PARTNER CONTENT

By Saboor Zahir, Axioma Product Specialist, SimCorp

The hedge fund landscape has never been more competitive. In Q2 2025 alone, hedge fund asset inflows reached $24.8 billion1, marking the largest quarterly inflow since 2014. It’s no surprise emerging managers face an uphill battle to differentiate themselves in an increasingly sophisticated marketplace.

In the last decade, the industry has been transformed. Multi-manager pod-style platforms dominate asset gathering, managed account adoption has surged, and institutional investors now represent the majority of hedge fund capital. These sophisticated allocators evaluate managers through a risk lens first, seeking partners who can provide granular transparency into portfolio construction, factor exposures, and downside protection.

What does this mean for emerging managers?

This shift represents a clear pathway to competitive advantage: those who can demonstrate granular risk transparency, robust governance, and institutional-grade infrastructure, are the ones that are poised to capture more asset flows.

Key Risk Indicators for Competitive Differentiation

Allocators are looking for quantitative ways to assess the alpha and diversification benefits within their hedge fund investments. Reporting on key risk indicators can allow emerging managers to prove their worth. Below, we outline the ‘must-have’ analytics that your risk system should be able to handle.

Exposure Analysis

Exposure analysis allows investors to isolate asset class level analytics. Leading managers need to be able to quantify specific positions and identify how well hedged portfolios actually are. These metrics are easy for investors to compare and aggregate across many hedge funds.

Critical metrics include:

- Equity Beta Exposure: Simplifying equity exposure into beta exposures allows allocators to have confidence that they are truly paying for alpha.

- 10-year Equivalent: Interest rate exposure to a familiar asset class allows investors to quantify the duration risk being taken.

- Delta adjusted notional for equity/FX/Commodities: Accounting for leverage of options is critical in understanding risks across asset class.

- Sensitivities (DV01, CS01, Inflation01): Offering a clear and intuitive view of key exposures that can be aggregated across multiple sources.

Value-at-Risk (VaR)

While exposure analysis provides asset class granularity, VaR offers the unified risk picture allocators need for portfolio construction. For example, how can managers combine equity beta exposure with a 10-year equivalent treasury exposure? The best way to do this is use a unified risk forecast that models all asset classes.

Value-At-Risk allows clients to unify risk across asset classes while simultaneously focusing on losses. The most common forecast for VaR is a 1-day 99% confidence level with a 1-year lookback using historical simulation.

Factor Analysis

Factor analysis offers a different lens into risk – the capability that separates managers who understand their return sources from those operating on intuition alone. Allocators increasingly evaluate managers based on factor exposure transparency and diversification quality. Historically, factor analysis has been focused on equity strategies but new models in credit have given fund managers similar tooling in credit.

Essential factor analysis includes:

- Systematic vs. Idiosyncratic Risk Breakdown: Prove you’re generating alpha from genuine security selection rather than disguised factor bets.

- Industry and Country Attribution: Demonstrate conscious sector positioning versus accidental concentration.

- Style Factor Tilts: Quantify exposure to Quality, Value, Momentum, volatility or leverage factors.

- Crowding Analysis: Hone on crowding factors to protect against diving into crowded hedge fund favorites and short squeeze candidates.

Stress Testing

Ultimate diversification comes from the ability for portfolio positioning to withstand losses during extreme market events. Stress testing allows firms to find blind spots in their current positioning while also testing resiliency.

Effective stress testing encompasses:

- Historical Scenario Analysis: Historical stress tests like the Lehman Crisis and Covid allow investors to quantify the downside protection offered by hedge funds through real market crisis. As the saying goes, “history doesn’t repeat itself, but it often rhymes”.

- Predictive stress tests: While historical stress tests look backwards, forward looking scenarios allow investors to have foresight into prospective events and see their impact across asset class. These could be scenarios that are preparing for increases in inflation, or drawdowns in the equity markets.

