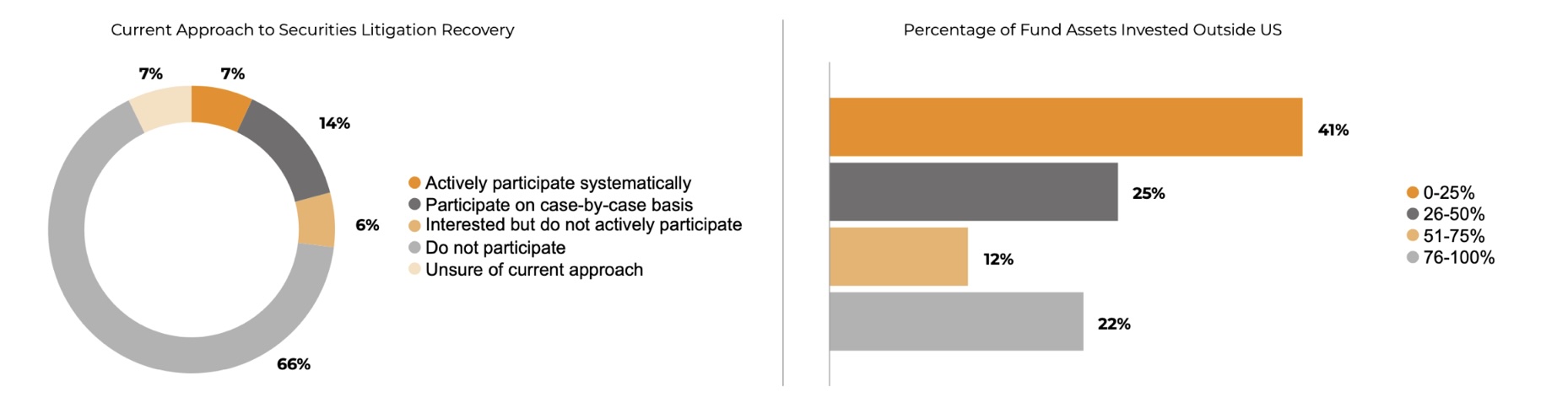

In an industry obsessed with finding edge, a multi-billion dollar opportunity lies largely unclaimed. Despite record settlements and straightforward economics, just 7% of hedge funds systematically participate in securities class action recoveries. A further 14% participate case-by-case, meaning four in five funds leave money on the table entirely.

Here’s what that actually means. When a company like Volkswagen or Apple misleads investors and gets caught, it settles by creating a compensation fund for affected shareholders. Hedge funds that owned the shares during the fraud period are entitled to file claims. No testimony required. No legal exposure. Just proof you held the stock and suffered losses.

Yet most eligible funds don’t bother filing.

The numbers tell a striking story. Investors recouped $5.2bn in US settlements in 2024, whilst international recoveries surged to $529m in 2023 and $483m in 2024 (over four times 2022 levels). Major settlements included Apple ($490m), Alibaba ($433m) and Alphabet ($350m). Most funds with exposure filed no claims.

“The beautiful thing about claim filing in the US is, if you do have an eligible claim, you will get money,” says Michael McCreesh, managing director and head of SS&C Battea, which helps institutional investors capture these recoveries. “And the more matters you file claims in, the more money you will get. It is that simple.”

So why don’t they?

Recent Hedgeweek research surveying over 100 hedge fund managers reveals the barrier isn’t awareness or economics but psychology. Nearly half of non-participants cite “lack of expertise” as the primary reason. Yet two in three funds that do participate have simply outsourced the entire process to specialised administrators.

“Funds don’t need legal expertise,” McCreesh explains. “They need to make one decision: engage a provider who has that expertise.”

The expertise barrier appears largely imaginary. Among systematic participants, implementation varies widely: 27% use third-party providers exclusively, 36% employ hybrid models and 9% handle everything internally. The diversity suggests multiple straightforward approaches work equally well.

The international opportunity looks even more puzzling. One in three surveyed funds invest the majority of assets outside the United States, where recovery rates can reach 30-40 pence per dollar versus 2-15 pence domestically. Yet these internationally-focused managers show no higher participation rates.

McCreesh acknowledges past challenges in European litigation created warranted scepticism. “Years ago, the vast majority of litigation was filed under novel laws before anyone really knew what they were doing.” However, he notes dramatic improvements: “The lawyers and funders have improved dramatically in recent years. It is a night and day difference for the better in some jurisdictions now.”

Here’s the part that should really get attention. Settlement funds operate on a pro-rata distribution model. When eligible investors don’t file claims, that money often gets redistributed to those who did file. Non-participants effectively subsidise their competitors.

When researchers informed survey respondents of this mechanism, only 7% said they would immediately assess their unclaimed amounts. Nearly one in three cited “other priorities regardless of potential amounts.”

“Hedge funds must realise that should they not file, the money owed to them will just go to others,” McCreesh says. “If you are not filing, then your competitor is likely receiving your share.”

What actually triggers funds to start participating? “We see client onboarding after the client has experienced an outsized loss,” McCreesh notes. “Another common occurrence is related to new staffing. Often, an employee has seen recoveries achieved through their former employment and is eager to bring that extra alpha to their new employer.”

There’s no minimum fund size required. “There is no minimum viable AUM. Losses and recoveries are relative. We encourage all funds to file claims.”

As performance fees compress and investors demand better net returns, every source of incremental value matters. Securities litigation recoveries represent one of the few additional return sources requiring no investment risk, no capital deployment and no market timing skill.

The question for the 93% who abstain: is organisational inertia worth leaving money on the table when your competitors are picking it up?