Interest rate volatility is like a storm cloud building on the horizon. The US Federal Reserve has kept rates stable for nigh on a decade, but global asset managers are now preparing for their fixed income portfolios to feel the impact of a rate rise later this year.

In a speech delivered at Jackson Hole on 29 August, US Federal Reserve Vice Chairman Stanley Fischer gave the latest indication of an imminent interest rate hike by saying: “There is good reason to believe that inflation will move higher as the forces holding inflation down – oil process and import prices, particularly – dissipate further.”

Whatever the impact on global markets, managers and investors will need to find ways to hedge their portfolios against rising rates and higher volatility in the fixed income market.

New tools available to fixed income investors and traders are the CBOE/CBOT 10-year US Treasury Note Volatility Index (TYVIX℠ Index), introduced by the Chicago Board Options Exchange® (CBOE®) in May 2013, and TYVIX futures, (ticker symbol VXTY), launched in late 2014, which give traders an effective way to hedge, gain exposure to, or trade interest rate volatility.

The TYVIX Index

Just as the CBOE Volatility Index® (VIX® Index), measures the expected volatility of the broad stock market, the TYVIX index measures the expected volatility of the interest rate market. The index is calculated using transparent prices from the CBOT’s 10-year Treasury note options and is updated and disseminated continuously throughout the trading day.

“The CBOE VIX, known as the market’s fear gauge, is derived by taking prices from the S&P 500 options market and plugging those data points into the CBOE VIX methodology,” explains John Angelos (pictured), Director, Institutional Marketing Credit Derivatives at CBOE. “Using the CBOT 10-year Treasury note options prices, we apply essentially the same methodology as the VIX Index calculation to those prices to create a fixed income volatility index – TYVIX.

“Technically, the VIX index is a real-time measure of expected 30-day volatility of the S&P 500 and the TYVIX index is a real-time measure of expected volatility of the 10-year Treasury note futures listed on the Chicago Board of Trade (CBOT), which is the most actively traded listed interest rate market.”

Just as the VIX index acts as a barometer of rising anxiety within the market with respect to equity price volatility, so the TYVIX Index provides an equivalent window on the rise or fall in implied volatility within the 10-year T-note market.

By looking at the TYVIX Index, one can see what the market’s expectations are of future bond price changes. The more uncertainty there is around changes to interest rates, the higher the TYVIX index tends to be.

“Fixed income portfolio managers have long recognised the need to hedge the volatility component of those portfolios, but the way to do that is quite a cumbersome and inexact process,” says Angelos. “Typically, what those portfolio managers would do is put on a straddle – trading an at-the-money option on Treasury calls and puts. But to be effective, you had to try to isolate movements in the underlying price, which is referred to as ‘delta hedging’ your position.

“To continue that process over a period of time you have to continually adjust that position – which is a complex, risky, and not very cost-effective exercise,” he adds. “What CBOE has done is take the tested and proven way of trading volatility (the VIX methodology) which allows you to trade volatility in its purest form using a single contract.”

In other words, TYVIX futures contracts remove that inherent complexity. Because the volatility component is separated out from the options, investors are able to trade pure volatility without the directional price risk of the options. By eliminating the need to ‘delta hedge’ multiple options contracts, TYVIX futures provide a more cost-efficient and effective way to trade volatility. TYVIX futures are cash settled to the level of the underlying TYVIX cash index at expiration, further simplifying the trading process.

Meet the creators

Building on the popularity of the VIX Index and the growing use of VIX options and futures for hedging and managing risk, CBOE sought to expand the VIX methodology to other asset classes. The exchange already had launched volatility products based on other indexes, such as the Russell 2000® Index, and ETFs, such as gold, oil and emerging markets. As interest rate concerns came into focus as Fed policy shifted, CBOE’s product research staff members explored ways to create a volatility index for the fixed income market.

