Insights based on multiple surveys of over 100 global allocators into alternatives in 2025

The allocator playbook underwent a subtle but significant recalibration in 2025. Whilst headlines fixate on the inexorable rise of multi-strategy behemoths and their gravitational pull on institutional capital, a more nuanced story emerges from Hedgeweek’s comprehensive surveys of global allocators. The traditional dynamics between limited partners and general partners are shifting, with operational excellence now commanding equal billing to performance pedigree.

Our research, drawing from multiple surveys of institutional investors allocating to alternatives, reveals four distinct demands that are reshaping how capital flows through the hedge fund ecosystem. These aren’t merely preferences – they represent fundamental shifts in how allocators assess, select, and monitor their hedge fund investments in an increasingly institutionalised marketplace.

…

1. New relationships remain important to allocators

An interesting finding from our research reveals that 40% of allocators are actively seeking new hedge fund managers rather than reinforcing existing relationships. Just 13% are focused on re-investing with current managers, while the remainder are adopting a mixed approach.

Manager selection preferences

This trend emerges despite mega hedge fund multi-managers hoovering up significant capital. Niche new strategies promising diversification often with better terms, SMAs, and lower fees seem of particular interest to allocators. This is especially relevant as mega multi-managers prove expensive with relatively high management and performance fees, alongside a growing use of ‘pass-through’ fees.

…

Key Insight: While inflows may be concentrated in multi-managers, allocators are actively exploring fresh relationships, suggesting a bifurcated market where scale and specialization both have their place.

Find the full report here.

…

2. We might have passed peak fee compression

Despite ongoing industry pressure on fees, the survey reveals surprising stability in fee expectations:

The 23% actively negotiating lower fees likely reflects standard institutional practice rather than widespread dissatisfaction. More tellingly, 22% express willingness to accept higher fees for certain strategies or managers, indicating that performance differentiation remains paramount. This suggests a more nuanced relationship between cost and value than simplistic fee compression narratives would suggest.

Allocator fee expectations

Find the full report here.

…

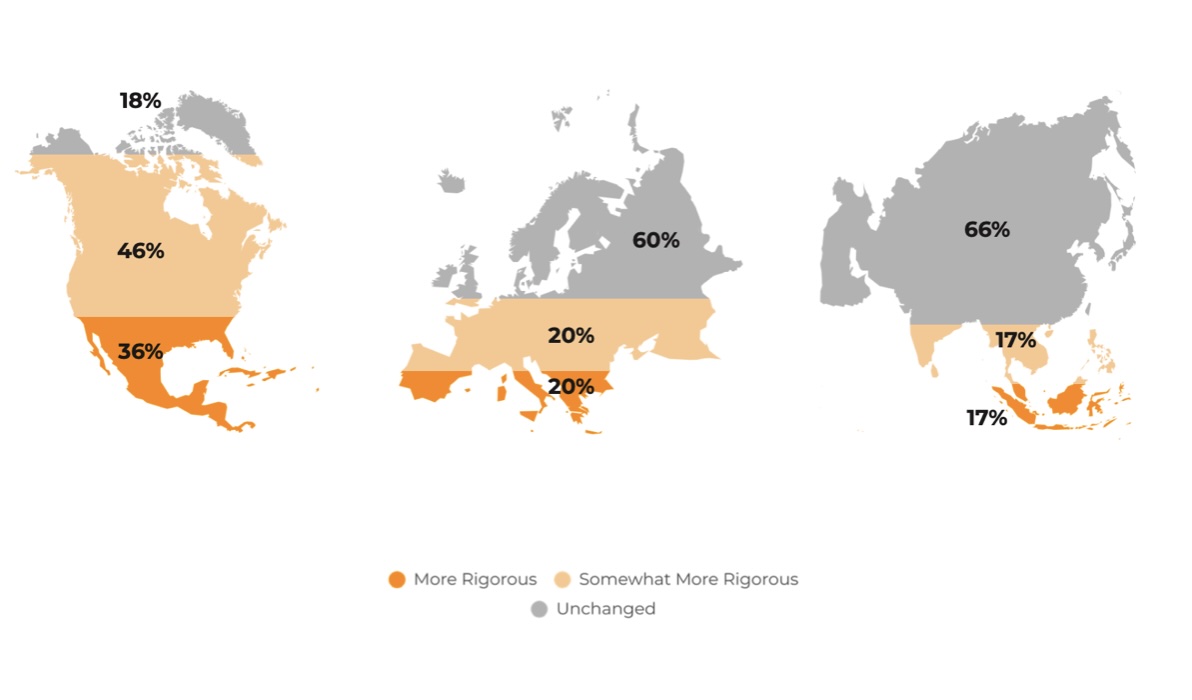

3. Operational alpha is essential

Allocators are not looking for new relationships where they get burned. Capital efficiency is paramount – if they’re venturing beyond the big multi-managers, they want every dollar to count.

