The two-and-20 fee structure has long been dead. But what’s been slowly replacing it reveals a hedge fund industry splitting into two distinct tiers – and the gap between them is widening.

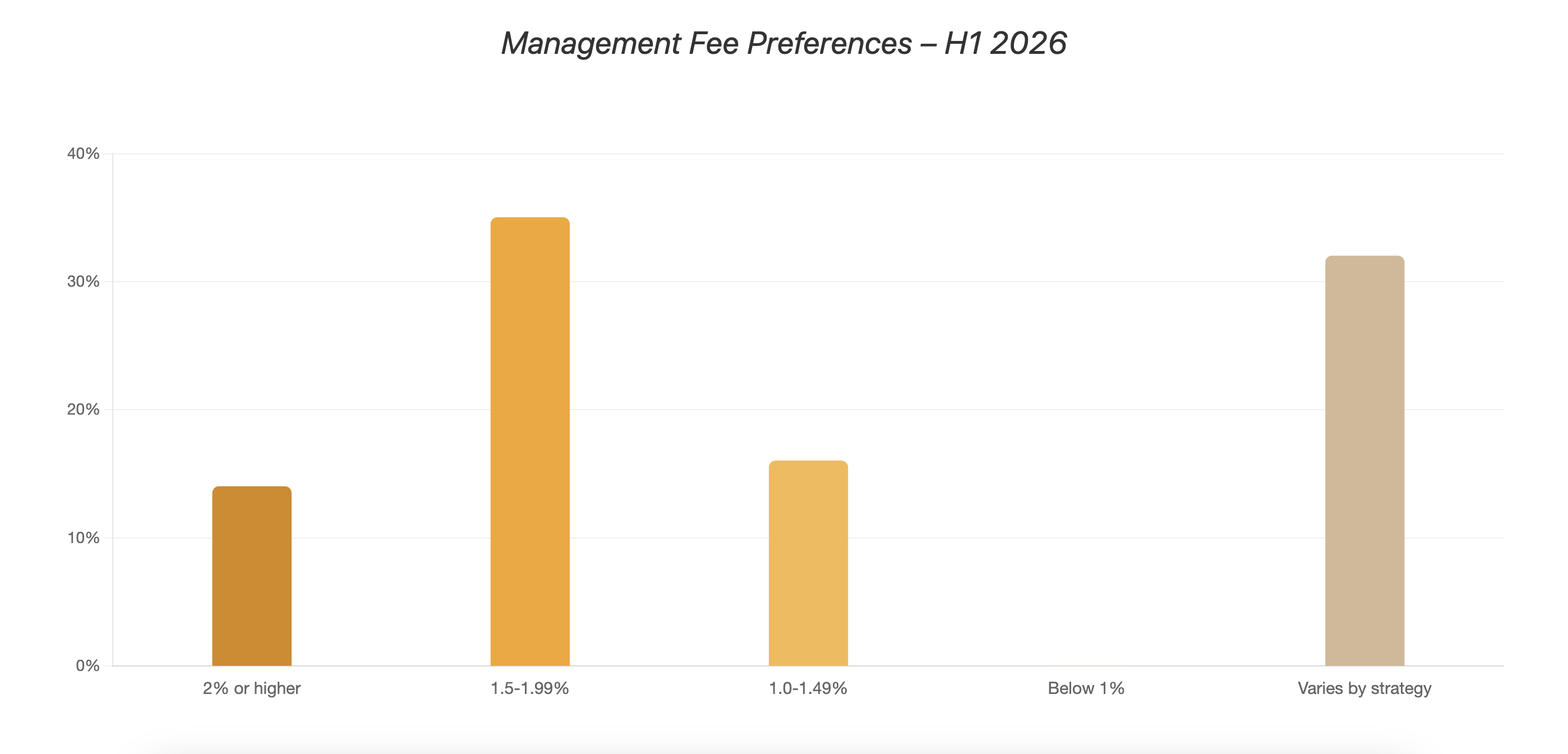

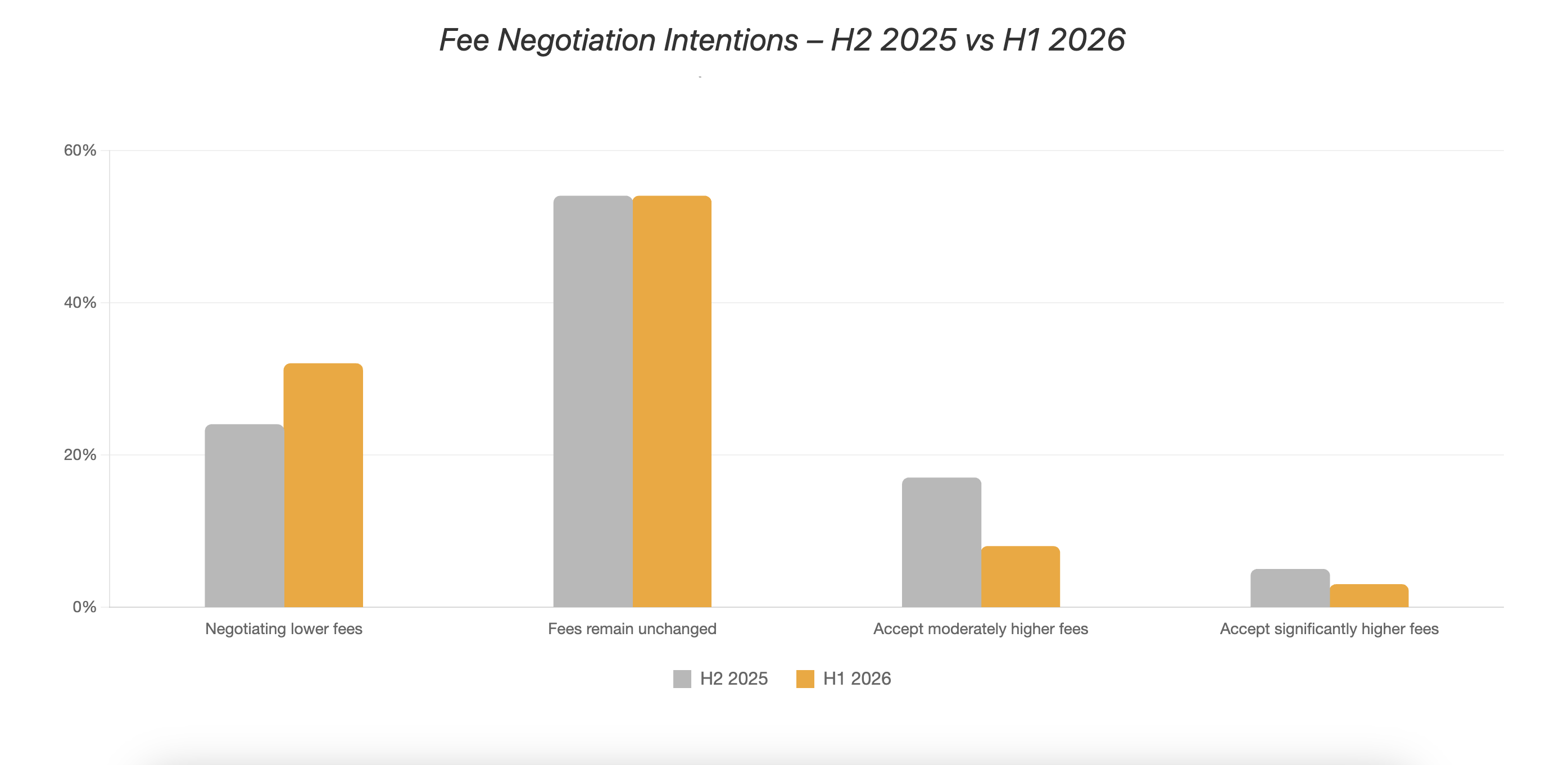

Nearly one-third of hedge fund allocators are now actively negotiating lower fees across their portfolios, up from 24% six months ago, according to the Hedgeweek-AIMA H1 2026 Allocator Survey. More tellingly, preferred management fee bands have shifted decisively downward, with the 1.5-1.99% range jumping from 21% to 35% of preferences.

That 14-percentage point jump suggests 1.5-1.99% is becoming the new industry standard for many strategies.

“Seven or eight years ago AIMA published a report saying the two and 20 was dead, and we maintain that,” notes Tom Kehoe, managing director at AIMA. “Nobody is settling on two and 20 anymore.”

But the story isn’t simple compression. “Investors say they’re prepared to pay, provided who they’re allocating to is delivering on a consistent basis,” Kehoe adds.

And therein lies the bifurcation. At the top end, some platforms made 25% net of fees this year. “Investors will pay 6, 7, 8% in fees if they’re coming out with 20%+ returns,” Kehoe observes.

The bifurcation extends to allocator size. Larger institutions – particularly those with over $5bn in assets – show greater willingness to pay premium fees for differentiated strategies. Fee pressure is most acute among mid-sized allocators.

A pension fund allocator notes fee discussions have become “more nuanced,” focusing on “what you’re actually paying for.” “We’ll pay for genuine alpha, but expect discounts for beta-like exposure.”

