The average time taken for private real estate funds to reach a final close so far this year is the longest it has ever been. This extract from Preqin Real Estate Spotlight: August 2015 explores the key trends that emerge when comparing time on the road to fundraising success and past performance in an increasingly competitive market.

The real estate fundraising landscape remains a competitive one, despite increasing institutional demand for exposure to the asset class. Preqin’s Real Estate Online contains detailed profiles for over 4,900 private real estate funds worldwide, which include information on strategy and geographic preferences, fundraising, known investors, manager track records and more. Using this fundraising data, we can see that in 2012, 274 private real estate funds closed raising USD72 billion in institutional capital commitments. However, by 2014, the number of funds closed was down by 15 per cent, while the amount of capital raised had increased by 45 per cent. Correspondingly, the average final close size of a private real estate fund nearly doubled from USD252 million in 2012 to USD444 million for funds closed in 2014. This trend appears to be continuing: 95 private real estate funds have closed so far in 2015, raising USD69 billion and with an average close size of USD728 million – the highest on record.

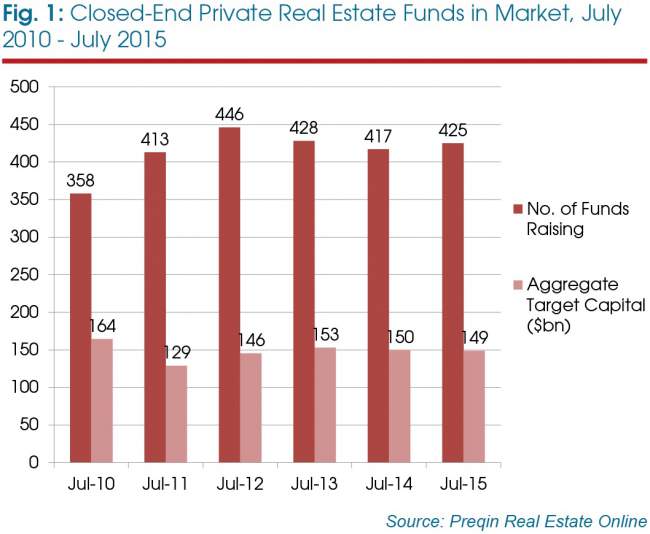

With capital concentration increasing year-on-year, often among larger and more experienced managers, fund managers need to differentiate themselves in order to secure commitments. As shown in Fig 1, the level of competition in the real estate fundraising market remains extremely high; 425 funds are in market, seeking aggregate capital commitments of USD149 billion, as of July 2015.

Time taken to reach a final close

In this competitive environment, the time taken for managers to reach a final close has increased from an average of 14.2 months in 2010 to 19.5 months in 2014, albeit with a reduction in average close time in 2013. So far in 2015 the average time taken to reach a final close stands at 19.8 months – a record high for closed-end real estate vehicles. Notably, in recent years, the proportion of funds raising capital for over two years has increased; between 2010 and 2013, 21 per cent of vehicles, on average, were in the market for 25 months or more, with this proportion rising to 31 per cent and 35 per cent for funds closed in 2014 and 2015 YTD respectively (Fig 2). Correspondingly, in 2015 so far, the proportion of vehicles reaching a final close in under one year is the lowest it has been at any point since 2010, with only 28 per cent of vehicles closing in 12 months or less, indicative of the difficulties some managers are experiencing in closing vehicles quickly. Among the fastest vehicles to close in 2015 so far is Matan Fund V, which held a final close on USD100 million in April, one month after its launch. The fund will invest in warehouse and industrial properties in the Washington, DC area.

The size and reputation of fund managers play an important role in the fundraising process, with the larger players exerting significantly more influence on the marketplace than their smaller counterparts. Not only do the larger fund managers have more resources to put towards marketing their vehicles, they can often make use of existing investor relationships to attract new commitments and utilize their brand name to extend their network of institutional investors. As the amount of capital fund managers have raised in the last 10 years decreases, the longer, on average, it takes to reach a final close; for funds raised since 2013, the 10 largest fund managers, by capital raised in the last decade, reached a final close in an average of 14.7 months, compared with 19.2 months for the next 40 fund managers and 18.1 months for managers outside the top 100.

