Following on from last week’s extract from the Preqin Hedge Fund Spotlight | May 2015, which focused on the largest hedge fund managers in the industry, Simon Dhadwal takes an in-depth look at the ‘USD1bn Club’ of institutional investors allocating at least USD1bn to hedge funds, including the significance of this group, investment preferences and new entrants to the Club.

The past 12 months have seen mediocre performance generated by the industry as a whole and a handful of high-profile pension funds publicly announced their intention to scale back their hedge fund allocations. Nevertheless, assets under management (AUM) across the industry increased during this period and inflows from institutional investors continue to pour in. Such inflows are driven by a number of large institutional investors allocating at least USD1bn to the asset class – collectively, they make up the investor USD1bn Club. Here, we take a closer look at the investors that form this elite network, their current hedge fund preferences and plans within the asset class over the next 12 months.

There are currently 227 institutional investors that have at least USD1bn invested in hedge funds. This figure is an increase on the 203 investors that were identified as members of the USD1bn Club of institutional hedge fund investors in a Preqin study last year. Furthermore, growth is also evident in the aggregate capital invested in hedge funds by these larger institutions, which amounts to USD735bn, a 13% increase on the USD650bn allocated to hedge funds as of May 2014.

Who are the new entrants?

Over the past year, there have been 51 new entrants into the USD1bn Club. While insurance companies represented the largest proportion (22%) of new entrants last year, private sector pension funds make up the largest proportion of new entrants at this time, accounting for 29% of the group. One example of a private sector pension fund that has joined the ranks of the USD1bn Club is Novartis Pension Fund, which over the past 12 months has increased its allocation to hedge funds from 5% to 8.2% of its total assets. Foundations make up the next highest proportion (16%) of new entrants to the USD1bn Club. By geography, the vast majority (77%) of these new large hedge fund investors that have entered the club are based in North America, followed by 15% based in Europe.

Characteristics of USD1bn Club Investors

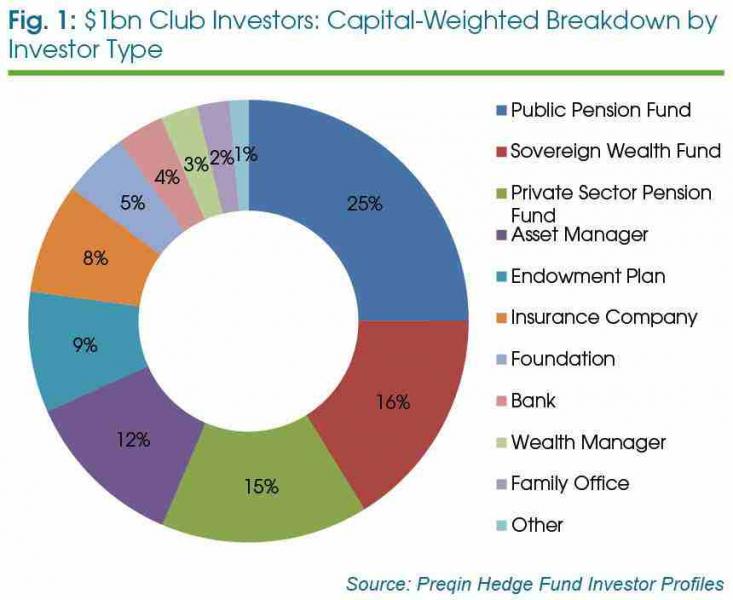

Public pension funds account for the largest proportion of capital invested in hedge funds (25%) by the USD1bn Club of institutional investors (Fig. 1), a figure which remains unchanged from the Preqin study conducted last year. Over this period, hedge funds saw a handful of high-profile pension schemes, such as US-based CalPERS and Netherlands-based PFZW, withdraw from the space. At least for now, this appears to be the case among the very few, with other investors and public pension funds filling these vacated spaces, such as Employees’ Retirement System of Texas and California State Teachers’ Retirement System (CalSTRS) allocating more than USD1bn to the asset class.

Moreover, sovereign wealth funds feature prominently among institutional investors with at least USD1bn committed to hedge funds and represent 16% of the total capital invested by this group. These funds continue to gain influence within the institutional hedge fund investment sphere, despite less than 10 such investors belonging to the roster of the USD1bn Club. One example of a sovereign wealth fund with over USD1bn allocated to hedge funds is Texas Permanent School Fund State Board of Education, which made its first investment in the asset class in 2008 as part of a strategic move to diversify its assets into the alternatives space.