Operational due diligence has become dramatically more stringent, with four in five North American allocators increasing scrutiny versus just a third in Asia-Pacific. This stark regional divide mirrors shadow book expectations: nine in ten Western allocators now demand these capabilities, whilst only a third of Asia-Pacific allocators consider them important – creating a strategic investment dilemma for globally-focused managers.

Regional operational due diligence changes

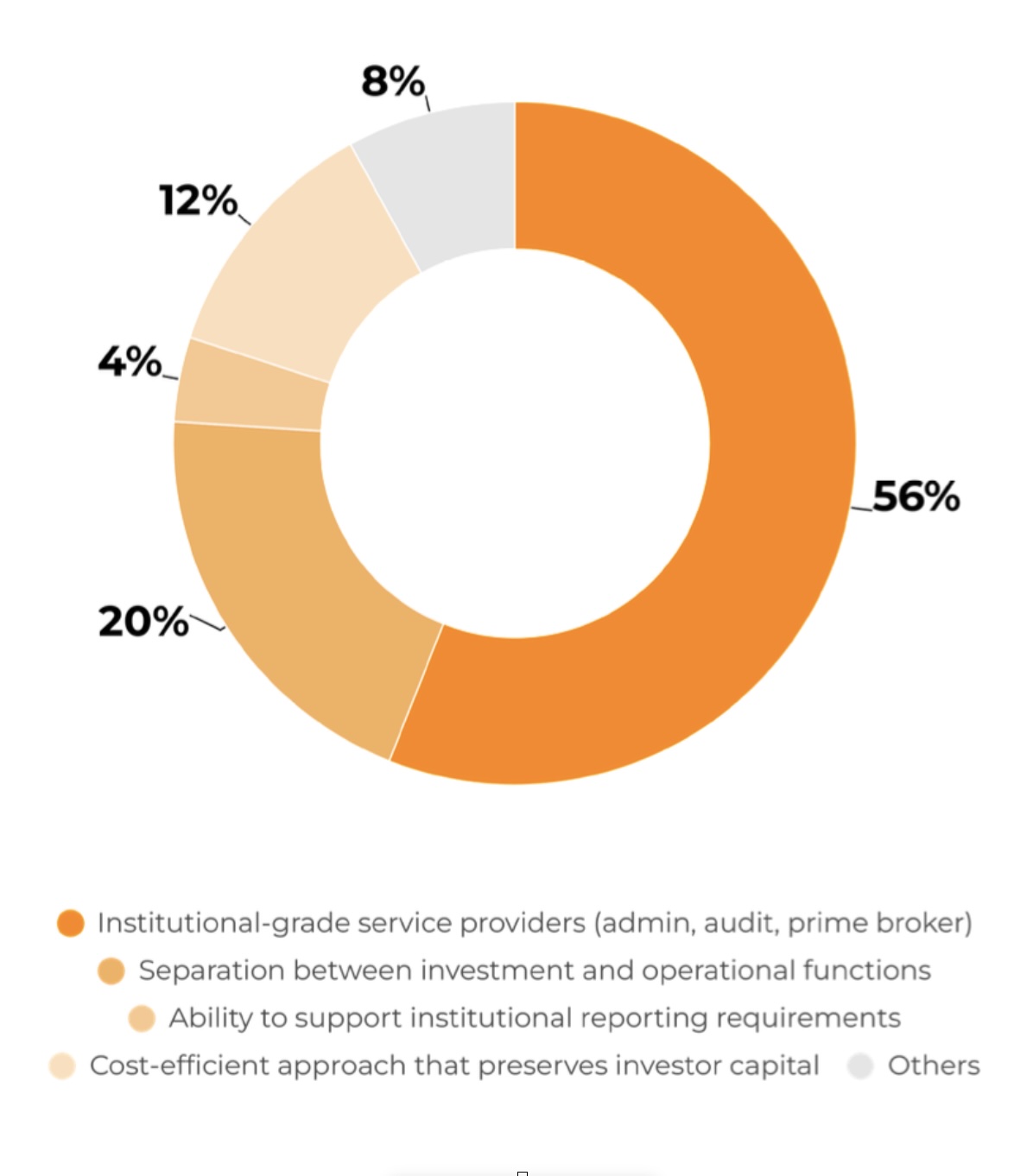

Over half of allocators (56%) now consider institutional-grade service providers a minimum operational requirement for emerging managers. More critically, nearly three-quarters view absent independent fund administration as an immediate red flag – the single most important infrastructure requirement.

Minimum operational requirements

…

Bottom Line: The infrastructure bar has risen dramatically, with proper service providers and fund administration becoming immediate disqualifiers rather than mere preferences in allocation decisions.

