Future economic growth and development in Asia is inextricably tied to the funding of infrastructure projects on the continent at present. In this extract from Preqin Infrastructure Spotlight – June 2015, Oliver Senchal examines the current state of the Asian infrastructure market, detailing fundraising, fund managers, investors and deals in the region.

Unlisted infrastructure fundraising

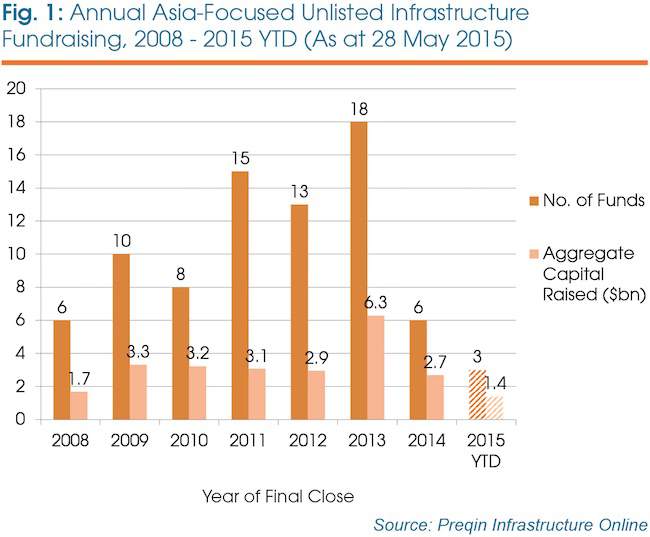

The unlisted infrastructure market in Asia remains a difficult place to raise capital; only six funds closed last year raising an aggregate USD2.7 billion and only three vehicles have held a final close so far this year (Fig 1). At this rate, 2015 is likely to surpass 2014’s total, in line with average aggregate capital raised in the period 2008 to 2012 (USD2.8 billion).

Asia-focused infrastructure funds closed in 2014 raised an average of USD449 million – a seven-year high and a 29 per cent increase on the USD349 million average raised in 2013. As it stands, 2015 is continuing this trend: funds closed so far this year have an average size of USD467 million, a reflection of the increased concentration of capital among a few large managers. Further demonstrating the success that some firms have achieved in the past few years, the proportion of Asia-focused unlisted infrastructure funds closing above their target size has increased from 13 per cent in 2011 to 67 per cent in 2014. Encouragingly, two of the vehicles to have closed so far this year were above target.

With Asia-based infrastructure funds closed since 2008 spending an average of 21 months in market, fundraising can be a lengthy process for many firms. The average time managers spent marketing their offerings reached its peak in 2012 (26 months), although this fell to 23 months for funds closed last year. Funds closed so far this year spent an average of 18 months on the road, with some managers able to quickly attract sufficient capital to reach a final close; one recent example being Singapore-focused Equis Funds Group’s Equis Asia Fund II, which reached a final close in February 2015 having spent just nine months fundraising.

Fund managers

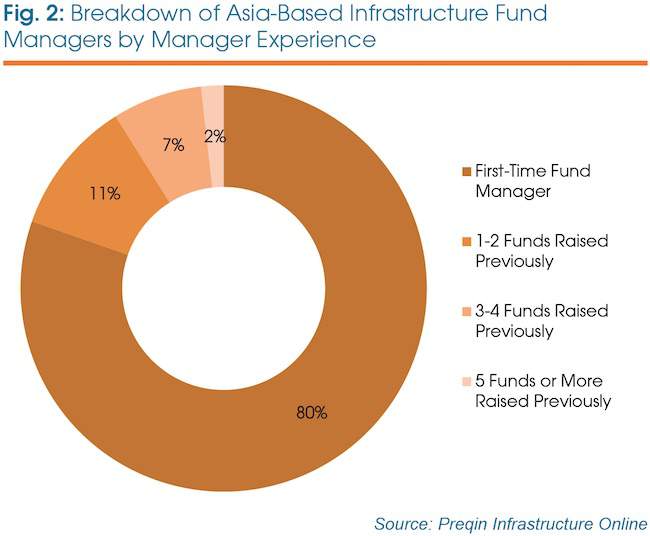

Infrastructure fund managers are often less experienced than those in other asset classes, due to the relatively recent emergence of infrastructure as a distinct asset class. This is particularly true in Asia, where infrastructure as an asset class is even less developed than in Europe or Australasia. As a result, 80 per cent of Asia-headquartered managers are raising their first vehicle (Fig 2), although there is clearly scope for the asset class to develop in the coming years. Additionally, funds focusing primarily on Asia tend to attract smaller amounts of investor capital due to the relative inexperience of the fund managers based in the region; the large majority (69 per cent) have raised less than USD500 million in institutional investor capital.

Preqin’s Infrastructure Online contains detailed profiles for over 55 fund managers headquartered in Asia, including capital raised, available dry powder, strategic and geographic preferences and more. China and India are the investment focus of the largest proportions of Asia-headquartered fund managers; unsurprising due to the large demand for infrastructure in these rapidly developing economies.

Regional infrastructure investment focuses are also targeted by larger proportions; fund managers targeting Asia as a whole and the ASEAN region represent 18 per cent and 11 per cent respectively of the Asia-headquartered fund manager population.

