PARTNER CONTENT

By Nanette Abuhoff Jacobson, Multi-Asset Strategist and Adam Berger, CFA, Multi-Asset Strategist, Wellington Management

In 2026, we think economic and market conditions will make a compelling case for adding hedge funds to a traditional asset allocation mix. In particular, multi-strategy hedge funds and equity long/short hedge funds may help investors address the effects of three macro concerns:

1. Elevated inflation

After a long absence, inflation returned in 2022 and we expect it to linger in coming years, driven by:

- Deglobalization and trade tensions as countries seek to protect domestic industries

- Tight labor markets, which will push wages higher

- Underinvestment in commodity production, leaving supply short of demand

- Rising government deficits and a lack of political will to cut spending

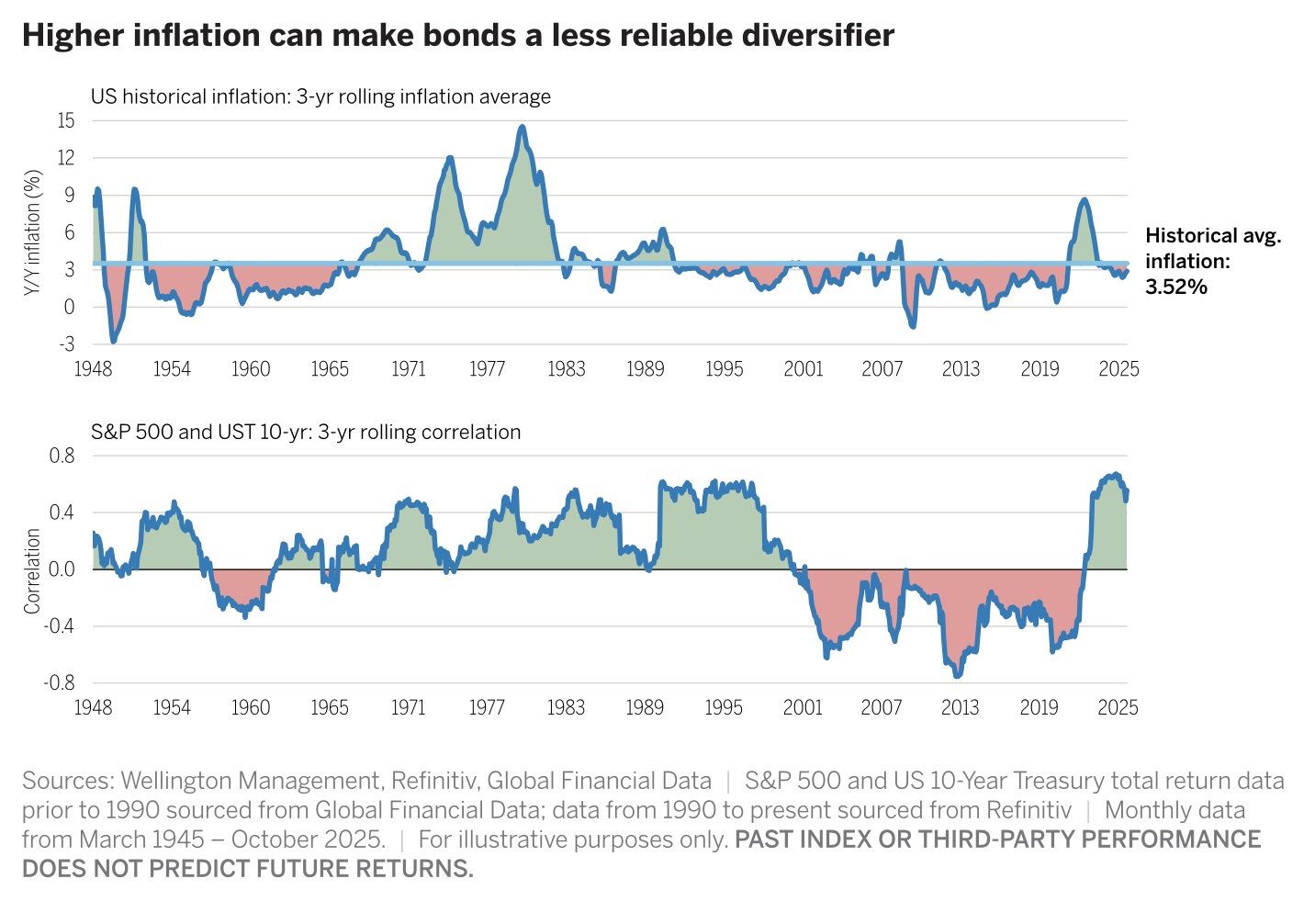

Why does this matter from an asset allocation standpoint? Investors have long relied on the negative correlation between stocks and bonds for diversification purposes (i.e., when stocks struggle, bonds help cushion the blow). But historically, higher inflation has been a key driver of positive stock/bond correlations (Figure 1), as it tends to push interest rates up and bond prices down, while simultaneously eroding equity valuations and challenging margins.

Given the potential for the stock/bond relationship to be less reliable in periods of higher inflation, we think investors should consider broadening their portfolio toolkit to include multi-strategy hedge funds — and specifically moving some capital from fixed income to multi-strategy funds. These funds generally maintain exposure across hedge fund strategies, such as macro, long/short equity, and long/short credit strategies, in pursuit of a more stable risk and return profile. They may include a wide array of independent, specialized risk takers; pursue strategies across a range of asset classes; and combine systematic and fundamental investment processes. By combining strategies and tightly managing their aggregate risk, multi-strategy funds create the potential to provide considerable portfolio-level diversification.