In 2010, CBOE connected with Yoshiki Obayashi, who is a managing director at Applied Academics LLC, which collaborates with academics and partners with financial institutions to monetise new products. Obayashi had been working with Antonio Mele, a professor at the Swiss Finance Institute, on the design of fixed income volatility indexes. Obayashi and Mele consulted with CBOE to design what would eventually evolve to become the TYVIX Index.

“At a high level, the methodology that underlies the calculation of TYVIX can be thought of as the VIX methodology applied to the Treasury options market. But the TYVIX is a model-independent measure of implied volatility of the 10-year T-note future as implied by the options on those futures,” explains Obayashi.

“Another nice attribute is that it’s a purely directional measure of volatility. Up until the launch of TYVIX futures, when traders and portfolio managers wanted to express their views on the volatility of interest rates, they’ve had to rely on options-based trading strategies that are strike- and path-dependent, and hope that their positions would correctly capture the volatility movement and they’d get paid out, which doesn’t always happen.” In contrast, “TYVIX futures provide linear exposure to volatility, and is a much cleaner trade,” explains Obayashi.

Having the ability to adjust and respond market volatility could become vital in future, as developed markets (in particular the US and the UK) begin to raise rates as their economies improve.

A strikeless measure of volatility

Another term that is used to describe the TYVIX index is a “strikeless measure of volatility.” An options strike is the price at which investors can buy or sell the underlying contract.

If one has an at-the-money straddle today struck at USD110 and there is a 6 percent implied volatility, and if rates move tomorrow, that at-the-money option will be struck at USD115 with implied volatility at perhaps 5.5 percent. It’s now really difficult to compare those two positions because they are struck at different levels.

“This is what we would call strike- dependent positions: or at-the-money implied volatility,” explains Obayashi. “With TYVIX, by taking the entire skew of the 10-year T-note options from at-the-money all the way to out-of-the-money, it distills down all of the information that is embedded in that skew of options into one number that reflects the fair price of variance of implied T-note futures.

“Given that it is a strikeless, pure directional implied volatility index, if you trade futures contracts on it and the implied volatility pushes it above your purchase price before expiry, you’re going to make money. It’s one of the main attractive features of the index,” says Obayashi.

Mele expands on this methodology by noting that the movements of the TYVIX Index may become particularly severe during periods of market stress, reflecting an increased sensitivity of out-of-the-money options to tail-risk events. The TYVIX Index may oscillate more than at-the-money implied volatilities in periods of turmoil.

“In moments of stress, those out-of- the-money options become more valuable as investors are willing to pay more for protection to tail-risk events. As the price of the options rises it pushes up TYVIX – so if you are long TYVIX futures you will make gains. When we talk about the skew, what we are talking about is these out-of-the- money options, which are more likely to be exercised in tail events,” comments Mele.

Transparency

Another attractive feature of the TYVIX Index is that the data for the calculation comes from a transparent source. The TYVIX Index is derived using prices of highly liquid 10-year Treasury note futures options traded at the CME. Those prices, as well as historical pricing data, are easily accessible and widely available.

That distinguishes the TYVIX Index from the Merrill Lynch Option Volatility Estimate (MOVE) Index, which is calculated once a day using OTC prices that are set by a certain dealer. Further, the MOVE Index uses only at-the-money options and does not take advantage of information embedded in the out-of-the-money contracts, which often tells a much richer story about the market expectations of volatility.

“The transparency of the CBOT T-note options prices and the ability to see all the bids and offers in the market is a real advantage. That’s something you can’t do in the OTC space,” adds Angelos. “We calculate TYVIX and disseminate it every 15 seconds; the MOVE Index is marked to market at the end of every day. So if you’re looking to extract meaningful and useful information from the marketplace the TYVIX allows you to do that because it is based on real-time, transparent data that everyone has access to, whether you are a retail or institutional investor.”

Focused time frame

Another aspect of the TYVIX Index is that it focuses on one point of the volatility curve. This further differentiates it from the MOVE index, which blends out averages of implied volatility across the term structure.