While a fifth of Asia-focused vehicles closed relatively quickly, over a third struggled to gain momentum and were on the road for over two years. Everbright Ashmore Beijing Tongzhou Real Estate Fund was on the road for just four months after its launch at the end of October 2014, reaching a final close on CNY 3.5 billion. The fund aims to provide capital to develop Beijing’s Tongzhou Canal area into a major industrial and mixed-use development zone that will house finance, technology and culture sectors. While it is more pronounced for Asia-focused funds, this trend is repeated for both North America- and Europe-focused funds. A quarter of all North America-focused real estate vehicles closed after two years of fundraising, with this proportion rising to 29 per cent for Europe-focused funds.

Fundraising momentum

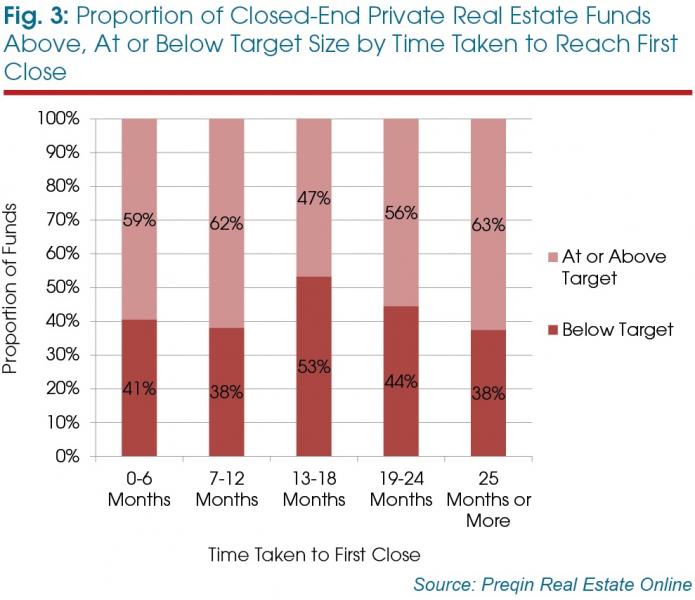

The majority of funds closed since 2010 (61 per cent) achieved their first close within six months of launching, with only 12 per cent of vehicles taking longer than one year to hit this mark. However, does taking longer to reach a first close lead to a less successful fundraise? Fig 3 shows that this is not always the case. While 59 per cent of funds that reached a first close within half a year met or exceeded their initial target, the same can be said for funds reaching first close in 7-12 months (62 per cent), 19-24 months (56 per cent) and funds that reached first close over two years after their initial launch (63 per cent).

With fundraising an increasingly long process for many firms in recent years, a third of firms marketing funds have already been on the road for over 18 months, with a fifth in market for over two years. Gaining some momentum through a strong first close is important for fund managers; funds that are able to reach a first close quickly are often able to gain further traction in the marketplace. A fifth of fund managers that reached a first close within six months of launching reached a final close in the following six months. Furthermore, smaller proportions of fund managers reaching first close quickly spent more than a year marketing their funds than those funds that reached a first close in more than half a year. This displays the importance of achieving the milestone relatively quickly as it becomes demonstrative of a manager’s ability to attract capital and the credibility of their strategy to potential investors, many of whom will prefer to invest after a fund’s initial close.

