The amount of capital awarded by investors to separate account structures reached an all-time high in 2014. In an extract from Preqin Real Estate Spotlight – June 2015, Oliver Senchal examines the growing prominence of this type of alternative structure in the broader fundraising market, including investor appetite and fund manager plans.

Growing prominence

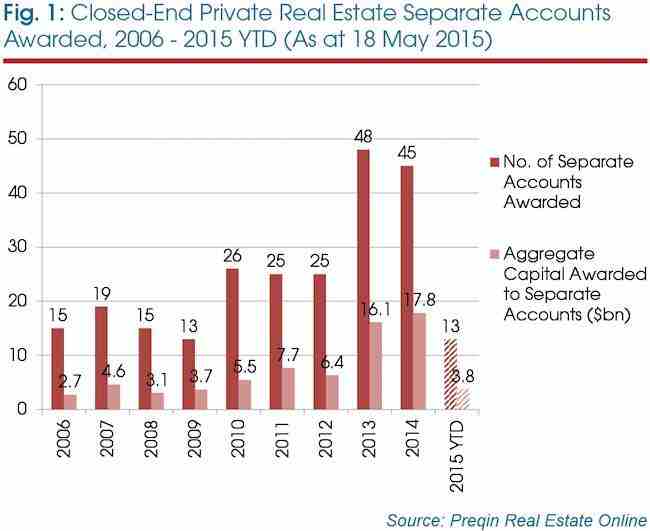

Preqin’s Real Estate Online contains detailed information on over 300 real estate separate account structures. As Fig 1 displays, the aggregate value of separate accounts awarded in a single year between 2006 and 2012 never exceeded the USD7.7 billion awarded in 2011. While 2013 represented a peak in the number of separate account mandates, 2014 was an all-time high in terms of the amount of capital committed to these structures (USD17.8 billion).

It is only since 2013 that separate accounts have begun to constitute a sizeable proportion of overall private real estate fundraising, both in terms of number and aggregate value. Between 2006 and 2012 separate accounts accounted for 8 per cent of the total number of funds and 7 per cent of the total capital raised, while since 2013 that average has reached 22 per cent of the number and 15 per cent of the aggregate capital. Even with only 13 separate account mandates awarded so far this year, this still represents over a quarter of all vehicles closed in 2015, indicative of the growing prominence of separate accounts in the industry.

Strategy, geography and property types

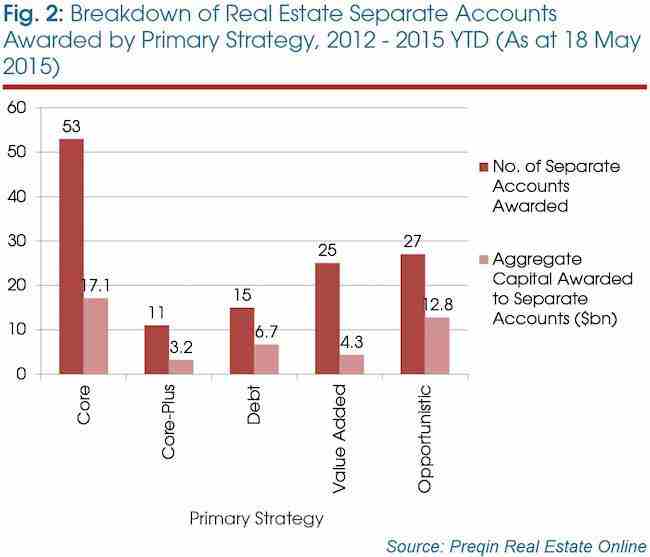

Vehicles targeting core real estate secured the highest proportion of mandates (40 per cent) and the highest proportion of separate account capital (39 per cent) in the period 2012 to present (Fig 2). It is perhaps unsurprising that core accounts have gained the most traction; the approach can offer a good option for investors to place large amounts of capital in stable, income-producing assets. Higher risk strategies are also widely utilised however, with the amount of capital allocated to value added and opportunistic accounts combined equalling that of core accounts (USD17.1 billion).

Since 2012, half of all separate accounts have been primarily US-focused, followed by Europe (30 per cent) and Asia-Pacific (13 per cent). The proportion of total separate account capital follows a similar trend, with US-, Europe- and Asia-Pacific-focused accounts collecting 43 per cent, 34 per cent and 19 per cent of the total capital respectively. Regarding primary property focus, diversified (30 per cent), residential (23 per cent), office (17 per cent) and industrial properties (16 per cent) were awarded the highest proportions of mandates. However, industrial-focused separate accounts accumulated the largest proportion of aggregate capital since 2012 (36 per cent), higher than office- and residential-focused mandates collectively and nine percentage points higher than the proportion of capital collected by diversified mandates.