2. Rising volatility

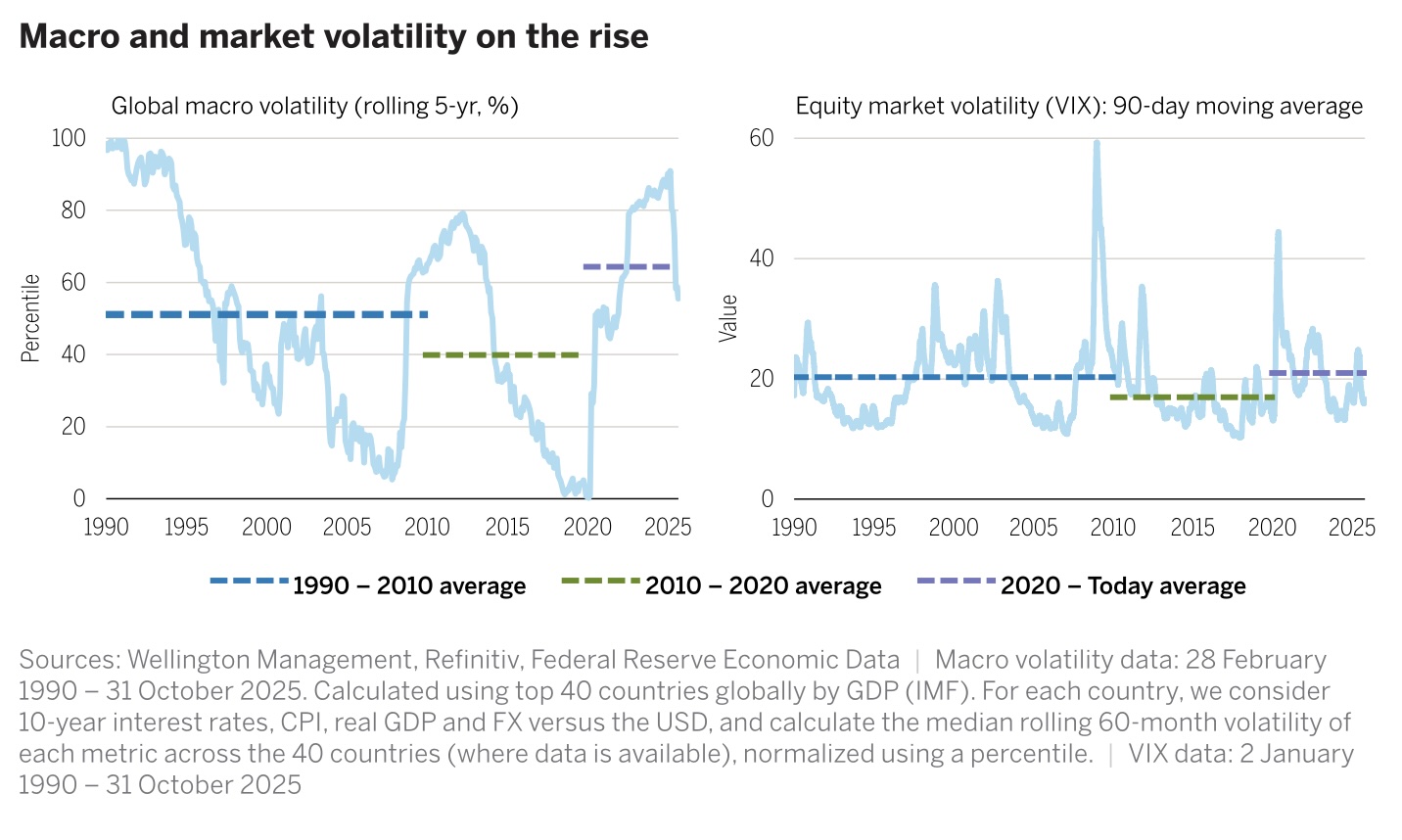

Like inflation, economic and market volatility were relatively subdued in the years following the global financial crisis (Figure 2). Because inflation was not a concern, central banks could respond to any economic decline by easing monetary policy. Aside from a brief recession during the pandemic, we saw slow but mostly positive growth. With interest rates low, companies could borrow cheaply, helping to boost earnings and fund share repurchases.

But since 2020, global macro volatility has risen substantially. As for market volatility as represented by the VIX (right chart), it was rarely higher than 20 and was often below 15 during the 2010 – 2020 period, but since 2020 it has rarely been below 15 and frequently been well above 20.

Inflation is a key culprit, forcing central banks into a difficult balancing act as they try to manage rising prices while also supporting economic growth. This is resulting in more policy uncertainty across regions and, as our global macroeconomics team has argued, it is likely to drive greater cyclicality and dispersion in economic outcomes going forward. Also contributing to the volatility are the unprecedented surge in government debt burdens and concerns about institutional credibility since the pandemic, as well as geopolitical tensions in many parts of the world.

All of this may add up to more boom/bust and bull/bear cycles going forward. One way investors may be able to make their portfolios more resilient is by replacing some of their equity exposure with equity long/short hedge funds. By design, these funds tend to have less equity market exposure (“beta”) than long-only equities. In addition, long/short hedge funds tend to have dynamic exposure to the equity