Hedge funds are being repositioned to fulfil their original promise. In a striking shift over just six months, institutional allocators have moved decisively away from viewing hedge funds as yet another return maximiser and toward valuing them as portfolio stabilisers.

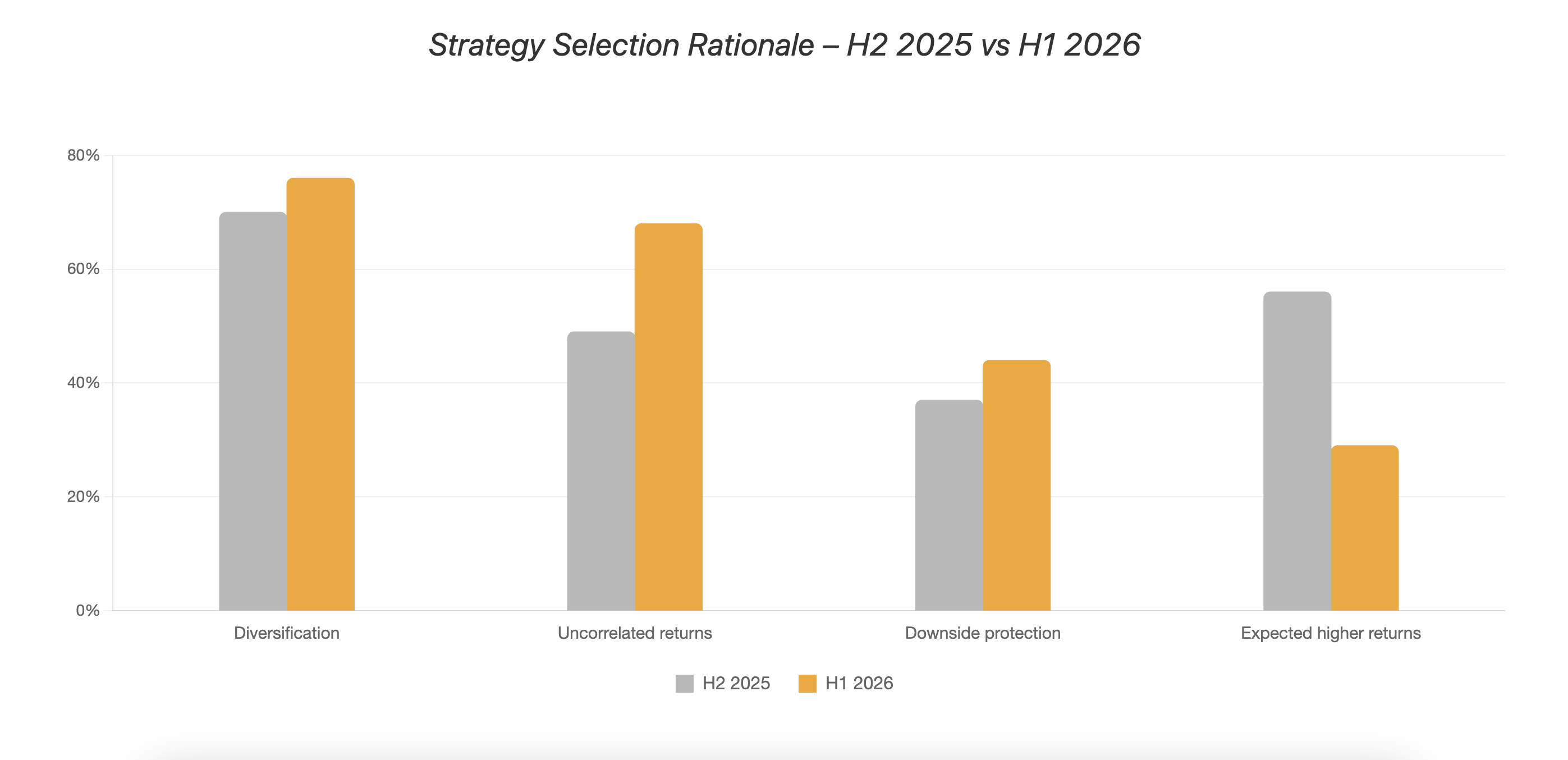

The change is captured in two dramatic data points from the Hedgeweek-AIMA H1 2026 Allocator Survey: the percentage citing “uncorrelated returns” as a key rationale for hedge fund allocation has surged from 49% to 68%, while those citing “expected higher returns in current market conditions” has collapsed from 56% to 29%.

That 19-percentage point jump in uncorrelated returns, combined with the 27-point collapse in higher return expectations, represents the most significant finding in the survey.

“Allocators are explicitly telling us they value hedge funds for portfolio construction benefits – diversification, low correlation, downside protection – rather than outright return maximisation,” AIMA’s head of research and communication, TomKehoe notes.

But this isn’t new thinking, he emphasises. “More established, sophisticated investors would not look to hedge funds to deliver higher returns. They would describe it as delivering uncorrelated performance.”

What’s changed is this view has become explicit and widespread.

A large pension plan allocator explains: “The single biggest shift is the geopolitical realignment and having to think about diversifying US dollar and asset exposure given the tremendous run in equities. Can it go on for another year? It’s about hedging risks. Too much USD, too much equity beta.”

