PARTNER CONTENT

By Arnab Banerjee PhD, and Robert D Stock PhD, Axioma Analytics Solutions, SimCorp

A critical assumption in typical equity factor risk models is that the specific returns – the parts left over after fitting to a linear factor model – are uncorrelated, resulting in a diagonal specific covariance matrix. But this is not strictly true, and there is value in understanding the systematic structure hiding in specific returns.

Crisis creates clusters, not convergence

We investigated whether transient, thematic “crisis” factors arise by analyzing ten different major market disruptions. What our research revealed is that by harnessing residual-probing methods, it is indeed possible to identify transient factors in periods of market stress.

The usual description of a crisis is that “correlations go to one” and everything moves down together. If that were truly the case, we’d expect to see clusters of companies with correlated residuals growing in size, and the number of separate uncorrelated clusters dropping as everything merges together.

Evidently that is an oversimplification, because we actually observed the number of correlated-residual clusters increasing in this study.

Why does this happen?

Our hypothesis is that during a thematic crisis, different groups of stocks still behave somewhat differently, but within those groups affected by the thematic factors, the specific correlations rise (as expected), producing more linkages and creating more short-term clusters. It appears a strong crisis produces a multitude of transient factors in which the differentiations between somewhat-similar companies get erased in the minds of investors, but these separate groups still behave differently from each other. Hence, many new small clusters appear on a short-term basis. (Specific volatility could also rise in a crisis, but that is not hidden by the diagonal matrix assumption).

Detecting transient patterns

For this research, we developed a modified approach of an existing Axioma risk model method, Comparable Company Specific Covariance (CCSC). This uses Agglomerative Hierarchical Clustering on the specific return correlations to find companies (within the same industries) with highly-similar business models. The standard CCSC method adds off-diagonal terms to the specific covariance matrix for all pairs within each cluster. Clustering stops when elements become further away than implied by an absolute specific return correlation of less than about 0.5.

CCSC is designed for stability to operate within a broader risk model framework, by using, for example, a three-year trailing data window, and updating no more frequently than quarterly. By design, it may be unable to detect mild, short-term effects. Therefore, for this study, we modified the approach so that CCSC could be made more responsive to detect and characterize transient, thematic crisis factors.

The methodology

This meant shortening the correlation-computation window from three years to three months, and computing it weekly instead of quarterly. We picked ten crisis periods: 9/11, WorldCom, Subprime, Lehman, US Credit, Brexit, COVID, Ukraine, SVB, and Liberation Day. We also picked four random “control” periods where the market was flat or up. We then computed our CCSC clusters at T = [-4, -2, -1, 0, +1, +2, +4, +6] weeks around the event using the residuals from our global short-horizon model, and looked for some signal. Examining various measures of cluster size and strength, the most robust signal was the number of clusters. Our signal is therefore the maximum peak-to-previous-trough percentage change in the number of clusters observed over the ten-week period around the event.

Now, not every crisis will necessarily produce transient factors. Some could be explained perfectly well by heightened volatility (and/or correlation) in the normal style factors. Also, transient thematic factors aren’t necessarily only appearing in a crisis; they could be contributing to bullish (but narrow) market advances as well.