“The 10-year curve has been far more active in recent times than the 2-year curve but blending everything together dilutes that activity,” says Obayashi. “TYVIX is useful because it focuses on one point only, the 10-year T-note, which just happens to be where everyone is looking right now.”

Interpreting the TYVIX Index

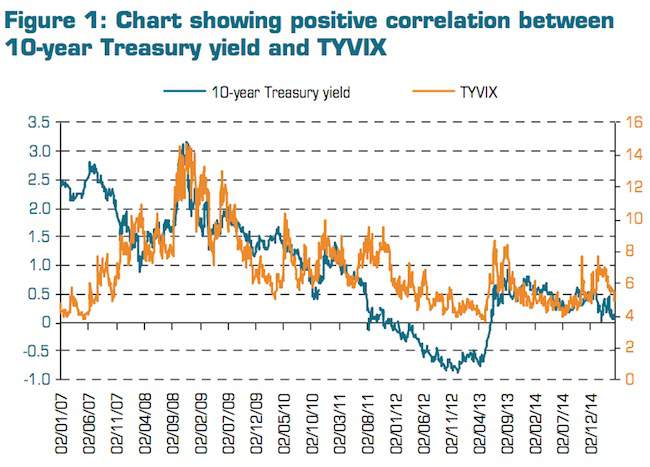

The TYVIX Index is a useful indicator for what to expect in the future. The index, broadly speaking, has a positive correlation to movements in bond yields; see Figure 1. The higher the interest rate (or yield) increases are expected to be on the Treasury note, the higher TYVIX is likely to be.

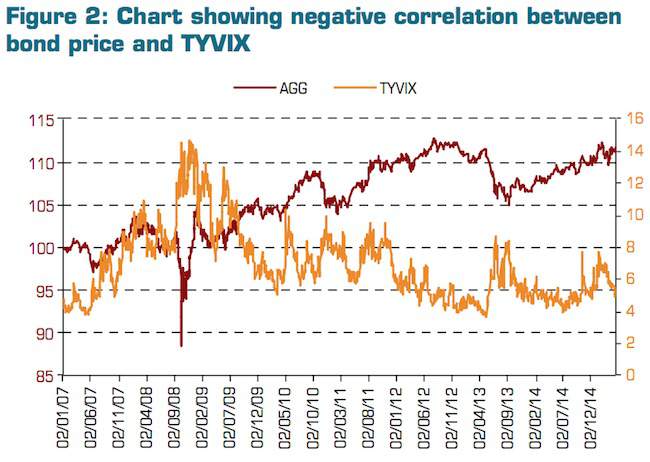

This was observed back in April, for example. Between 24th April and 6th May, the TYVIX Index climbed from 4.89 to 6.53. At the same time, the interest rate on 10-year T-notes rose from 1.91 per cent to 2.23 per cent. Contrast this with the price of bonds and the opposite relationship tends to hold true. During the same period, the iShares Barclays 20+ Year Treasury ETF (TLT) saw its value fall from USD130 to approximately USD121.

“That price move in TYVIX is a reaction to a potential interest rate increase — yet the Fed still hasn’t made its decision. So the market is already preparing itself for that announcement,” says Angelos.

By referring to Figure 2, one can see the negative correlation between the TYVIX Index and AGG, which is another ETF bond portfolio product.

Bond prices could move as a result of a number of different factors. It could be a function of the US fiscal deficit, of changes to monetary policy (FOMC announcements), or inflation expectations. There are various macroeconomic factors at play that will effect market participants’ expectations of bond price movements in the future.

“TYVIX can be applied as a tail risk strategy for a fixed income portfolio just as VIX futures are used to hedge against tail risk in S&P 500 broad-based equity portfolios,” explains Angelos. “If you expect rates to increase in the near future quite significantly, you will start to see a significant decrease in the value of your underlying bond portfolio.

“The gains you make by buying TYVIX futures could offset some of the losses incurred in the underlying bond portfolio. The shorter the Fed policy cycle is and the more severe the rate hike expectations are, the stronger the inverse relationship likely will be between TYVIX and the underlying bonds.”

