Whilst multi-strategy giants dominate flows, Luxembourg-based AlphaBee Asset Management has built a profitable niche, selecting curated hedge fund managers through methodical evaluation and deep research – though the spectre of the GFC informs every decision.

“We always have 2008 in the back of our heads,” says Co-Founder Frederic Guibaud. This defensive, even paranoid, mindset has shaped a fund-of-funds approach that deliberately restricts its investment universe whilst hunting for alpha in liquid arbitrage strategies that larger players routinely overlook.

The firm’s edge lies not just in finding emerging managers before institutional capital discovers them but in active portfolio construction that Guibaud claims doubles returns compared to passive allocation.

“We are able, through this active positioning and this active management, to add about 100% value,” he says, pointing to performance data that shows his flagship fund significantly outperforming an equal-weighted version of the same underlying strategies.

Defensive performance

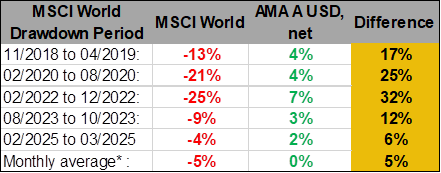

The results speak to this approach. AlphaBee’s flagship Multi Arbitrage fund has posted gains in two-thirds of months when the MSCI World declined. During February-March 2025’s 4% drawdown in global equities, the fund was up +2.4% net. Since launch almost eight years ago, the strategy currently stands at 6% annualised net returns with volatility controlled between 2-3%.

A comparison between AlphaBee Multi Arbitrage fund and MSCI, provided by the fund

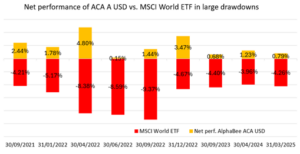

The firm’s Commodity Arbitrage fund, launched in May 2021, has generated +14.5% annualised net returns since inception, compared with the HFRI Macro Commodity Index’s 4.7% over the same period.

Both strategies performed strongly during 2022’s market turmoil, posting net gains of 7.6% and 12.9%, respectively, when traditional portfolios struggled and lost close to -20%.

AlphaBee runs the two Luxembourg Sicav-SIF funds constructed from within a universe exceeding 10,000 alternative strategies, winnowed down to focused portfolios of 10-20 positions. The firm’s five-person investment team commits significant personal capital alongside external investors, reflecting its origins as a seeding single-family office that opened fully to external capital in 2021.

Barriers to entry analysis

Like equity/credit analysts applying Michael Porter’s five forces framework, AlphaBee assesses hedge fund strategies for sustainable competitive advantages. “It’s a little bit the same with any hedge fund strategy,” Guibaud explains. “When there is alpha, other managers will come up with the same or similar strategies trying to capture that alpha.”

The firm spotted commodity arbitrage opportunities in 2018 when volatility in the sector had been suppressed for years, investing in managers “that nobody knew,” who were “below $100m in assets under management at the time”. Those early investments proved prescient as subsequent events ranging from Covid-19 to Ukraine’s invasion created the market dislocations that arbitrage strategies require, and AlphaBee Commodity Arbitrage fared well in both scenarios

A comparison between AlphaBee Commodity Arbitrage fund and MSCI, provided by the fund

Credit strategies or other strategies that could become illiquid under adverse market scenarios, as well as those exhibiting important negative tails in their expected returns, are excluded. Traditional global macro and typical equity long-short strategies are also excluded, with exceptions made only for proven specialists operating in some niche where the alpha can be found. AlphaBee currently backs a North American upstream market-neutral energy manager who benefits from reduced analyst coverage in fossil fuels. “Nobody wanted to be a fossil fuel analyst anymore,” the manager told them. “The opportunity set is great for us.”

Timing volatility cycles

Despite geopolitical headlines suggesting market turbulence, Guibaud argues current commodity volatility remains overall historically low – a counterintuitive position that he believes creates conditions for future opportunities.

“At one point, volatility will mean revert, and it will probably overshoot as it has done in the past,” he says. “When it does, we should be able to profit as we have done in the past.”

However, he distinguishes between productive volatility driven by fundamental uncertainty and the current environment where unpredictability stemming for example from ongoing and shifting tariff threats which can override the fundamental analysis that arbitrage strategies depend upon.

The firm’s concentrated focus – “we’re three full-time people only doing specialised hedge fund analysis day in, day out” – allows for intensive due diligence including mandatory on-site visits, as well as analysis of the hedge funds’ ecosystems, to assess both quantitative performance and operational risks. They are supported by a 20+ strong team which operates the funds in Luxembourg.

“The devil is in the details,” Guibaud says of their approach. “We’re looking for alpha, but if the alpha is in an emerging manager, that’s even better because then we can negotiate maybe capacity, or founders’ share class fees, and we will be early in the alpha wave. Because every alpha has a wave – after a few years, it will crest, and then it will come down. We want to be early and ride the wave up.”

While mega-funds continue to dominate hedge fund flows and startup numbers decline, a quiet revolution is taking place in the industry’s margins. Investors are increasingly hunting specialised managers who can fill precise portfolio gaps – from employee wellness to sustainable living.

These emerging niche strategies aren’t just surviving in the shadow of multi-strategy giants; they’re thriving by targeting unexploited market inefficiencies and emerging secular trends. The series explores how these specialised funds are carving out their space in an industry typically associated with scale, examining their unique value propositions, challenges and the investors backing their vision.