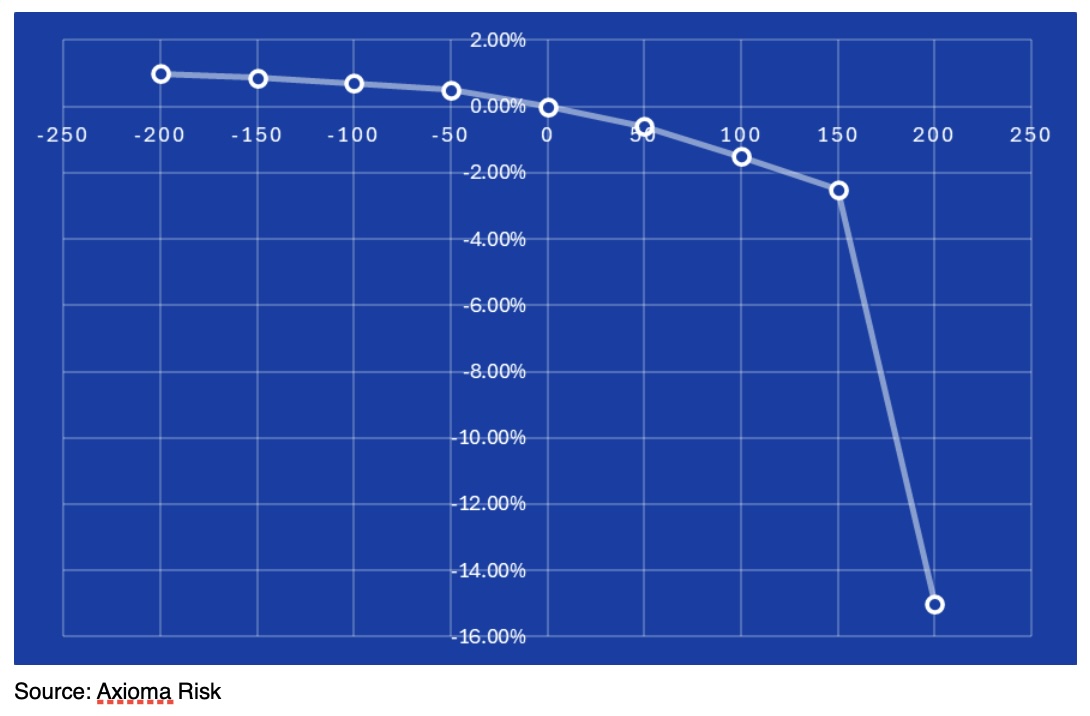

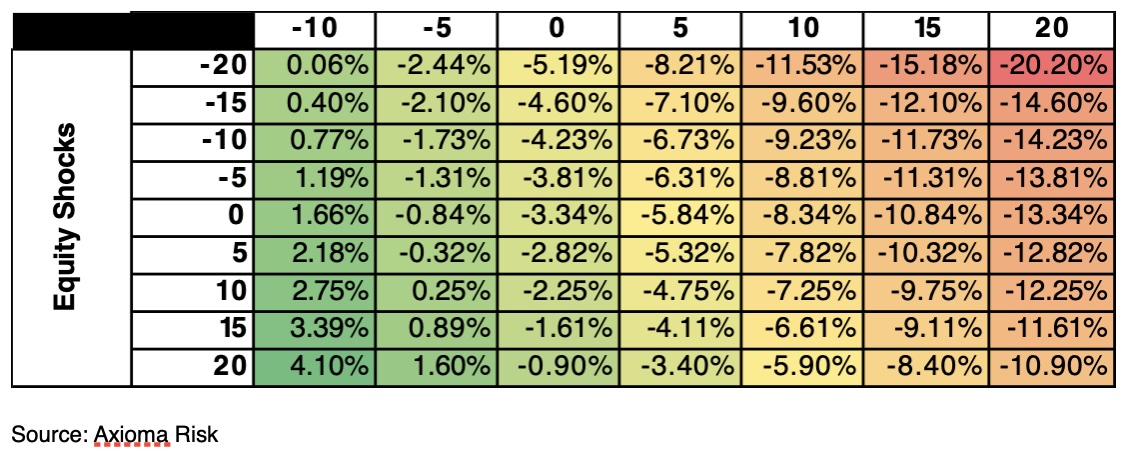

- Laddering parameter: Finding the breakpoint is an important piece in building resilient portfolios. For example, to understand the behavior of a portfolio to changes in equities, a risk manager can apply incremental shocks to equity markets from extreme negative shocks to extreme positive shocks to assess the behavior of a portfolio to changing levels of equity markets. Such analysis can also be done in two dimensions with equity and volatility or interest rates and credit spreads.

Chart 1: Interest Rate Shocks (Bps-X) vs Portfolio Returns (%-Y)

The chart above demonstrates how applying a range of stress tests enables managers to identify key inflection points in their portfolio.

Chart 2: Equity vs Volatility Stress Grid

The chart above goes a step further and looks at a two-dimensional range of equity and volatility shocks for an options portfolio. You can clearly see that the portfolio is quite susceptible to poor performance when equities are down and volatility is up.

Risk Technology as Competitive Advantage

Emerging managers can stand out by providing an elevated level of risk governance and transparency to their investors. Ultimately, this helps validate the diversifying qualities of hedge funds.

Delivering this level of risk transparency however, requires institutional-grade technology. Manual processes and basic spreadsheet analysis cannot provide the real-time, multi-dimensional risk insights that sophisticated allocators demand.

Leading emerging managers need to partner with established risk management platforms that offer comprehensive factor models, stress testing capabilities, and an automated reporting infrastructure. These partnerships allow smaller managers to compete with the risk management sophistication of large multi-manager platforms while maintaining operational efficiency.

To learn more, visit us at www.simcorp.com/axioma.

Footnotes

- https://www.hfr.com/media/market-commentary/global-hedge-fund-industry-surges-through-2q-volatility/

Saboor Zahir, Axioma Product Specialist, SimCorp – Saboor leads the Analytics Solutions Engineering team for SimCorp Americas, focusing on risk, performance attribution, and portfolio construction, including Axioma products. Saboor’s previous roles include leading the Axioma risk specialist teams that acted as firmwide subject matter experts in risk analytics on behalf of Axioma clients. Saboor holds a BSc in Electrical Engineering and MSc in Financial Engineering from New York University. He is also a CFA charter holder and an FRM.

Saboor Zahir, Axioma Product Specialist, SimCorp – Saboor leads the Analytics Solutions Engineering team for SimCorp Americas, focusing on risk, performance attribution, and portfolio construction, including Axioma products. Saboor’s previous roles include leading the Axioma risk specialist teams that acted as firmwide subject matter experts in risk analytics on behalf of Axioma clients. Saboor holds a BSc in Electrical Engineering and MSc in Financial Engineering from New York University. He is also a CFA charter holder and an FRM.