PARTNER CONTENT

By Robert D Stock, PhD, Axioma Analytics Research, SimCorp

Passive investing in index funds has been enormously popular and for good reasons. In fact, total passive assets surpassed active assets by early 2024, according to Research Affiliates1. But the popularity of systematic index-based investing may also create unintended effects, including reduced diversification and amplified liquidity and volatility risks. In this article we explore whether other investment opportunities have arisen in the wake of the passive juggernaut.

Is there a factor to capture this passive investment risk?

This research examines how different investment flows interact with market structure, providing insights valuable for both active and passive strategies.

We selected the Axioma US5.1 factor risk model for this study, which covers hundreds of major ETFs. Since ETFs are usually passively managed, we used the percentage of a stock’s market cap held by ETFs as a proxy for exposure to Passive Investment Risk.

In the period of consideration, January 2014 through July 2025, we further limited our universe to the top 20% of assets in the US market by capitalization, so that we are only considering assets that plausibly could have been chosen by an ETF but for some reason are overlooked. Very small stocks will generally have no ETF ownership, and we didn’t want our analysis to become simply a measure of Size. Instead, we wanted to see if the performance of otherwise-similar stocks differs substantially due to a low versus high percentage of ETF ownership. We then checked if some distinguishing factor characteristic of these stocks could proxy for the ETF ownership risk, or if ETF ownership could represent a new risk factor.

Procedure and results

1) At the end of each month, screen the universe of US stocks for the top 20% by market cap giving us a pool of around 2,000, with minimum market caps in the $5 to $10 billion range (called “ALL”).

2) Compute their percentage ownership by domestic ETFs. Define “high” ETF ownership as >10% of market cap (over the period, average ownership increased steadily from 2% to nearly 5%).

3) If this finds less than 100 High ETF stocks, lower the threshold until we have 100 in the portfolio (there were fewer than 100 stocks exceeding the threshold until mid-2019, growing to over 500 by mid-2024).

4) Find the same number of stocks with the lowest ETF ownership, using smallest market cap as a tiebreaker, for the “Low ETF” portfolio.

5) Equally-weight stocks in both portfolios and let run until the next monthly rebalance.