market, meaning they can bring their “net” long exposure down to help protect capital during sell-offs. With these potential advantages, we would expect equity long/short hedge funds to meaningfully outperform long-only equities in a deep sell-off (though they would likely be down, perhaps significantly, in the event of a sudden and rapid market collapse).

3. Rich valuations

Strong market gains, especially in US mega-cap technology stocks, have left investors to contemplate the potential downside of high valuations and extreme levels of index concentration. As of 30 October 2025, for example, the trailing PE ratio of the S&P 500 was at nearly the 96th percentile for the past 20 years. The only sustained period with a higher result was the post-pandemic stretch from August 2020 to July 2021.

We think hedge funds can help by providing a return source that does not depend on market beta. While we recognize that some investors may be skeptical about hedge funds, given some cases of challenging performance over the past decade, we think we’ve entered an environment that may be more fertile for hedge funds, including the higher levels of macro volatility and interest rates noted above. Our research suggests these are among the factors that have historically driven stronger periods of hedge fund performance.

What to do next: Implementation ideas

A key question for investors contemplating the role hedge funds can play in today’s market is how to incorporate them into an existing portfolio. In our latest research, we look at how different allocations to multi-strategy and equity long/short funds could enhance a traditional portfolio. We also discuss the all-important manager selection process. Read more in our new paper, “Are hedge funds the missing ingredient?”