Key findings

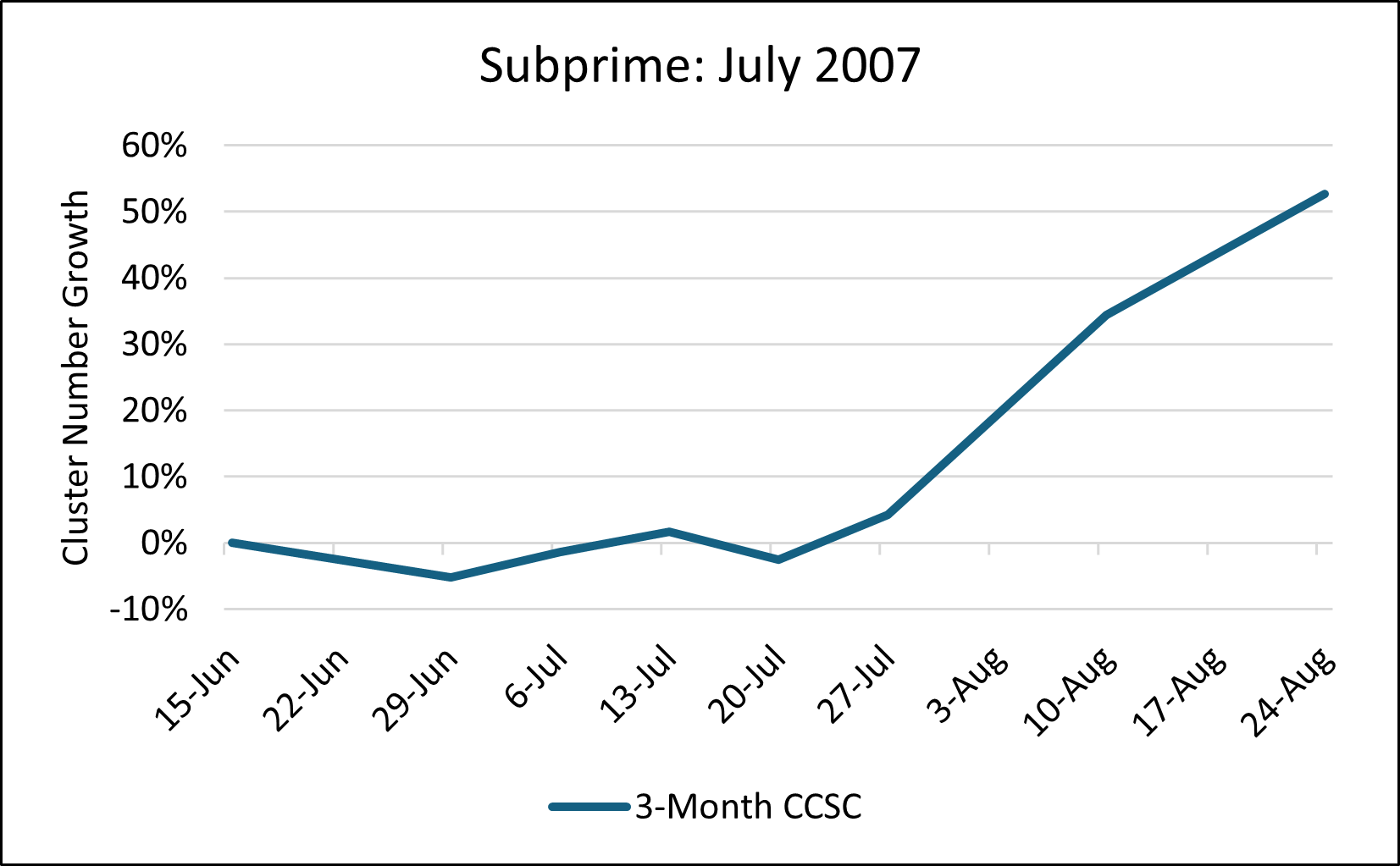

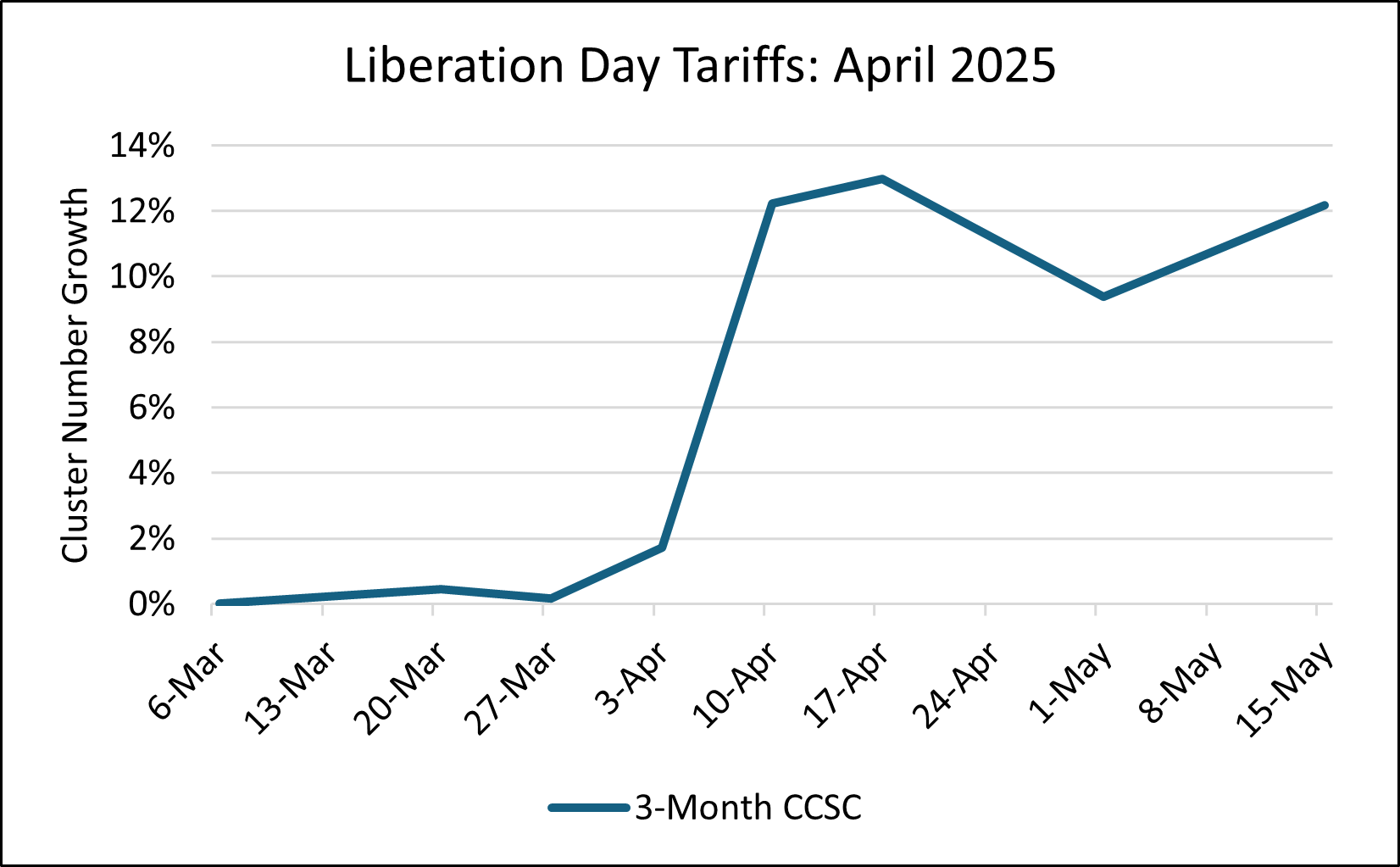

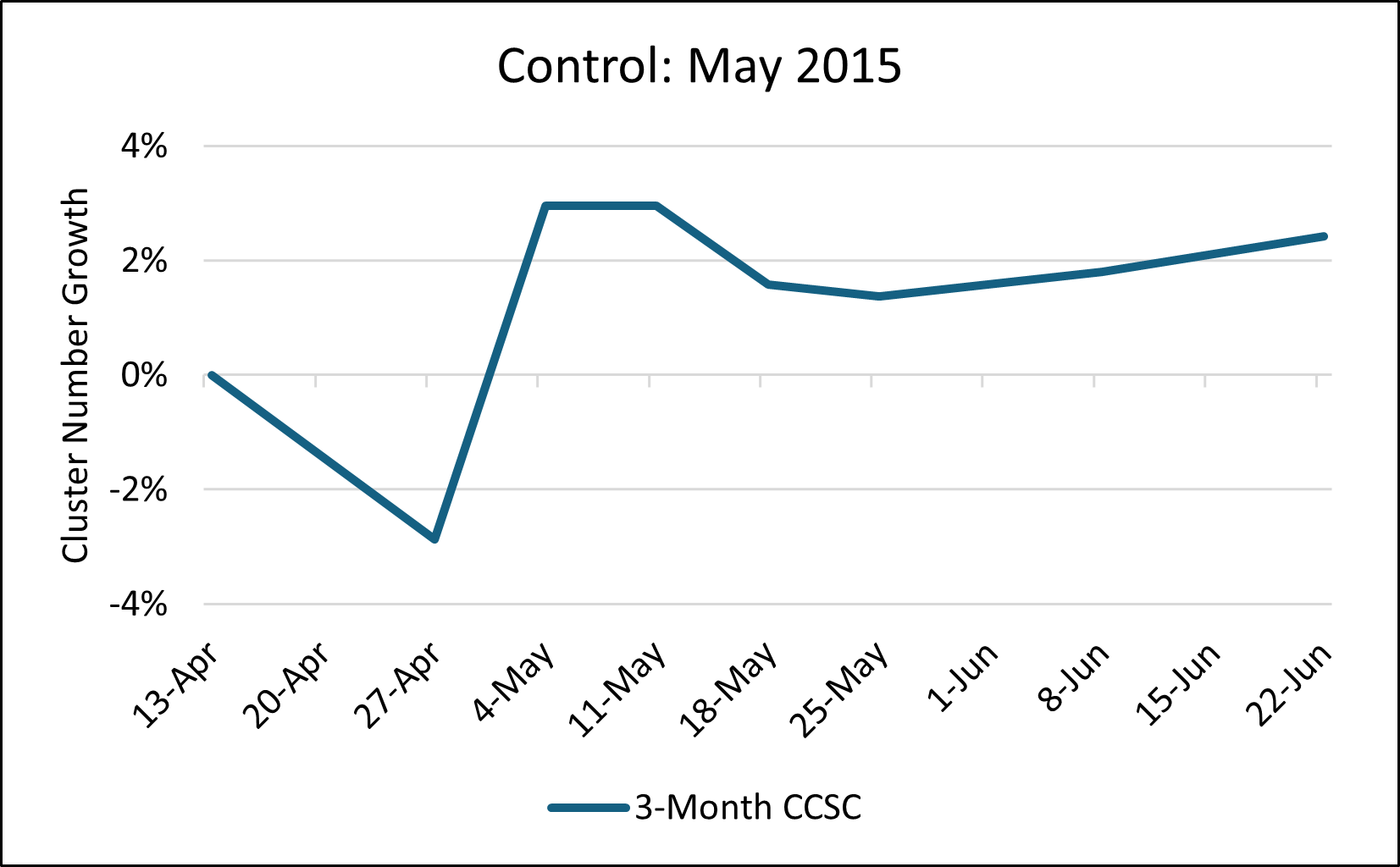

One particularly strong and clear case is the Subprime Crisis, in which the number of clusters rose by 53%. For the Liberation Day Tariffs, the rise was smaller (+13%) but very rapid. Figures 1 and 2 show the rolling growth in the number of clusters over the previous minimum for these two cases. Figure 3 shows the meandering profile of a typical control period, with the number of clusters staying in a band of ±3%.