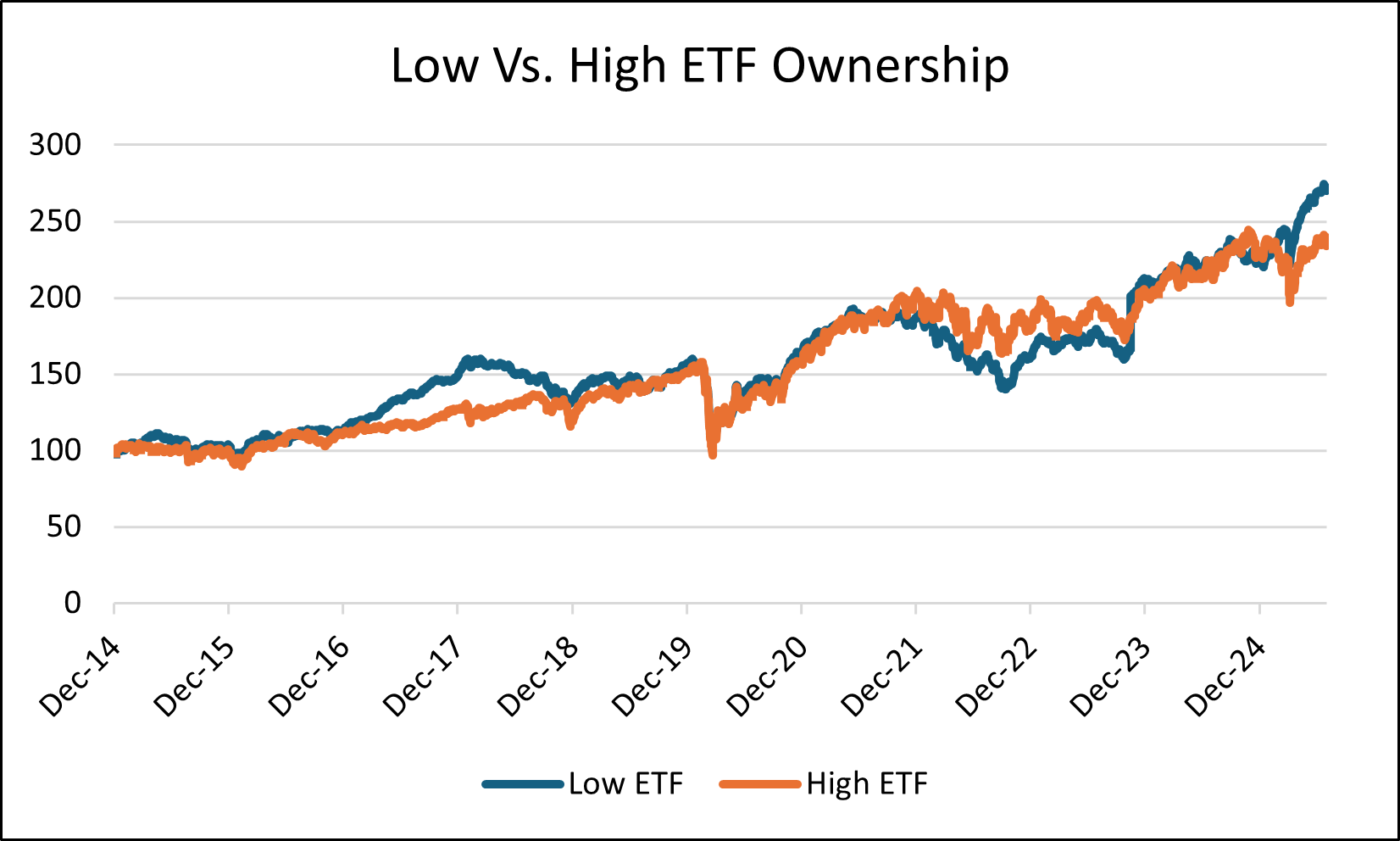

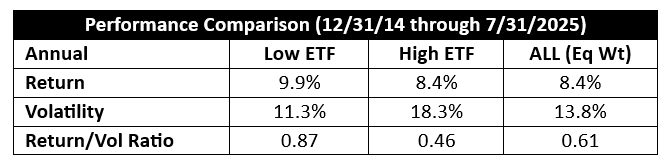

Figure 1 shows the growth of the two portfolios, and Figure 2 summarizes the performance and compares it to the whole top 20% market cap universe.

Figure 1: Growth of $100 for Low and High ETF ownership, rebalanced monthly

Figure 2: Annualized performance

Figure 2 shows that the High ETF ownership subset has lower performance than the whole large stock universe (having higher risk for the same return), while the Low ETF subset is substantially better on both counts, supporting the case that passive investing can increase volatility risk and reduce diversification.