Of investor capital held within the USD1bn Club, the largest proportion comes from investors based in North America (61%), up from 54% of capital invested in 2014. North America is home to some of the largest hedge fund managers in the world and the region remains significant in USD1bn Club hedge fund investment activity. While North America has witnessed more capital being poured into hedge funds by its largest institutional hedge fund investors, this is to the detriment of investor capital coming in from Europe. The proportion of hedge fund capital invested by Europe-based investors in the USD1bn Club has fallen from 28% last year to 21% as of May 2015, representing a USD30bn decrease in the capital allocations to hedge funds made by Europe-based USD1bn Club members since last year. Stricter regulatory reforms have posed major challenges for many of the largest Europe-based institutional investors and the amount of capital they can commit to hedge funds. This includes Basel III for banks and the AIFMD across European Union-based investors which only previously deployed capital to hedge fund managers based outside the region.

Moreover, Europe-based insurance companies have had to consider their allocations to hedge funds following Solvency II regulation that will levy capital charges of 49% on hedge fund investments. This directive is due to come into effect from January 2016 and has caused some of these insurance companies to weigh up moves to reduce their hedge fund allocations, or even exit the space entirely. This was the case with Norway-based insurance company, Storebrand, which withdrew from hedge funds in Q2 2014. This upcoming regulation may also have had some impact on the aforementioned reduction in the proportion of capital allocated by Europe-based USD1bn Club investors over the year, given that insurance companies account for 8% of total capital invested in hedge funds (Fig 1), with around half of these investors based in Europe.

Meanwhile, the proportion of hedge fund capital invested by Asia-Pacific-based investors in the USD1bn Club stands at 10%, a minimal decline from 11% last year. However, thanks to a fundraising revival in the Asia-Pacific market in 2014 (123 funds launched in 2014 compared with 90 funds in 2013) there are more opportunities for the largest investors to allocate capital to these newest funds, and could translate into aggregate gains in capital invested in the region over the course of the year. Rest of World regions see large sovereign wealth funds account for the entire 8% of total capital invested in hedge funds by USD1bn Club investors.

USD1bn Club investors vs. all other investors

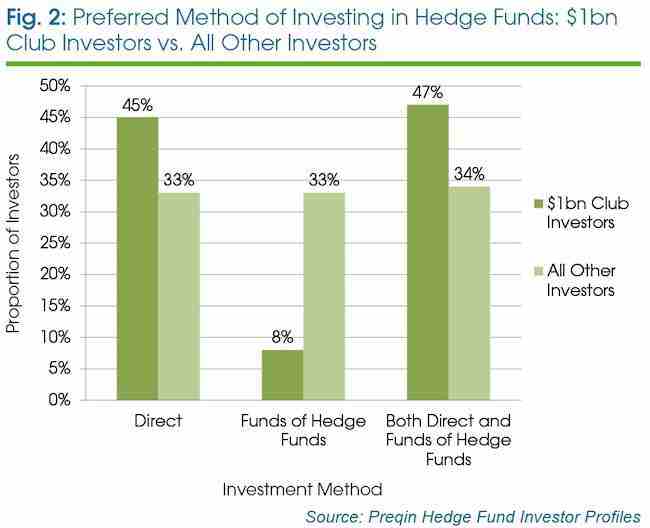

While it appears that investors outside the USD1bn Club favour utilizing solely multi-manager vehicles in their hedge fund portfolios equally to single-manager hedge funds, or using a combination of both structures (Fig. 2), investors in the USD1bn Club are more inclined to utilize a mixture of direct hedge funds and fund of hedge funds structures, accounting for nearly half of the USD1bn Club. Meanwhile, a small proportion (8%) of the USD1bn Club allocate to hedge funds solely through funds of hedge funds, principally as large investors tend to have the resources and experience available to them to manage hedge fund investments, bypassing the need to rely on the expertise of a fund of hedge funds manager. The experience and expertise of investors in the USD1bn Club compared with their smaller counterparts is made evident by a number of key statistics. On average, their first hedge fund investment was made 12 years ago while other investors, on average, entered the marketplace two years later. Moreover, USD1bn Club members tend to have a significantly larger number of hedge funds in their portfolio (typically 30) compared to the rest of the investor universe (8).

Furthermore, the USD1bn Club has increased its mean allocation of its total assets to hedge funds from 2014 (14.8%) to 2015 (15.9%), further demonstrating the positive sentiment which is driving long-term allocation plans for many institutional hedge fund investors. This is endorsed by the results of a survey conducted by Preqin in late 2014 to assess investors’ allocation plans in 2015: 84% of respondents signalled their intention to either increase or maintain their hedge fund allocations over at least the next 12 months.