Figure 1: Rolling change in the number of clusters over the previous minimum

Figure 2: Rolling change in the number of clusters over the previous minimum

Figure 3: Rolling change in the number of clusters over the previous minimum

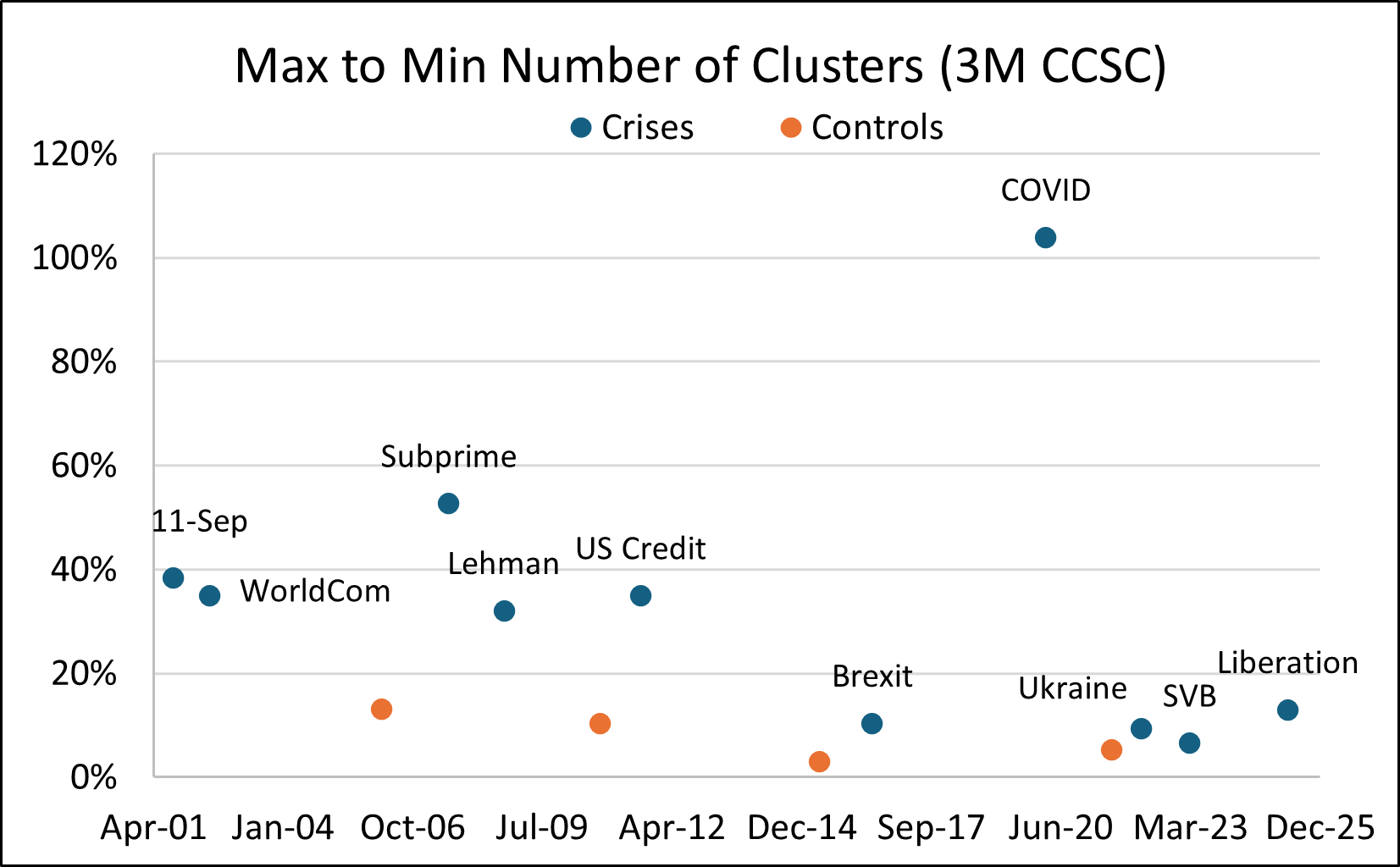

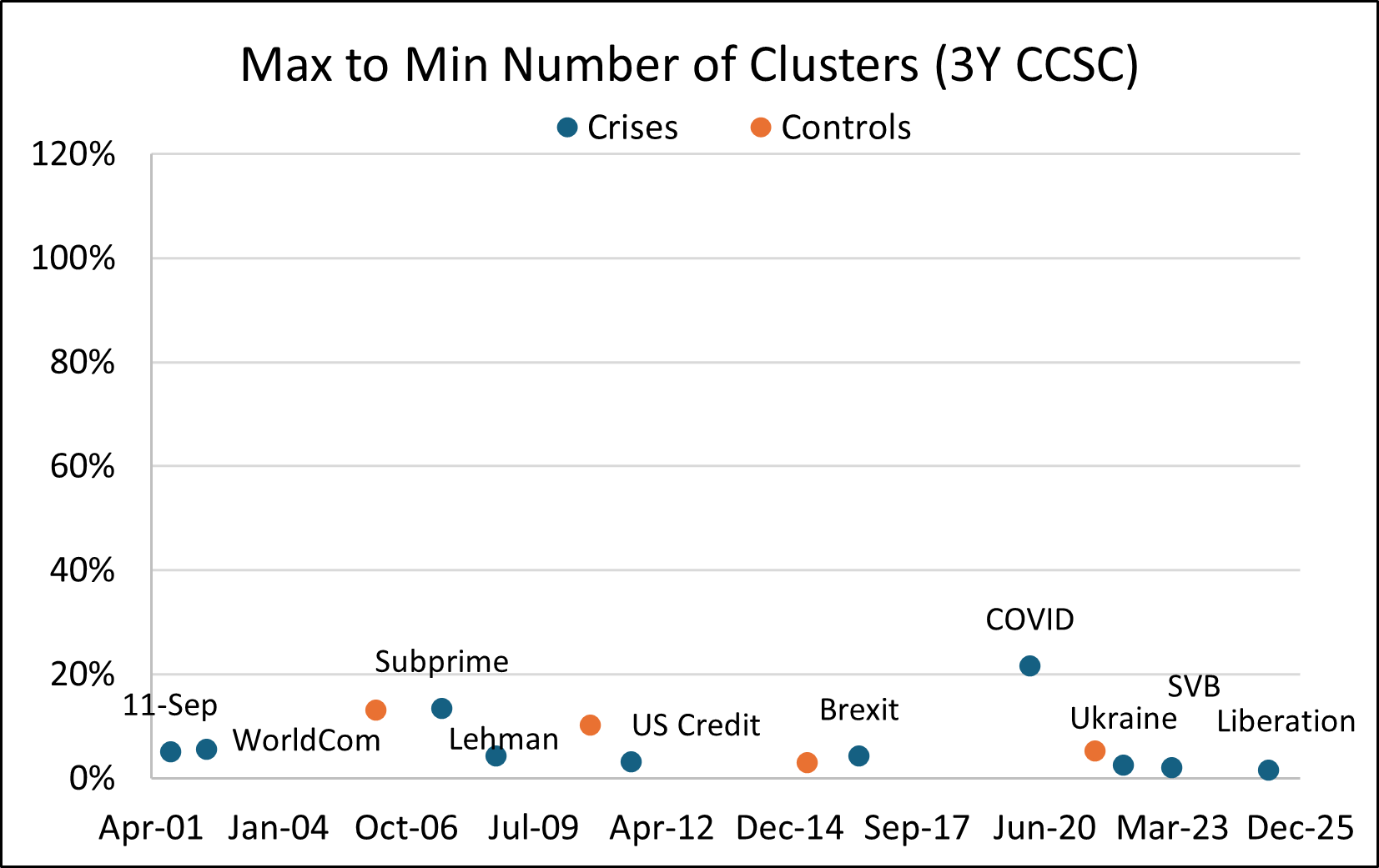

Figure 4 shows the maximum percentage growth over the previous minimum across the ten-week periods for all ten crises and the four controls. It is clear that a significant set of new clusters appeared for six of the ten major crises (increasing by more than 20%), suggesting a real, dynamic systematic structure in the residuals driven by otherwise-hidden crisis factors. Likewise, changes below about +10% are clearly in the noise of random fluctuations. Those in the +10% to +20% range (Tariffs, Brexit, two controls) are a grey area for further study. The standard CCSC process with its longer window would only have detected the major outlier (COVID) with a +22% rise; the other crises didn’t register above the controls in the standard CCSC (Figure 5).

