Preqin recently surveyed over 50 managers of dedicated secondaries assets to find out about their activity in 2014 and to assess their outlook on the market for 2015. Patrick Adefuye analyses the key findings from these results.

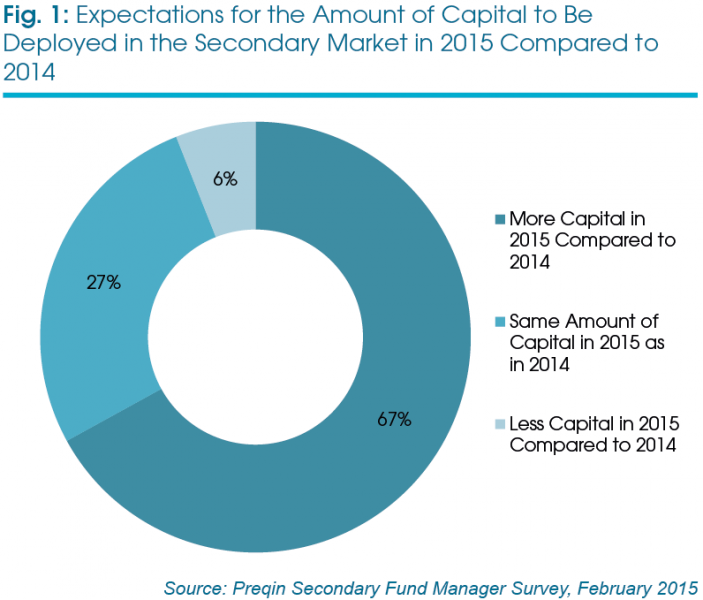

2014 was not only a record year for secondaries transaction volume, but has also been recognized as a record year for secondaries fundraising; an aggregate USD29bn was secured by the 27 secondaries funds that reached a final close during the year, the highest ever annual amount of capital secured. As a result, two-thirds of secondary fund of funds managers surveyed expect to deploy more capital in the asset class in 2015 compared to the previous year (Fig 1). A further 27% indicated that they expected to maintain their level of spend in 2015.

Pricing

It is clear that the secondary market is awash with capital, from the managers of secondaries funds, fund of funds vehicles with allocations to the secondary market and opportunistic institutional investors that are capable of gaining exposure to it. Inevitably, pricing is impacted by this strong demand for funds on the secondary market. Survey respondents indicated that the average price paid for buyout funds purchased on the secondary market was 90% of NAV, although this can be as low as 70% of NAV for mature assets.

In 2015, 45% of respondents indicated that they expect the price paid for buyout funds on the secondary market to increase (discount to narrow), while 48% expect it to remain the same. Given the expected increase in spend from the majority of respondents, strong pricing does not appear to be deterring buyers. Not only is there capital available to pay more (on a dollar basis, as well as on a percentage to NAV basis given that NAVs are also rising), there is also the willingness to do so, as the sentiment towards private equity and particularly buyout funds is positive given the strong environment for exits and distributions.

Leverage

One concern regarding the higher prices being paid for assets is the impact this may have on returns and that returns for assets bought on the secondary market in this current climate are likely to be lower than previous years. Anecdotally, it appears that secondary market buyers have turned increasingly to leverage to improve returns.

While the majority of fund managers that we spoke to did not use debt for acquiring funds (81%) or in funding a drawdown (89%) in 2014, debt is likely to play a bigger part in the secondary market in 2015. Thirty-four percent of respondents expect debt usage to increase in 2015, while the remaining 66% predict it will remain the same. No respondents expect the level of debt usage to decrease in the coming year.

Secondary Market Sellers

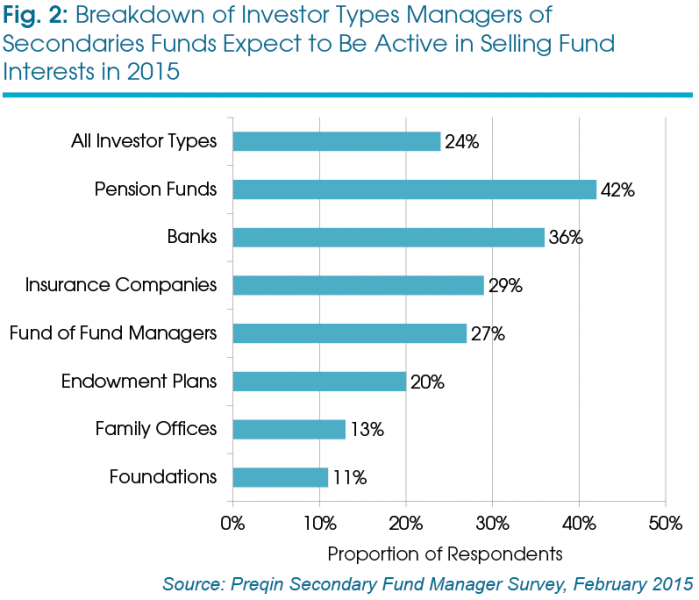

Managers of secondaries funds were asked to indicate which groups of investors would be selling funds in 2015, with pension funds cited by 42% of respondents, as shown in Fig. 2. Pension funds have become increasingly comfortable using the secondary market in recent years in order to achieve their desired portfolios. Banks and insurance companies (cited by 36% and 29% of respondents respectively) are also expected to be prominent sellers in the year ahead, both for regulatory reasons. Preqin’s research team is in daily contact with institutional investors in order to identify new sellers and update the investment plans of existing investors. Sellers are classified into two groups:

• Likely and opportunistic sellers that have pro-actively begun a process to sell funds or are generally open to approaches from buyers (and frequently have sold stakes before) and;

• Possible sellers, which are investors that are either over-allocated to a particular asset class and could consider the secondary market to rectify this, or investors that have put new investments on hold and therefore may be reviewing one or more of their manager relationships.

Analysis of the portfolios (specifically private equity) of likely and opportunistic sellers show interesting results that further illustrate their motivations for considering the secondary market. Fig. 4 shows the vintage year spread of the portfolios of likely and opportunistic sellers profiled on Secondary Market Monitor and shows that these investors are most exposed to funds that are 7-10 years old, accounting for 41% of all funds held by these investors.

Funds of vintage years 2005-2008 are considered the sweet spot for most secondary buyers, as funds of this age are typically at their realization phase returning capital to investors. Interestingly, likely and opportunistic sellers have significant exposure to funds that are 10 years old or more, representing 38% of funds held by these investors and therefore, in most cases, past their pre-agreed life-time. Collectively, these funds have a total of over USD100bn in remaining, unrealized value.

This is an extract from the Preqin Private Equity Spotlight | March 2015. This month’s edition looks in detail at the secondary market, as well as the latest industry news and data gathered by Preqin’s research teams.

Click here to read the full Spotlight, or visit our Research Center for more information and free research.