Ryan Sullivan, Vice President, Investor Services at Brown Brothers Harriman & Co highlights key components of the DOL rule that may spur growth in ETFs and how this regulation will influence existing ETF trends.

On 6 April, 2016 the Department of Labor (DOL) proposed the final version of its fiduciary rule which aims to broaden the definition and scope of fiduciary protections that have been in effect for Employee Retirement Income Securities Act plans since 1974.

Under the existing rules, financial advisors can be incentivised to sell clients products with higher fees and questionable returns, creating a potentially conflicted advice model for investors. The DOL’s proposal requires all financial advisors to act in the best interest of their clients instead of prioritising their own bottom line. The proposed rule will apply to any financial advisor offering advice that is “individualised or specifically directed to a plan sponsor, plan participant, or IRA owner for consideration in making a retirement investment decision.”1

If approved, the final DOL rule will likely continue to propel trends that have been underway for years, such as the migration of assets from high to low-cost products and the growth of robo-platforms. As a result, ETFs are likely to be one of the rule’s key beneficiaries. While ETF growth has normalised in recent years, we believe that the rule could drive ETF assets back to a growth rate between the products’ current three and five year CAGR range of 8per cent–15per cent. This would result in ETFs adding another USD1.5 trillion in net new assets over the next five years.

Here, we highlight key components of the DOL rule that may spur growth in ETFs and offer our thoughts on the influence this regulation will have on existing trends in the ETF industry.

COMPONENTS OF THE DOL RULE MAY SPUR ETF GROWTH

EXISTING TRENDS WILL BE ACCELERATED BY THE DOL RULE

ASSETS MOVING TO LOW-COST PRODUCTS

The proposed DOL rule examines a few aspects of fees worth mentioning, particularly the fee amount and fee structure of investment products that advisors use in client accounts. The final proposal still allows for the use of higher-cost products, but advisors must prove and support the usage of such products to comply with the best interest standard.

Leveraging lower-cost products may allow advisors to better manage their regulatory risk while seeking to serve the client’s best interest. In fact, ETFs are regularly used to help keep costs down for investors in fee-based accounts. Investors in fee-based accounts are still charged the underlying expenses of the funds chosen by their advisor.

As the management fees of ETFs are typically lower than mutual funds, they can help reduce that management expense. A recent wealthmanagement.com survey found 45 per cent of advisors still use commission-based accounts, suggesting a large segment of advisors could still move to fee-based accounts and lower-cost products in substantial volume, further driving advisor-managed assets into ETFs.2

Compensation via ‘distribution fees’ from the fund to an advisor or platform received much scrutiny from the regulator. This compensation model can take different forms, either through the usage of a 12b-1 fee or through sub-TA or sub-accounting fees, typically paid to third-party distributors for record-keeping and other services performed for clients. While the DOL rule allows for the continued use of some of these compensation models, advisors must now monitor and report on the retirement plans they service as these payments can be prohibited at certain participant sizes. Mutual fund share classes charging 12b-1 fees today may be increasingly phased out by financial advisors managing retirement assets in favor of less costly ETFs.

ACTIVE MANAGERS EXPLORE THE ETF MARKET

While ETFs have historically been seen as passive strategies, that view is quickly becoming outdated. In the last two years, a number of brand-name active managers have entered the ETF market. Over this time, the industry has seen an explosion of innovation in strategies and product design. If the DOL rule further promotes the current shift in assets from high to low-cost products, it may present an opportunity for managers to add ETFs to their investment product menu and tap into different asset pools and distribution channels. Factoring in that the DOL proposal still allows for the usage of proprietary products, the industry may continue to see large, institutional organizations enter the ETF market and distribute them through their own advisor networks.