Using TYVIX futures in diversified bond portfolios

One of the most obvious applications of TYVIX futures as part of managing a bond portfolio or fixed income portfolio more generally would be as a hedging tool against major drawdowns.

AGG is one of the big industry benchmark bond indexes with an associated ETF tracking it. The AGG Index consists of a mix of Treasury bonds, municipal bonds, mortgage-backed securities and investment grade corporates.

“What we’ve been able to show is that, if you look at the correlation between the returns on AGG and hypothetical returns on TYVIX, the returns on TYVIX pick up whenever there are concerns over interest rates in the market,” comments Obayashi.

“During the crisis in 2008-2009 there was very little correlation between the two, which makes sense because it was more of a credit risk story than an interest rate story,” he adds. “Nevertheless, whenever worries about interest rates take centre stage in the market, TYVIX becomes tightly linked with bond portfolio returns.

“The next step is to see what happens if you overlay a bond portfolio with a long position in TYVIX futures. What we are able to show is exactly what we expect, namely that during big drawdowns if you are long TYVIX futures you can smooth out your returns and reduce the extent of those drawdowns.

“We repeated the analysis for muni ETFs, bond ETFs, mortgage ETFs and they all show the same distinct relationship with respect to expected volatility,” Obayashi says.

The following are some illustrative examples of how and when to use TYVIX in a rising interest rate environment.

1. Long volatility hedge

This would be the most straightforward application. Let’s say the manager is long bonds – these could be predominantly Treasuries or a mix of Treasuries, corporates and so on. They will want to analyse the sensitivity of the portfolio to changes in interest rate volatility.

If the manager’s view is that there is going to be turbulence in the bond market they know that their portfolio will likely take a hit. Then that manager would analyse the sensitivity of their portfolio to an interest rate hike, running different stress test scenarios, to figure out how long a position in VXTY futures they should take to mitigate P&L swings in the portfolio.

That is a straightforward, long volatility hedge to guard against a market drawdown.

2. Calendar spread

This is where a trader believes the market is going to be range-bound for the upcoming period. Calendar spreads profit from a rise in implied volatility whereby the long option has a higher vega (a measure of the impact of change in the underlying volatility of the option) than the short option.

By using the TYVIX Index as their reference tool, a global macro or fixed income manager might decide that the curve will be flat for 20 days but that volatility will increase between 20 and 40 days. Since the TYVIX Index reflects 30-day expected volatility, it offers a way to formulate views on the timing of interest rate spikes up or down. In this example, the manager might decide to buy (go long) long-end T-note futures and sell (go short) nearer expiration T-note futures to make tactical gains in the strategy.

3. Scheduled economic events

The TYVIX Index can be useful ahead of scheduled economic events, such as GDP figure releases, central bank announcements, nonfarm payroll figures and so on.

“If you think that the market is erroneously expecting an interest rate decision, causing TYVIX to spike up ahead of the meeting, you could take a contrarian view,” suggests Obayashi. “Maybe you think the TYVIX is overpriced and based on your understanding of what the policymakers will likely do, you might choose to take a short volatility stance by selling TYVIX futures.

“On the other hand, you could be risk- averse and go long VXTY futures over the short-term to protect your long bond portfolio around these big macro announcements. In this way, the TYVIX index can be used tactically throughout the year as a short-term hedging strategy.”

That fits nicely with the underlying Treasury options market because these contracts themselves tend to be actively traded around scheduled announcements.

“TYVIX gives you a much cleaner way to mirror that activity,” adds Obayashi.

4. Short volatility play

One of the most important applications of the TYVIX Index and buying VXTY futures is to hedge against downside risk and seeking to profit from rising volatility.

But what separates the smartest managers from the rest is their ability to assess multiple market factors and take a contrarian view; in other words, to generate alpha in their portfolios. Selling TYVIX is one way of generating alpha, as opposed to merely trading it from the long side.

