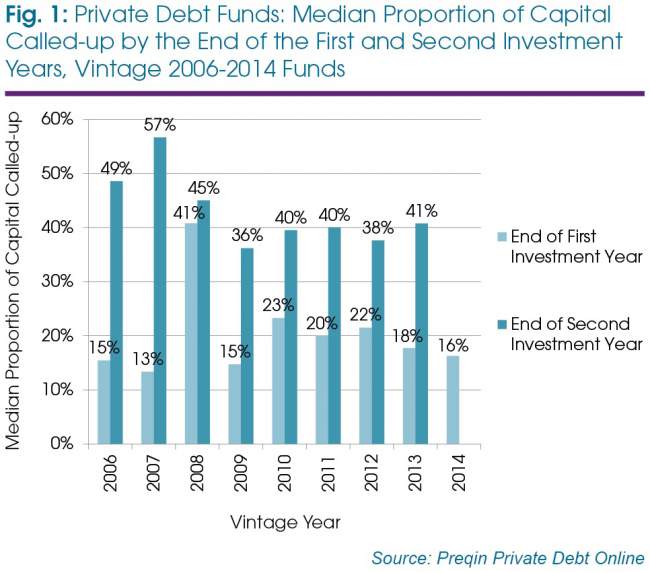

Fig 1 displays the median proportions of committed capital called up by the end of the first and second investment years, among all private debt funds for vintage years 2006-2014. It shows that post-2008, the median proportion of capital called up during the first two years of investment is lower than before the financial crisis. This could be explained by recent fundraising success pushing up dry powder levels at a faster rate than available deals in a competitive marketplace. Dry powder now stands at a record USD191 billion, up 37 per cent since December 2014, which may place pressure on fund managers to put this capital to work.

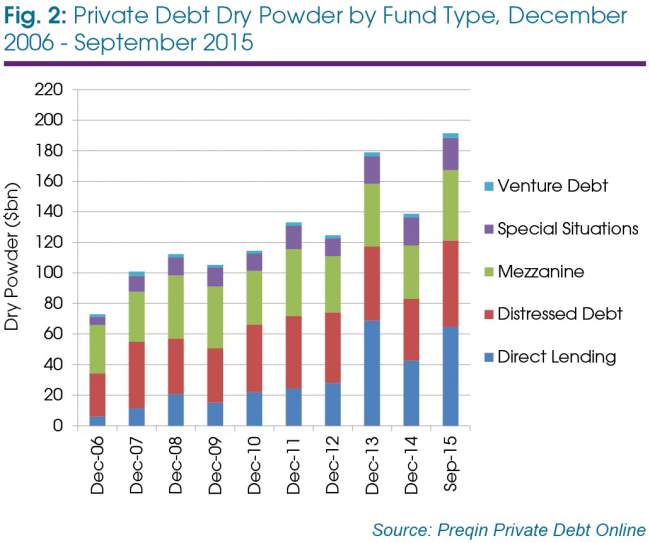

As shown in Fig 2, direct lending funds account for the largest proportion of dry powder at USD65 billion, up 52 per cent since December 2014. Distressed debt funds have also witnessed a notable increase in the amount of dry powder available to them, with the figure currently standing at USD56 billion, while mezzanine funds hold USD46 billion.

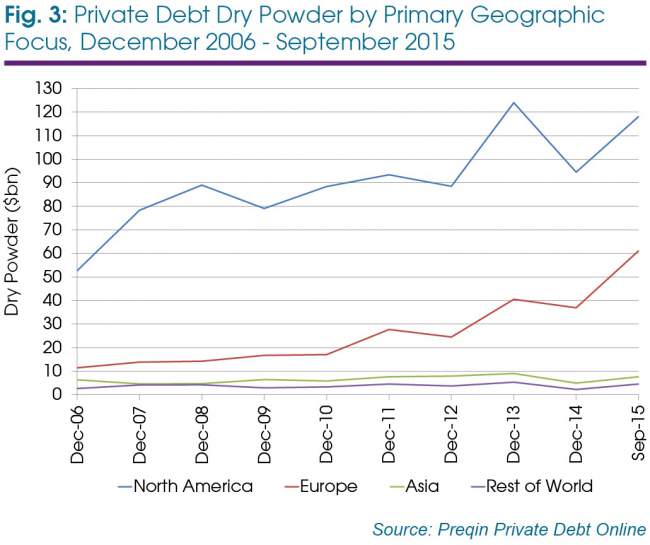

Europe-focused private debt funds have seen dry powder increase by 66 per cent since December 2014 to reach USD61 billion (Fig 3). Dry powder available to North America-focused funds currently stands at USD118 billion, an increase of 25 per cent compared to December 2014.

This article is an extract from the Preqin Quarterly Update: Private Debt, Q3 2015, one of five quarterly editions that also cover private equity, hedge funds, real estate, infrastructure and private debt. Download all of the reports for free by visiting our website.