Success in achieving fundraising targets

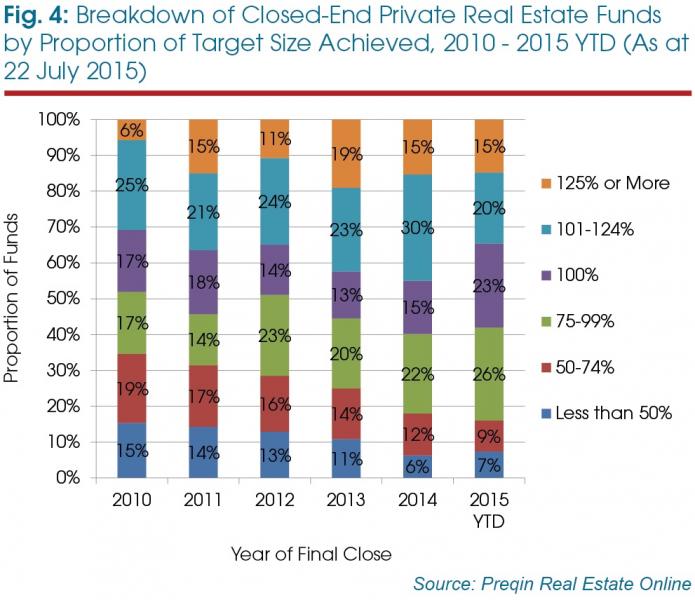

While some funds are experiencing considerable success with fundraising, others are struggling to gain a foothold in this competitive environment. The proportion of private real estate funds that have closed at or above their target size increased from 49 per cent in 2012 to 60 per cent in 2014 (Fig 4); however, a quarter of funds on average have secured less than 75 per cent of their target since 2010. So far in 2015, 58 per cent of funds have closed at or above their target size, including 15 per cent that have raised 125 per cent or more of their initial capital target.

Of all funds to close in 2015 so far, Vier Metropolen has raised the largest proportion of its initial target size. The fund is one of the first to be raised in accordance with Investment KG, a new pooling vehicle under the Kapitalanlagegesetzbuch (KAGB) in Germany. The opportunistic fund, raised by Bamberg, Germany-based Project Investment, reached a final close in February 2015 on EUR200 million, doubling its initial EUR100 million target. Of the larger vehicles to complete a final close this year, Tristan Capital Partners’ European Property Investors Special Opportunities 4 targeted an initial EUR950 million, but ultimately raised EUR1.5 billion for value added and opportunistic investments in logistics, office, retail and residential properties in the deeper and more liquid markets of Western and Central Europe.

The previous performance of a fund manager has little correlation to the amount of time spent in market for a follow-on fund. While fund managers that have a top-quartile fund spend the least amount of time, on average, raising their successor vehicle (17.5 months), fund managers with bottom-quartile real estate funds raised their successor funds quicker than those with second- and third-quartile predecessor funds.

However, the performance of previous funds has a significant impact on the fundraising success of the follow-on vehicle. For private real estate funds closing on or above target, 45 per cent were follow-up offerings to a top-quartile fund, while just 13 per cent had prior funds ranked as bottom quartile. It is interesting to note that, given how challenging it is for firms to raise capital in the current market, most firms that do close funds are the previously strong performers; of the firms that are closing below target, a significant 57 per cent still had top- or second-quartile predecessor vehicles, suggesting that many of the third- or bottom-quartile fund managers have struggled to successfully raise a follow-on vehicle.

Outlook

Competition for capital is intense, and as a result fund managers are spending more time on the road marketing their vehicles in order to attract sufficient capital to close these funds. Although the average length of time a real estate fund manager spends on the road has increased to its highest point (19.8 months), there is a large range surrounding the mean, with some very successful funds closing within a few months of launch and others taking much longer. A strong determinant of the length of time to raise a real estate fund is the size and brand of a fund manager, with the larger managers over the last decade securing capital from investors significantly faster than their peers.

Investor appetite for real estate remains strong, but with so many funds being marketed, investors can be selective in their choice of commitments. Aside from a handful of the biggest players, fundraising is a long process for most, but for those managers that can demonstrate a strong track record, a clear pipeline of potential deals and support from existing LPs, there is certainly the institutional demand for them to be very successful.

This is an extract from Preqin Real Estate Spotlight: August 2015. Click here to read the full newsletter, which also features an examination of the private real estate investor landscape in Chicago, a fundraising update, key statistics on Southern Europe-based investors and more.