Size of separate accounts

Nearly half of all real estate separate accounts awarded since 2012 have been less than USD250 million in size, and three-quarters have been smaller than USD500 million. Nevertheless, mandates awarded for over USD1 billion contributed the highest proportion (28 per cent) of total separate account capital, even though only 10 vehicles were formed in the time period. The largest real estate separate account formed since 2014 is Goodman China Logistics Holding, a partnership between Goodman and CPP Investment Board (CPPIB), which invests in logistics properties in China. The largest separate account formed in 2015 so far is Pacific Multifamily Investors, a partnership between Pacific Urban Residential and California Public Employees’ Retirement System (CalPERS). The vehicle was funded with an initial USD200 million allocation from CalPERS, which rose to a total commitment size of USD650 million in February 2015. The vehicle focuses on the acquisition of income-producing, institutional-quality multi-family real estate, targeting major markets in the Western US region.

Investors in separate accounts

Preqin’s Real Estate Online contains extensive profiles for more than 280 institutional investors with a preference for investing through separate accounts. These investors have average assets under management (AUM) of USD53 billion, which compares to USD20 billion for all investors. In addition, the separate account investors have higher average current and target allocations to real estate than for the whole investor universe: 10.2 per cent and 10.9 per cent respectively compared to 8.7 per cent and 10.3 per cent for all investors.

Separate accounts have often been the preserve of the larger investors that are likely to have the large commitment sizes necessary to form these relationships, along with the internal resource and knowledge required to invest through these structures, which may require more extensive due diligence, and the ability and resources to monitor and make decisions on an asset level. Of real estate investors with more than USD10 billion in assets, 52 per cent will invest through separate account structures, with this figure rising to 65 per cent for investors with assets greater than USD50 billion. Comparatively, only 19 per cent of investors with less than USD10 billion in AUM will consider separate accounts.

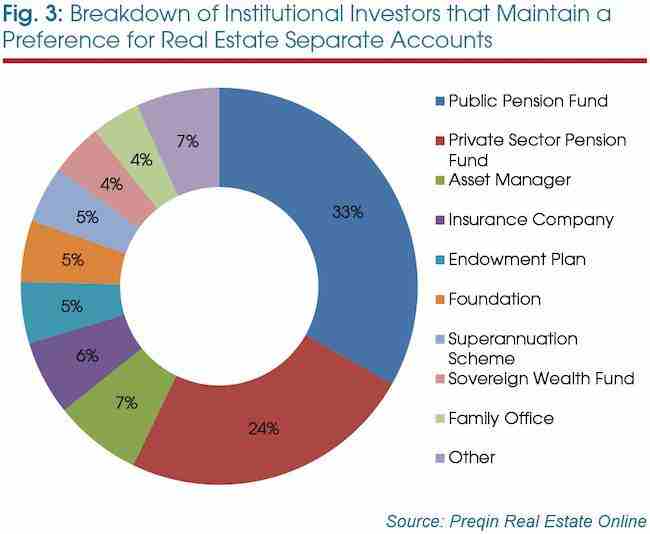

Pension funds make up the majority of investors that have a preference for separate account structures (Fig 3), with many pension funds having the resource available for separate account investments. Sovereign wealth funds, while relatively few in number, are likely to target separate accounts, with 80 per cent utilising this route to market.

Growing appetite for separate accounts

The increase in number and capital awarded to separate accounts has been driven by a steady increase in investor appetite. As detailed in the Preqin Investor Outlook: Alternative Assets, H1 2015, 29 per cent of investors will invest in separate account structures in the next 12 months (as of Q4 2014), with a further 11 per cent considering making their maiden commitment (Fig 4). This represents a seven percentage point increase in the proportion of investors investing or considering investing in separate accounts from Q4 2011. While the proportional increase appears modest, as discussed previously, the size of investors participating in these alternative structures means large amounts of capital are flowing into the real estate asset class.

Outlook

Separate accounts can offer many advantages to both investors and fund managers over commingled real estate vehicles. From an investor’s perspective, separate accounts offer greater control over their real estate investment programs, a higher level of exposure to desired assets, more favourable fees and other terms, and the ability to put large sums of capital to work. Fund managers, meanwhile, build closer relationships and gain large commitments from some of the world’s biggest investors, which may outweigh the potential reduction in fee income when compared to a pooled fund.

Sizeable separate account mandates represent a change in the way large investors are utilising their size to put large amounts of capital to work, gain greater control of investment decisions and negotiate better terms. Separate account structures are likely to continue to grow in prominence with rising investor appetite and fund managers responding by offering more separate accounts to investors. As separate accounts become more widespread, they will constitute growing proportions of many investors’ overall real estate portfolios. However, given the additional resources required, separate accounts are likely to remain the preserve of the largest investors in the asset class.

This is an extract from the Preqin Real Estate Spotlight – June 2015. To read the full spotlight, also looking at niche property fundraising and the Canadian private real estate market, click here.