Find the full report here.

…

4. Scaling roadmaps are now essential

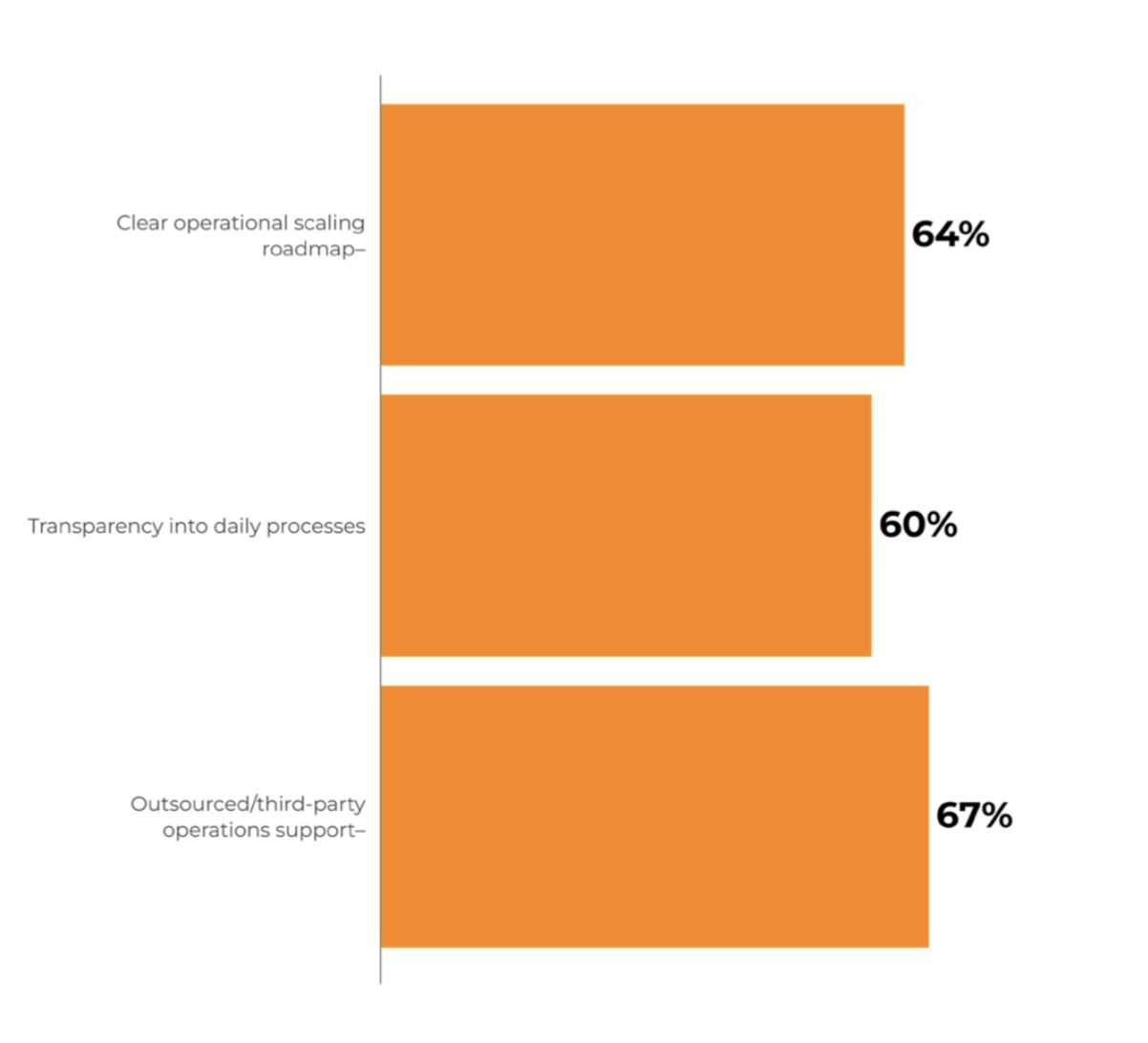

Beyond current operations, allocators want visibility into managers’ future scaling capabilities. Clear operational scaling roadmaps rank as the top comfort factor for allocators, especially in North America where 63.6% cite this as essential.

What would make allocators more comfortable with a manager’s operational setup?

Meanwhile, managers face significant operational challenges when thinking of scaling, with adding new funds representing their most challenging operational hurdle (35.2%). This highlights a critical gap between investor expectations and operational reality.

The message is clear: allocators are looking beyond current capabilities to assess whether managers have the vision and infrastructure to grow sustainably. Those who can articulate and demonstrate a credible scaling strategy will have a significant advantage in attracting institutional capital in an increasingly sophisticated and demanding marketplace.

Find the full report here.

…