Figure 4: Maximum percent change in number of clusters over the previous minimum across a ten-week period for various crises and control periods using short-term 3-month CCSC

Figure 5: Maximum percent change in number of clusters over the previous minimum across a ten-week period for various crises and control periods using standard 3-year CCSC

Conclusion

This research demonstrates that residuals are not random noise, and short-term CCSC can detect useful information to be exploited – especially during periods of volatility. The implications are far-reaching – beyond the academic. Transient factors represent both a risk and an opportunity that traditional models fail to capture, suggesting practical applications for portfolio managers and risk managers in the hedge fund space.

Learn more about CCSC methodology.

Arnab Banerjee PhD, Axioma Analytics Solutions, SimCorp – Arnab is currently involved in research and product development for Axioma Solutions at SimCorp. Previously, he worked as an independent consultant with institutional investors and buy-side firms, developing customized risk management tools and analytics. Before that, Arnab led equity risk modeling initiatives at MSCI, where as Vice President of Product Development, he collaborated with research, sales, and marketing teams to execute global risk model development strategies. Arnab holds a Doctorate in Business Administration from Georgia State University, and an MS in Financial Engineering from Columbia University. He is also FRM (Financial Risk Manager) certified by GARP.

Arnab Banerjee PhD, Axioma Analytics Solutions, SimCorp – Arnab is currently involved in research and product development for Axioma Solutions at SimCorp. Previously, he worked as an independent consultant with institutional investors and buy-side firms, developing customized risk management tools and analytics. Before that, Arnab led equity risk modeling initiatives at MSCI, where as Vice President of Product Development, he collaborated with research, sales, and marketing teams to execute global risk model development strategies. Arnab holds a Doctorate in Business Administration from Georgia State University, and an MS in Financial Engineering from Columbia University. He is also FRM (Financial Risk Manager) certified by GARP.

Robert D Stock PhD, Axioma Analytics Research, SimCorp – Bob develops Axioma factor risk models for SimCorp. After earning his undergraduate degree in Physics from Princeton and his doctorate in Physics from Carnegie Mellon, Bob worked for nearly a decade at MIT’s Lincoln Laboratory in the Directed Energy Group, performing simulations and analysis of high energy laser beam propagation through the atmosphere for missile defense applications. Bob then served the Ultra-High Net Worth segment for 15 years, first as a Quantitative Researcher for a boutique outsourced-CIO where he developed the majority of the firm’s intellectual property for hedge fund analysis, risk management, forecasting, and asset allocation. Subsequently, he served as a systematic portfolio manager for a large Trust before joining Axioma (now part of SimCorp) in 2022.

Robert D Stock PhD, Axioma Analytics Research, SimCorp – Bob develops Axioma factor risk models for SimCorp. After earning his undergraduate degree in Physics from Princeton and his doctorate in Physics from Carnegie Mellon, Bob worked for nearly a decade at MIT’s Lincoln Laboratory in the Directed Energy Group, performing simulations and analysis of high energy laser beam propagation through the atmosphere for missile defense applications. Bob then served the Ultra-High Net Worth segment for 15 years, first as a Quantitative Researcher for a boutique outsourced-CIO where he developed the majority of the firm’s intellectual property for hedge fund analysis, risk management, forecasting, and asset allocation. Subsequently, he served as a systematic portfolio manager for a large Trust before joining Axioma (now part of SimCorp) in 2022.