The “varies by strategy” preference rising from 27% last year to 32% in 2026 reinforces this split. Truly differentiated strategies can command premium fees. But managers offering replicable strategies face pressure toward 1.5/15 or lower.

This creates a challenge for managers in the middle – those who are good but not exceptional. For them, 1.5/15 isn’t a negotiating position. It’s becoming a ceiling.

The fee dynamics also interact with performance expectations. As allocators explicitly reposition hedge funds as portfolio stabilisers rather than return maximisers – with “expected higher returns” as a rationale collapsing from 56% to 29% – the value proposition shifts.

If allocators aren’t expecting outsized returns, they’re less willing to pay outsized fees. The premium must be justified by genuine uncorrelated alpha, exceptional risk management, or access to capacity-constrained strategies.

Despite strong hedge fund performance in 2025 – averaging approximately 15% net of fees through November – fee pressure hasn’t eased. If anything, success has made allocators more discerning.

The message to managers is stark: demonstrate genuine differentiation, or accept commoditised pricing. There’s no longer a comfortable middle ground where “pretty good” performance justifies premium fees.

For the industry, this represents maturation. Fees now correlate directly with demonstrated value – measured not just in returns, but in risk-adjusted performance, correlation profiles, and downside protection.

The two-tier market is here to stay. The question for each manager is: which tier are you in?

About the data: The Hedgeweek-AIMA H1 2026 Allocator Survey was conducted in November-December 2025 with over 100 institutional allocators globally.