PARTNER CONTENT

Introduction

2023 was a remarkable year for financial assets. USA inflation rates started to decrease from 6.45% in 2022 to 3.5% in 2023 [1]. Both the equity and fixed-income markets saw a strong rebound after the significantly bearish conditions of 2022. The 30-year average fixed mortgage rates in the United States hit 7.79% in October 2023, the highest since the US housing market crash of 2008 [2]. At the beginning of the year, investors anticipated a drop in corporate profits due to the possibility of the US economy slipping into recession because of elevated borrowing expenses. However, the economy managed to avoid a downturn, even though US interest rates climbed to their highest point in 22 years. Economic growth surpassed expectations, and corporate profits in the US reached nearly record levels from July to September. Despite concerns about geopolitics affecting the markets, companies involved in artificial intelligence experienced significant growth as investors showed confidence in the technology’s potential.

Given the geopolitical unrest and rising interest rates, some analysts propose that financial markets may experience a prolonged period of instability, with market volatility becoming the new normal [3]. Financial experts are raising doubts about whether hedge fund managers possess the necessary experience to navigate these challenges. The prevailing theory is that funds led by managers who have weathered past crises are likely to fare better in the current turbulent climate.

Defining manager experience

Using AlternativeSoft’s analytical platform, we evaluated the performance of two sets of hedge funds during 2023. One group included funds managed by individuals who commenced their roles before 2007, experiencing prior high-interest rate conditions and the 2008 global financial crisis. The other group comprised funds managed by individuals who began their asset management after 2017, during a period marked by recovery from the global financial crisis and the era of near-zero real interest rates. We formed two equally weighted portfolios and compared their performance based on annualized alpha.

Results

The result of this analysis indicates a considerable outperformance of the portfolio of funds with a long history of asset managers. Those funds whose manager start date was before 2007, created 5.23% alpha (annualized) during 2023 against funds with newer manager start dates.

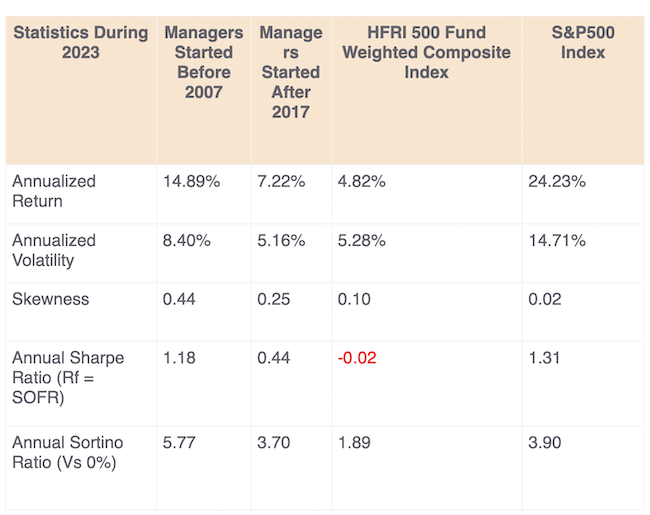

The risk and return statistics of the portfolios and their comparison with the sector index are shown in Table 1.

Table 1: Risk and Return Comparison of baskets of funds during 2023

Experienced fund managers have consistently outperformed their less experienced counterparts and across various return and risk measures. Throughout 2023, these seasoned managers have demonstrated superior returns and significantly higher risk-adjusted rewards compared to both the alternative portfolio and the sector index [4]. Their higher Sortino ratio indicates efficient portfolio operation, minimizing unnecessary risks that don’t yield commensurate returns. Additionally, these seasoned managers have achieved positive skewness, implying that there are more opportunities for potentially higher returns than for losses, which may be desirable for investors.

The second analysis

The second analysis uses the fund managers’ start date as a proxy for their experience to assess their performance in the new high-interest rate environment. This investigation employs a four-step process using the AlternativeSoft analytical platform as follows:

- 500 hedge funds were randomly chosen.

- Managers’ experience was determined by their tenure with the fund.

- Annualized alpha against sector performance was computed for each fund using the HFRI 500 Fund Weighted Composite index.

- Funds were ranked by annualized alpha and divided into ten equal groups (deciles).

The results show that the top decile (top 10% best performing) funds are on average around 5 years and 2 months more experienced than the worst decile. The highest rank has around 14 years of experience on average. This is the highest average amongst all groups. To test the significance of this difference a t-test [5] analysis was conducted on the difference between the means of the top and bottom deciles. The t-test result shows that the difference between the performance of the highest and the lowest ranks is statistically significant.

Relationship between manager experience and strategy

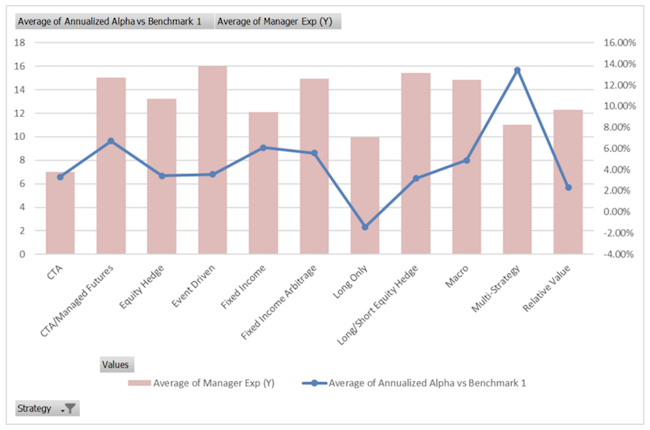

We examined whether there is a correlation between manager experience and alpha generation across different strategies. Chart 1 illustrates the Annualized Alpha against the HFRI 500 Fund Weighted Composite for each strategy from during 2023. Although the multi-strategy emerged as the top performing strategy in terms of Alpha, there isn’t sufficient evidence to attribute this solely to the managers’ experience.

Chart 1: Hedge Funds Average Annualized Alpha and Manager Experience Based on Different Strategies

Conclusion

AlternativeSoft’s analysis reveals that since the start of 2023, an equally weighted portfolio of hedge funds managed by managers who experienced the 2007-2009 financial crisis has significantly outperformed those managed by individuals who did not. When examining the broader correlation between hedge fund performance and managers’ start dates, significant differences are observed primarily at the extremes. The top 10% of best-performing hedge funds in terms of alphas in 2023, on average, have 5 years and 2 months more experience than the bottom 10%. A t-test confirms the statistical significance of this performance difference.

Two limitations affect this research. Firstly, there’s a potential for survivorship bias in comparing the performance of equally weighted portfolios, meaning that the funds with a long history of consistent managers that are still active are the most successful sample of funds. To mitigate this, the second analysis randomly selected funds to explore the relationship between performance and managers’ start dates. The second limitation is that an earlier manager start date does not necessarily translate into more experience.

[1] Source of data: Federal Reserve Bank of St. Louis https://fred.stlouisfed.org

[2] https://fred.stlouisfed.org/series/MORTGAGE30US

[3] https://www.economist.com/leaders/2022/10/06/a-new-macroeconomic-era-is-emerging-what-will-it-look-like

[4] HFRI 500 Weighted Composite

[5] The null hypothesis is that the means of the two samples (the top and bottom deciles) are not statistically different. A two-tailed t-test was performed with a confidence level of 95%.

![]()

AlternativeSoft is an award-winning quantitative analytics solution specialising in asset selection, portfolio construction, funds’ due diligence exchange and customised reporting.