Furthermore, institutional investors with at least USD1bn invested in hedge funds require an average track record of three years from a fund, which is lower than the minimum expectation of all other investors at 3.7 years. However, primarily due to policies preventing them from making outsized investments in a single fund, they have a higher minimum requirement for an underlying fund’s assets under management, which stands at USD695mn compared with USD515mn requested by other, smaller sized investors.

Investment plans for the next 12 months

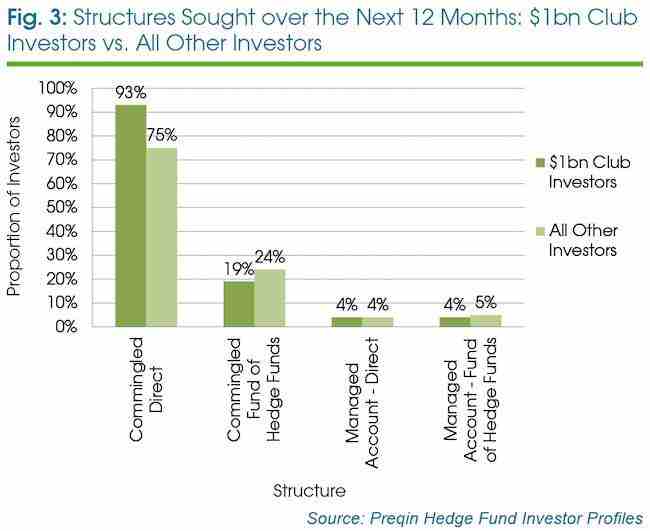

The appetite of investors in the USD1bn Club for hedge funds is further demonstrated by the future investment plans of some of the world’s largest investors looking to access the potential rewards and benefits associated with the asset class. To emphasise the shift of the USD1bn Club towards direct investments, Fig. 3 shows that a significant proportion (93%) of these investors are targeting a commingled direct method of investment over the next 12 months, an increase on 87% of such investors identified by Preqin in May 2014.

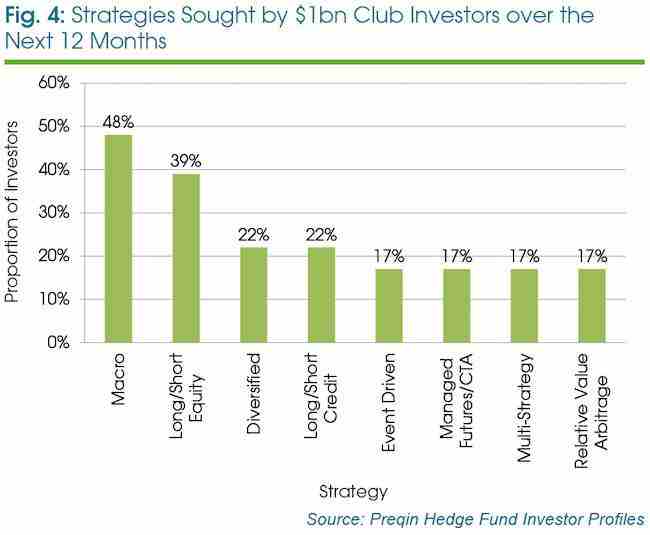

Among the USD1bn Club, macro strategies are the most sought-after hedge fund strategy over the next 12 months, as Fig. 4 illustrates. Political tensions and significant economic policies such as the end of quantitative easing in the US and Europe have created many potential opportunities for macro investors, which have propelled macro strategies into 48% of USD1bn Club investors’ searches. This is a notable reversal from this time last year when long/short equity was favoured by 50% of USD1bn Club investors (compared with 39% of searches in May 2015).

Meanwhile, long/short credit has gained more interest from these institutional investors over the past year, as the strategy currently features in the allocation plans for 22% of investors, compared with 17% in May 2014.

Outlook

Investors that form the USD1bn Club are significant players within the hedge fund industry, not just for the notable amounts of aggregate industry capital they manage, but also in the way they lead as key drivers of growth for hedge funds. Collectively, these investors allocate approximately USD735bn to hedge funds today, and their large ticket sizes make them valuable and desirable sources of institutional capital among hedge fund managers. These seasoned investors have been gaining exposure to hedge funds longer than their counterparts and continue to seek strong, risk-adjusted returns over the longer term. The rise in the number of USD1bn Club investors over the past few years shows that the appetite for major investment in the asset class remains strong, and with a healthy number of new entrants joining this elite group of investors, this appetite shows no signs of abating.

This is an extract from the Preqin Hedge Fund Spotlight | May 2015. To read the full spotlight newsletter, containing performance benchmarks, industry news and more, click here.