New Hedgeweek® data reveals allocator wariness as hedge funds chase private market opportunities beyond their core expertise.

As more and more hedge funds rush headlong into private markets, a Hedgeweek® survey of 100 institutional allocators reveals considerable unease about the pivot, with nearly two-thirds expressing negative or neutral views about managers expanding beyond their core competencies.

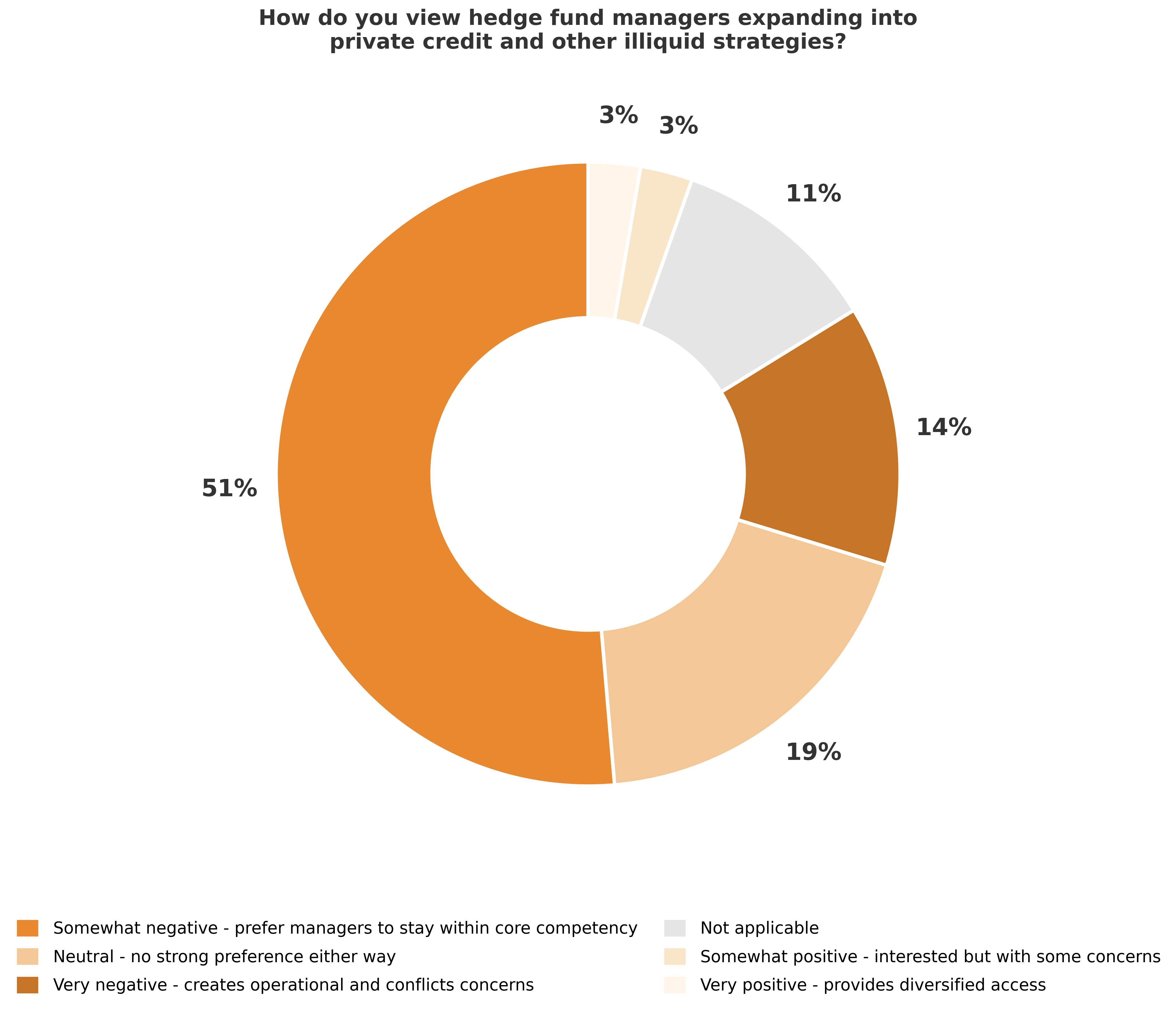

The data, collected in the second half of 2025, shows that 51% of allocators are “somewhat negative” about hedge fund managers entering private credit and other illiquid strategies, preferring them to remain within their established expertise. A further 14% hold “very negative” views, citing operational complexities and potential conflicts of interest. Only 5% view the trend positively.

The scepticism comes as some of the industry’s most prominent names – including Steve Cohen’s Point72 Asset Management, Izzy Englander’s Millennium Management, and Bobby Jain’s Jain Global – announce plans to raise billions for private credit and illiquid strategies. Point72 is in preliminary discussions to raise at least $1bn for a private credit fund, whilst Millennium is targeting $5bn for its first private markets vehicle.

The appeal is clear. Global hedge fund assets have reached a record $5tn, but capacity constraints at the largest firms have forced some to cap inflows or return capital. Meanwhile, private markets have expanded dramatically as the number of US-listed companies has halved since 2000, whilst private, venture capital-backed companies have increased 25-fold. Private credit assets under management have surged following the 2008 financial crisis, as credit activity migrated from banks to buy-side investors.

Yet allocators’ reservations appear well-founded. The skill sets that produce alpha in liquid markets – speed, relative-value analysis, derivatives expertise – do not necessarily translate to the relationship-intensive, patient capital approach required in private lending. “Private credit is a fundamentally different business,” Bruno Schneller, managing partner at Erlen Capital Management, told Bloomberg.

The structural challenges are formidable. Direct lending returns increasingly depend on access to cheap leverage, which requires scale, diversification and longevity that new entrants lack.

Recent setbacks underscore the risks. Millennium’s team led by Sean O’Sullivan took an approximately $100m writedown on First Brands Group, whilst UBS liquidated two funds run by its O’Connor hedge fund unit following private credit losses.

Hedgeweek® anticipates further diversification attempts, following the path blazed by DE Shaw – which has raised over $5bn in private credit since 2008 – and established crossover managers such as Diameter Capital Partners and GoldenTree. Several sizeable players are reportedly preparing similar moves, attracted by longer lock-ups, cross-selling opportunities and potential valuation benefits ahead of succession planning.

However, the allocator data suggests a more cautious reception than managers might expect. With 19% remaining neutral, the industry appears to be adopting a wait-and-see approach, mindful that not every expansion will succeed.

The real test, as Schneller told Bloomberg, will be “cultural and operational” – whether these firms can adapt their incentive systems and decision processes to markets where returns are realised over years, not quarters. For allocators, the preference remains clear: stick to what you know best.

For the full analysis of allocator sentiment in H1 2026, Hedgeweek will launch a comprehensive report in collaboration with AIMA in January 2026.