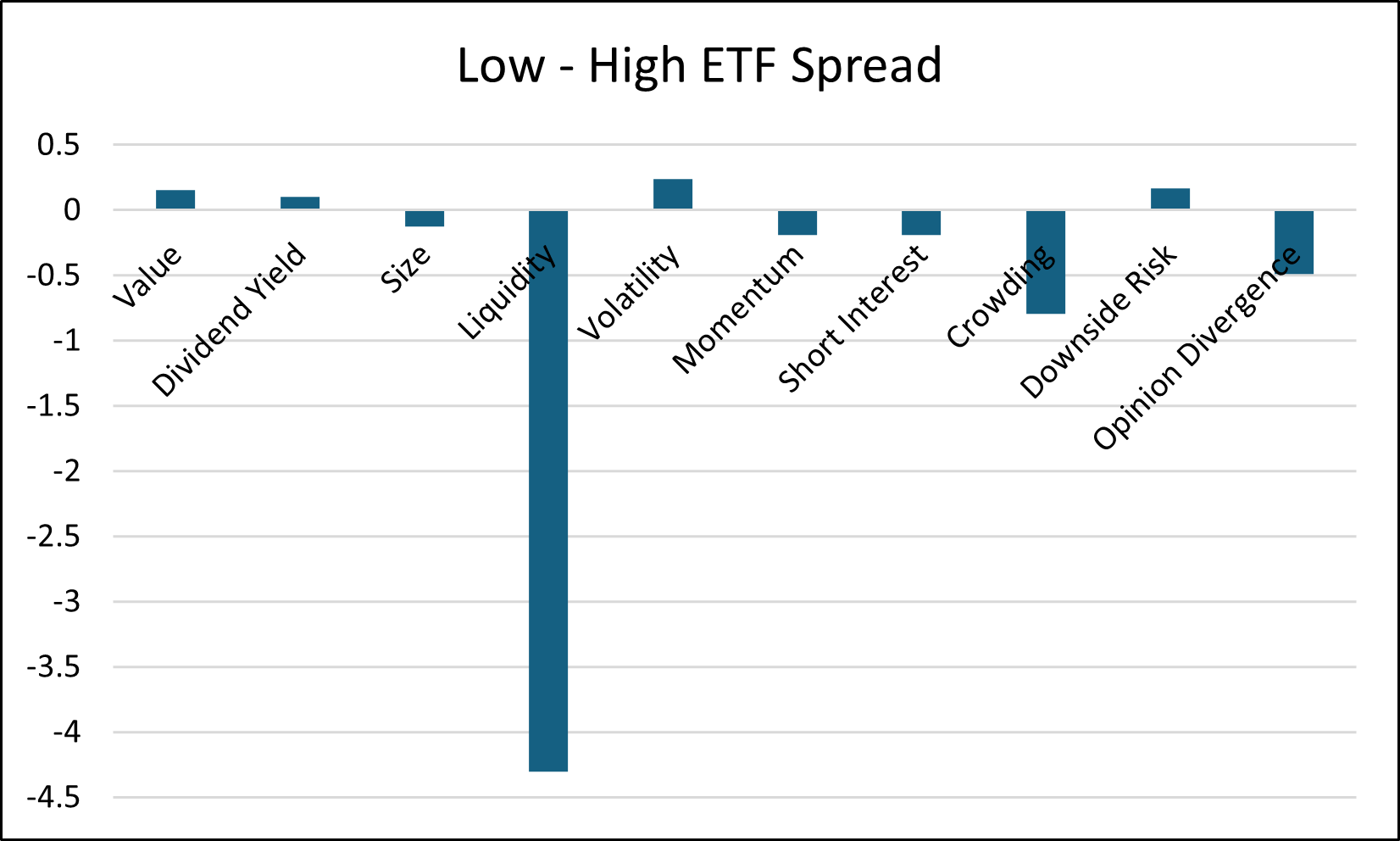

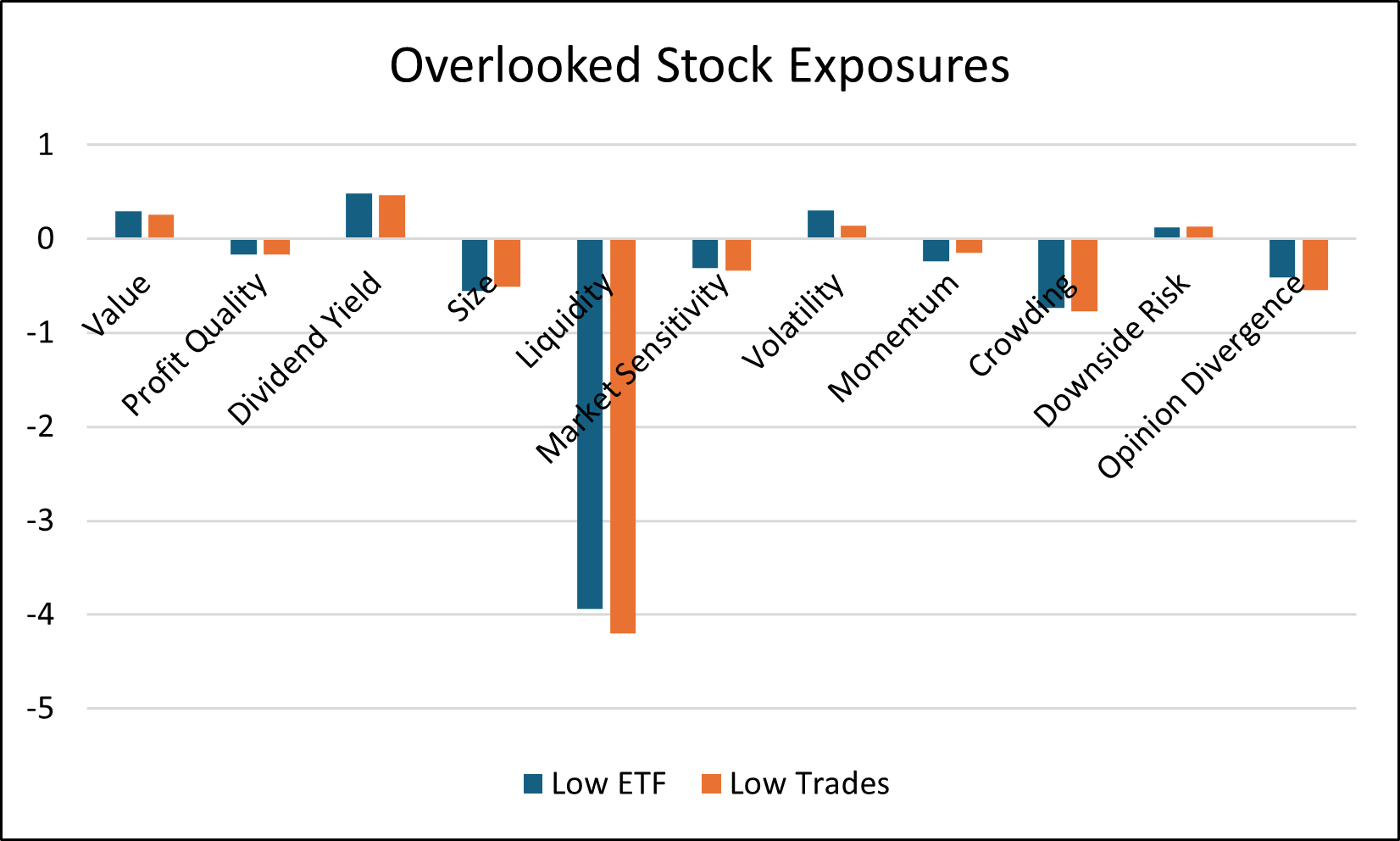

What do these stocks look like? Figure 3 shows the average factor exposure spread between the two portfolios (differences smaller than 0.1 are omitted).