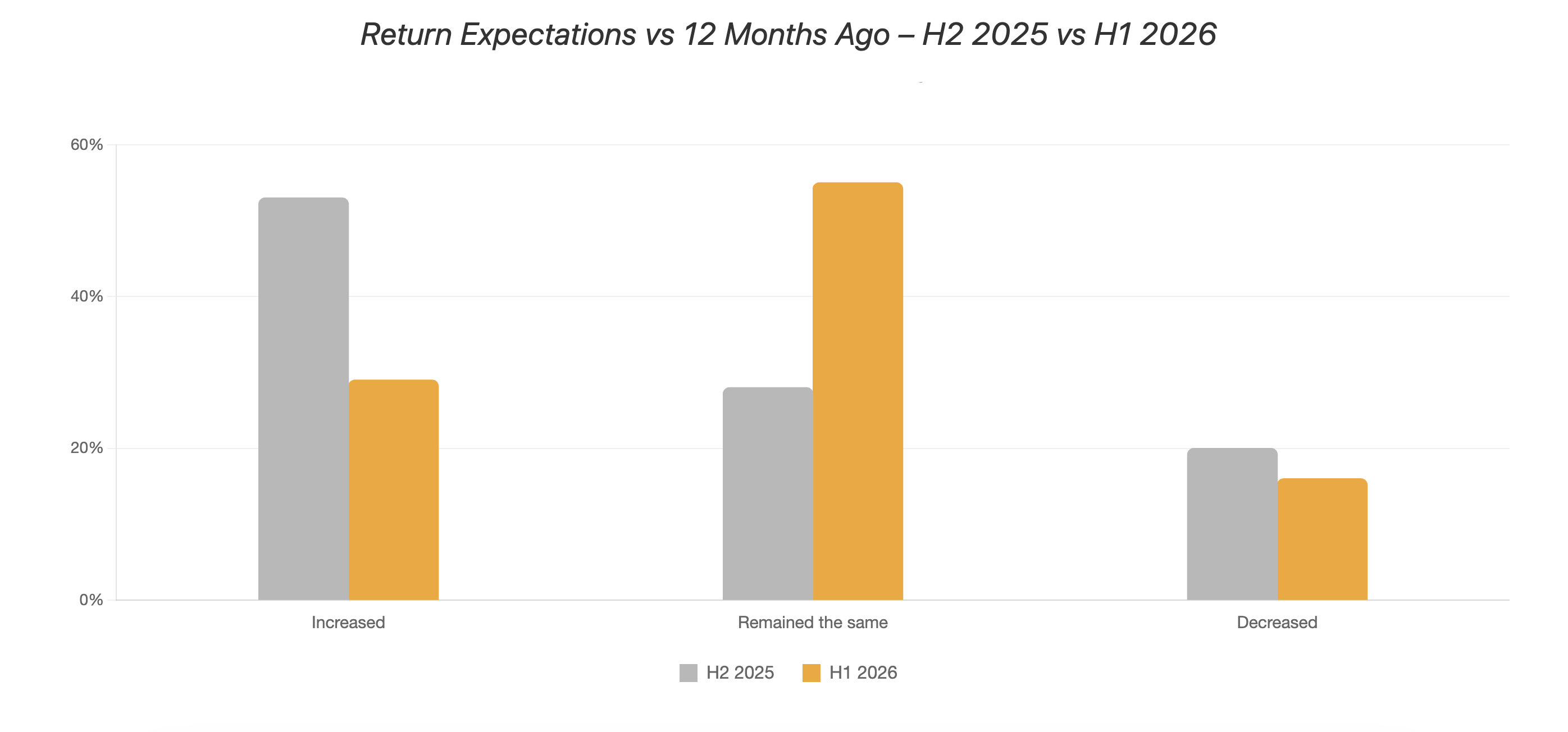

Supporting this repositioning, return expectations have normalised dramatically. Just 29% of allocators have increased their return expectations compared to twelve months ago, down from 53% in H2 2025. Meanwhile, 55% expect returns to remain the same, compared to just 28% six months prior.

Crucially, this normalisation is occurring alongside record confidence levels. Seventy-one percent of allocators express confidence their hedge fund portfolios will meet targets, with 34% very confident – up from 19% six months ago.

“The normalisation of return expectations is healthy,” Kehoe suggests. “After several years of strong hedge fund performance, allocators are being realistic about what’s sustainable. The fact that confidence remains high while return expectations moderate tells us allocators are satisfied with steady, risk-managed performance.”

This combination – high confidence with modest expectations – reveals allocators are content with consistent, uncorrelated performance rather than reaching for outsized gains.

For hedge fund managers, the message is unambiguous. Success in 2026 won’t be measured primarily by headline returns. It will be measured by whether managers can deliver genuine diversification and uncorrelated returns consistently – particularly when traditional portfolios face stress.

The question allocators are asking isn’t “What returns will this hedge fund deliver?” It’s “If there’s a market correction, what will this hedge fund deliver? Will it protect my portfolio?”

That’s the new value proposition. Managers who can answer that question convincingly will retain and grow institutional capital. Those who can’t – regardless of past performance – may face redemptions.