Smart Beta

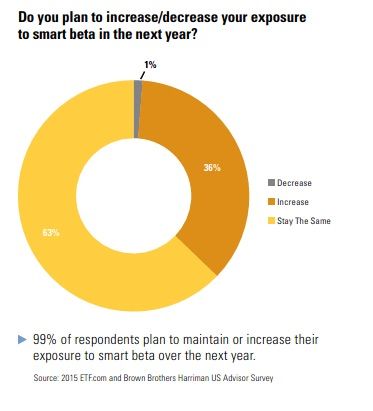

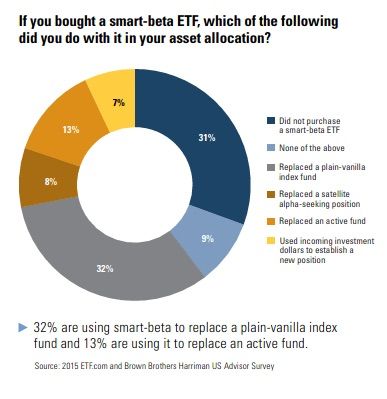

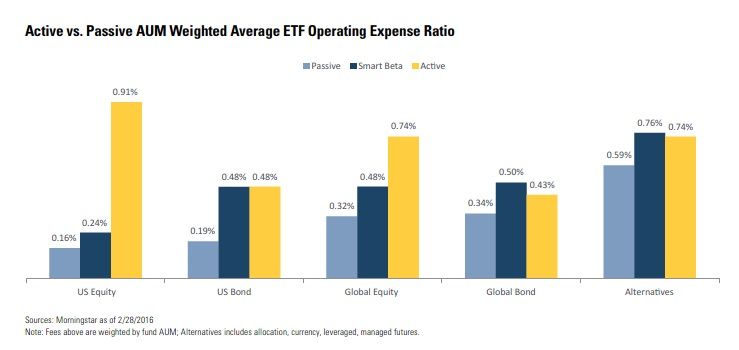

Smart-beta strategies continue to prosper and have gained traction quickly in advisory channels. A recent survey sponsored by ETF.com and Brown Brothers Harriman (BBH) showed that 13per cent of advisors are replacing active funds with smart-beta ETFs and another 32 per cent of respondents are trading traditional market cap weighted passive funds for smart-beta ETFs. Ninety-nine per cent of respondents in the survey had plans to either maintain or increase their current smart beta exposure in 2016.3 Active managers have noted the success and opportunity these strategies offer and the increase in competition from brand-name firms entering the ETF space in recent years has driven smart-beta fees even lower.

Active ETFs

Currently, the active ETF universe remains only a fraction of the larger ETF market, making up only about 1per cent of total ETF AUM.4 However, this segment has seen outsized growth in recent years through new entrants and new product offerings from existing sponsors. While these products retain a price premium over traditional, passive ETFs, they still provide a low-cost alternative to other actively managed products, which may help advisors adhere to their best interest standard. This area may still present an opportunity for active asset managers looking for an entry point into the ETF space but who may be wary of thin margins typical of passive products or having to enhance existing investment strategies to fit a rules-based methodology.

Non-Transparent Products

Beyond passive and active ETF strategies, innovations of the product structure have recently emerged to further blend ETFs with actively managed mutual funds. These new products seek to offer improved performance to investors by capturing the tax efficiency and low-cost features of ETFs with the portfolio disclosure policies typical of mutual funds. Active managers who may not want to publish holdings daily, as active ETFs do, now have an alternative. Proposals from NextShares, Precidian, T Rowe Price, the NYSE, and others are in various stages of approval or review with regulators. Of these, NextShares has gone live, with three exchange-traded managed funds (ETMFs) managed by Eaton Vance currently listed on NASDAQ. These products may provide another avenue for active managers to enter the market and launch products that maintain margin through savings tied to the fund structure, such as lower transfer agency fees, the removal of 12b-1 fees, and lower transaction charges.

SHIFTS IN US DISTRIBUTION

Robo-Platforms

One of the major changes included in the final DOL rule is the expansion of the Best Interest Contract Exemption (BICE) to any retirement plan represented by a retail fiduciary (e.g. bank, insurance carrier, RIA), or a plan with at least USD50 million in AUM. As advisors to these small plans weigh the costs and benefits of the new DOL fiduciary standards to their business models, robo-platforms may see additional flows from retirement advisors.

Robo-platforms have developed effective means of analysing and researching investment products to create asset allocation strategies for investors. Advisors to smaller retirement plans may choose to tap into that research expertise, versus managing their own selection process. This will vary by advisor, but some may see the costs of managing their investment research and selection as a burden given the new rule and will seek to outsource that function to robo-platforms. Today, robo-platforms almost exclusively use ETFs to implement their asset allocation strategies at a significantly reduced advisory fee — even zero advisory fees in some cases. This may also lead to the expansion of new robo-platforms, as intermediary channels like banks and investment consultants seek to protect their own advisory businesses.

Insurance Companies

Finally, given the DOL’s jurisdiction across retirement accounts, ETF usage by institutional buyers like insurance companies will warrant monitoring. Insurance companies have been adding ETFs to their general account allocations and the proposed rule will likely drive increased usage across their Variable Annuity (VA) offerings. Recent Cerulli research has shown that 61 per cent of VA sales were in IRAs, down only 1per cent from the two years prior. And the majority of those sales took place in commission-based accounts — only 4 per cent of recent VA sales have been in fee-based accounts.5

Couple this with the recent shift by the National Association of Insurance Commissioners decision to treat some fixed income ETFs as bonds, and the industry may see both annuity products and insurance general accounts become much larger consumers of ETFs.

Conclusion

It is important to note that the trends we have highlighted here are not a result of the proposed DOL fiduciary rule. Increased usage of low-cost products, desire for fee transparency, active managers entering the ETF market, and the growth of robo-platforms have been underway for years. If approved, the DOL rule should only accelerate the pace of these trends and could propel another USD1.5 trillion into ETFs over the next five years. Although the rule does not go into effect until 1 January, 2018, the industry can expect implementation efforts to begin soon.

Meanwhile, as implementation begins, the industry waits for the other shoe to drop: a potential move by the Securities and Exchange Commission to tighten the fiduciary standards of taxable brokerage accounts, which would present another fundamental shift in how and what investment products are used to manage client assets.

1United States Department of Labor, Fact Sheet: Department of Labor Proposes Rule to Address Conflicts of Interest in Retirement Advice, Saving Middle-Class Families Billions of Dollars Every Year.

2WealthManagement.com, Top Trends in 2016: Part 2 Fees Over Commissions, March 9, 2016.

3ETF.com and Brown Brothers Harriman, US Advisor Survey & European Investor Survey, November 2015.

4Morningstar Direct.

5Investmentnews.com; DOL rule will transform the annuity industry, February 21, 2016.