Figure 3: Average factor exposure spread

Source: Axioma US5.1 risk models

While most differences are small, the overlooked stocks clearly are far less liquid and less owned by hedge funds, but have a small Value tilt. This makes their outperformance even more interesting because this factor spread is a substantial drag on performance, indicating stock-specific alpha.

A new factor?

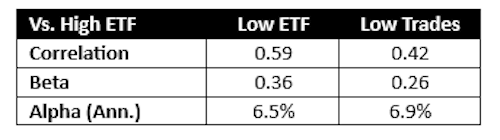

Not quite. ETF ownership concentration creates measurable performance and volatility effects but these are already largely captured by the Axioma Liquidity factor. It is a blend of three descriptors, one of which is “Percent of Days Traded” over the last 3 months; this is just a flipped version of the “zero_trades” factor of Liu2, which is the number of days with zero trading volume over some window. Figure 5 shows the average factor exposure of a “Low Trades” portfolio (screened on low Percent of Days Traded instead of Low ETF Ownership) over the same period and with the same number of stocks. The comparable alpha and beta of these overlooked stock portfolios to the riskier High ETF exposure portfolio is in Figure 4.

Figure 4: Comparison of overlooked stocks to High ETF ownership stocks

Figure 5: Average exposures of overlooked stocks

Not only is the factor exposure very similar, but the return profile has a 0.82 correlation, so the “anomaly” of Low ETF exposure is essentially captured by low Percent of Days Traded exposure.

Caveat emptor

While the Low ETF portfolio looks promising, ETF ownership also provides advantages: ETF demand, at least during a “normal” market, enhances liquidity for such stocks. This implies that Low ETF stocks, which correspond roughly with the “zero trade” stocks, can sometimes fall prey to their own idiosyncratic “flash crashes” because literally nobody is trading them. In several cases, for members of the overlooked stock portfolio, the price could drop one day nearly -100%, only to recover the next day by millions of percent! (and that’s why monthly returns were used for this analysis).

What are the implications of this study?

Passive managers should be aware of concentration risk with index construction while active managers may find opportunities in the more liquid stocks overlooked by ETFs. Overall, monitoring ETF ownership risk and its associated dynamics is important and can be assessed through the lens of a robust risk model.

1 Brightman, C. and Harvey, C. R., Passive Aggressive: The Risks of Passive Investing Dominance (July 8, 2025). Available at SSRN: https://ssrn.com/abstract=5259427.

2 Liu, W, A liquidity-augmented capital asset pricing model, Journal of Financial Economics 82:3 (2006).

Robert D Stock PhD, Axioma Analytics Research, SimCorp – Bob develops Axioma factor risk models for SimCorp. After earning his undergraduate degree in Physics from Princeton and his doctorate in Physics from Carnegie Mellon, Bob worked for nearly a decade at MIT’s Lincoln Laboratory in the Directed Energy Group, performing simulations and analysis of high energy laser beam propagation through the atmosphere for missile defense applications. Bob then served the Ultra-High Net Worth segment for 15 years, first as a Quantitative Researcher for a boutique outsourced-CIO where he developed the majority of the firm’s intellectual property for hedge fund analysis, risk management, forecasting, and asset allocation. Subsequently, he served as a systematic portfolio manager for a large Trust before joining Axioma (now part of SimCorp) in 2022.

Robert D Stock PhD, Axioma Analytics Research, SimCorp – Bob develops Axioma factor risk models for SimCorp. After earning his undergraduate degree in Physics from Princeton and his doctorate in Physics from Carnegie Mellon, Bob worked for nearly a decade at MIT’s Lincoln Laboratory in the Directed Energy Group, performing simulations and analysis of high energy laser beam propagation through the atmosphere for missile defense applications. Bob then served the Ultra-High Net Worth segment for 15 years, first as a Quantitative Researcher for a boutique outsourced-CIO where he developed the majority of the firm’s intellectual property for hedge fund analysis, risk management, forecasting, and asset allocation. Subsequently, he served as a systematic portfolio manager for a large Trust before joining Axioma (now part of SimCorp) in 2022.