This could involve disagreeing with the amount of market anxiety as measured by the TYVIX Index. For example, say the value of TYVIX is 5.88. Let’s suppose there’s an upcoming FOMC meeting in one week and TYVIX climbs up to 8. You might be of the opinion that this number is too high and you don’t expect an imminent rate hike.

In such a scenario you could decide to sell VXTY contracts at USD8.5 and sit on them until after the FOMC meeting. If you call it right, the FOMC meeting is a non- event, market volatility falls and the price of VXTY futures drops to USD6.5, you’ll make USD2 per contract on the trade (with a contract multiplier of USD1,000 that equates to a profit of USD2,000 per contract.)

In that sense, the TYVIX Index may be the simplest form of directional volatility trading around macro events – and even in the absence of macro events.

5. Volatility arbitrage strategies

“Another strategy that we’ve been hearing about is global volatility arbitrage strategies. What managers who run these strategies are doing is looking at equity volatility, crude oil volatility and fixed income volatility against each other. Because they know that volatility is a mean reversion asset, when one asset class gets out of line relative to another they will put on a spread (long and short) in anticipation that these relationships will mean revert over time,” confirms Angelos.

One development that fixed income arbitrageurs who trade across the curve will no doubt welcome is the introduction of 2-year, 5-year, 7-year indexes , to supplement the current 10-year T-note volatility index.

“Every time we meet with potential users of TYVIX futures they ask if CBOE could list similar indexes in 2-year, 5-year, 7-year futures,” observes Obayashi. “Unlike equities, there’s a whole term structure for fixed income and depending on what part of the term structure you are looking at, there could be very different situations.

“For example, the short-end of the curve has been dormant for many years because of the Fed’s ‘hold steady’ position, whereas the 10-year has been very active. But that’s not always going to be the case. As interest rates go higher, the shorter end might become more interesting.

“Not only that, but managers would like the ability to trade volatility in one part of the curve against another,” says Obayashi.

“All of the strikes have to have reliable data, which means there has to be enough liquidity (in the underlying options) and if there is, then we can create a product. That’s the challenge to populating the whole term structure. If we can, we will,” concludes Angelos.

Moving forward, global fixed income managers are going to need to navigate carefully through rising interest rate environments and cope with rising bond market volatility. The TYVIX index could well act as their compass bearing to navigate through this higher volatility scenario and TYVIX futures could be an essential tool for managing risk and leveraging that volatility.

Futures trading is not suitable for all investors, and involves risk of loss. Options involve risk and are not suitable for all investors. Prior to buying or selling an option, a person must receive a copy of Characteristics and Risks of Standardized Options. Copies are available from your broker, by calling 1-888-OPTIONS, or from The Options Clearing Corporation at www.theocc.com. The information in this article is provided solely for general education and information purposes. No statement within this article should be construed as a recommendation to buy or sell a security or futures contract or to provide investment advice. Past performance does not guarantee future results. Visit www.cboe.com/TYVIX for more information. The VIX® index methodology is the property of Chicago Board Options Exchange, Incorporated (CBOE). CBOE is not affiliated with Applied Academics. CBOE , Chicago Board Options Exchange®, CFE®, CBOE Volatility Index® and VIX® are registered trademarks and TYVIX is a service mark of CBOE. CBOT is a trademark of CME Group, Inc. (CME). CBOE has, with the permission of CME, used such trademark in the CBOE/CBOT 10 Year US T-Note Volatility Index. CME makes no representation regarding the advisability of investing in any investment product that is based on such index. S&P® and S&P 500® are registered trademarks of Standard & Poor’s Financial Services, LLC and have been licensed for use by CBOE and CBOE Futures Exchange, LLC (CFE). Financial products based on S&P indices are not sponsored, endorsed, sold or promoted by Standard & Poor’s, and Standard & Poor’s makes no representation regarding the advisability of investing in such products. All other trademarks and service marks are the property of their respective owners.