Asian deals

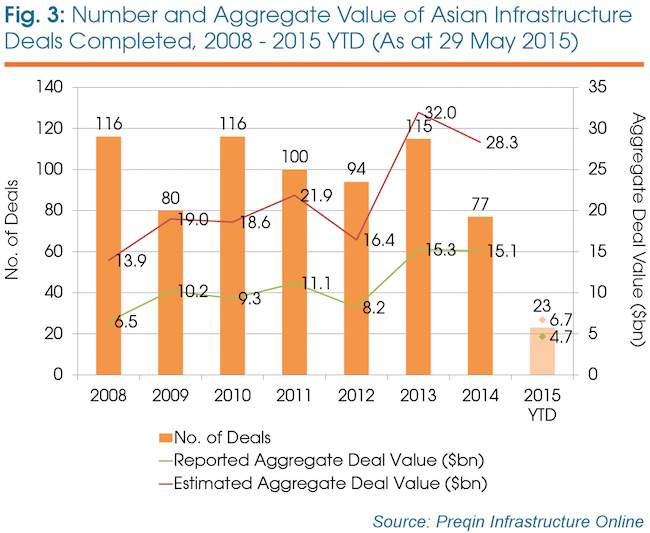

Preqin’s Infrastructure Online service contains details of over 11,200 completed infrastructure deals, including 1,319 involving Asian assets. Extensive profiles for these transactions feature information on deal size, total equity and debt invested, current ownership stakes, service providers and much more. Reported aggregate deal value for Asian infrastructure assets has shown considerable growth in recent years, from USD8.2 billion in 2012 to USD15.3 billion and USD15.1 billion in 2013 and 2014 respectively (Fig 3). While transactions are not quite reaching the peak total values of 2013, deals are increasing in size: the average infrastructure deal size for an Asian asset last year was USD368 million, a 32 per cent increase on 2013.

Asia presents a unique combination of developed and emerging economies, consequently generating many different infrastructure opportunities for a wide spectrum of managers and investors. India has hosted the largest proportion of Asian infrastructure deals since 2010: 30 per cent of transactions have taken place in the country. This is followed by China (16 per cent), Japan (8 per cent), Indonesia (7 per cent) and South Korea (7 per cent) picking up notable proportions of deals since 2010. So far in 2015, 43 per cent of infrastructure transactions have taken place in India, with deals in the Philippines (13 per cent) representing the next largest proportion of all deals in Asia.

Generally, smaller transaction sizes are common for Asian infrastructure assets. Infrastructure deals completed under USD100 million have represented approximately half of all Asian transactions in every year since 2010, and deals under USD500 million have represented 76 per cent to 94 per cent of transactions in the same time period. 2013 and 2014 had the largest proportions of large deals: 11 per cent and 10 per cent respectively of all Asian deals were above USD1 billion in value.

Asia-based investors

Preqin’s Infrastructure Online contains detailed profiles for over 290 Asia-based institutional investors active in infrastructure. Banks and insurance companies are the most prominent type of Asia-based infrastructure investor, comprising 42 per cent of investors in the region. No other investor type comprises over 9 per cent of infrastructure investors based in Asia; prominent investors in other regions, such as pension funds, foundations and endowment plans, make up a combined 15 per cent only. Private wealth is an important aspect of the Asian investor universe, with family offices and wealth managers accounting for 8 per cent of investors in the region.

Japan has the largest number (58) of Asia-based infrastructure investors, also representing the largest assets under management (AUM) of any Asian country with USD8.9tn in aggregate. While China has been active in the infrastructure asset class recently, the country is home to only the fourth largest number of infrastructure investors in Asia (32), although these institutions represent USD6.7tn in aggregate AUM, second only to Japan.

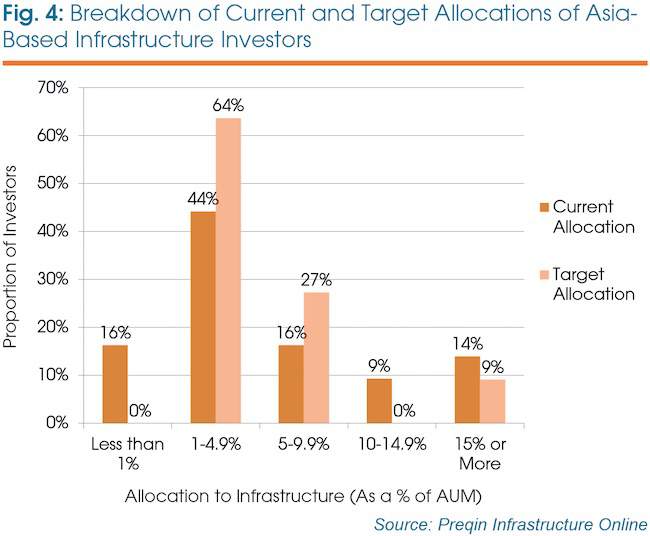

Institutional investors will typically allocate a smaller proportion of AUM to infrastructure when compared to other alternatives. Sixty-per cent of Asia-based investors have a current allocation to infrastructure of less than 5 per cent of AUM, with 16 per cent holding less than 1 per cent in infrastructure (Fig 4). Encouragingly, however, many investors appear to be below their target allocations to the asset class, with 64 per cent targeting 1-4.9 per cent of AUM to infrastructure, and 27 per cent targeting 5-9.9 per cent of AUM to the asset class, suggesting capital is likely to flow into infrastructure in the future.

Outlook

Despite the inception of the Asian Infrastructure Investment Bank (AIIB) by China, and Japan’s further USD110 billion financing of the Asian Development Bank (ADB), there remains a structural financing gap for infrastructure in developing Asian countries. According to the ADB, this gap stands at USD8tn from 2010 to 2020, and without adequate infrastructure Asia’s rising economic growth will be harder to maintain. However, the scale of the challenge facing the continent presents a wealth of infrastructure opportunities for fund managers to access as they try to build up successful track records and attract more institutional capital.

This is an extract from Preqin Infrastructure Spotlight – June 2015, which also looks at the top 100 investors in infrastructure and brings you the latest Preqin infrastructure data. Read the full newsletter here for free.