Sub-Saharan Africa is a rapidly growing investment theme and its dynamics will increasingly impact on both Developed and other Emerging Markets. The region is particularly interesting to investors on account of both the demographics, the rate of change of the markets and the low correlation with Developed and Emerging Markets. The May 2000 cover of The Economist carried a picture of Africa titled 'The Hopelesss Continent'. In March 2013 that changed to 'Africa Rising' with a feature concluding that the reforms and investment would soon bear fruit. The time is now as the investment is increasingly coming from International investors and with it the technology and transparency of dealing in the markets. Sub-Sahara Africa (SSA) is going 'mainstream'.

Sub-Saharan Africa is defined in investment terms to exclude the Arab countries of the Middle East and North Africa (MENA) which have more developed markets with their own dynamics after the 'Arab Spring'. 'Pure SSA' is normally taken to exclude South Africa, which dwarfs the rest of the region with an equity market capitalisation nearly three times its GDP. Nigeria, whose economy overtook South Africa last year to become the biggest in Africa at USD500bn, has an equity market of only 20% of its GDP. Ghana is 7%, Kenya is 40% and the global average is 87%. There is plenty of 'room to boom'.

The GDP growth rates in SSA are exceptional as seven of the world's ten fastest growing economies are in SSA (IMF). Clearly it’s easier to move that needle from a low base (as per the debate on Chinese growth at the other end of the spectrum), but that only supports the momentum argument. Furthermore the diversification of that economic growth is pronounced, with Nigeria deriving 80% government revenues from oil whilst Kenya has a consumer-driven economy which has seen the equity market mimic the linear ascent of the S&P in recent years. Low oil prices benefit the East and Southern Africa economies, which are all fuel importers.

In 2012 there were an estimated 800 million people living in SSA. The IMF forecast that to more than double to 1.7 billion by 2050. Africa is the second biggest continent in both land mass and population. Half of those people are under 20 years old, compare that to the ageing population in developed countries. With labour costs 2-10% of European, US and Japanese rates, that will help drive increases in productivity.

Key metrics including life expectancy, literacy, GDP-per-capita rates, economic freedom, corruption metrics, conflict and levels of urbanisation are all improving. Clearly these have not had a uniform basis-change across all of Africa's 53 nations, as corruption is still a major problem and violence touches too many lives. However more and more countries are successfully making the transition from authoritarian regimes to stable democracies. 30 ruling parties or leaders have been democratically removed by voters from 1991-2011, compared to only 1 peaceful transition of power from 1960-91.

Investment in SSA is happening internally and externally. Foreign Direct Investment flows (not aid) have had a bigger impact on financing strong growth with $54bn in 2015 ($37bn in 2012), growing faster than any other region in the world. Debt Markets have developed substantially to finance much investment across the continent. The banking sector is particularly developed in Nigeria and Kenya.

Infrastructure projects from Private Equity Funds funded by Sovereign Wealth Funds, DFI’s and Pension Funds have improved Power & Generation, transport and telecoms networks, but much more is needed. International investors are increasing allocations to equities. A few years ago that investor base was 40% US, 40% European and 20% South African. Now it is increasingly about the US investor as reforms are implemented. SSA ex-SA is estimated to be 15-20% of the Frontier Markets arena and both US Hedge Funds and Pension Funds are building positions in anticipation of the 'next China or India'. The low Debt to GDP ratios of the Frontier Africa countries are increasingly attractive. SSA Equities averaged across countries are one of the few areas where prices are still lower than the 2008 peak, yet earnings are higher.

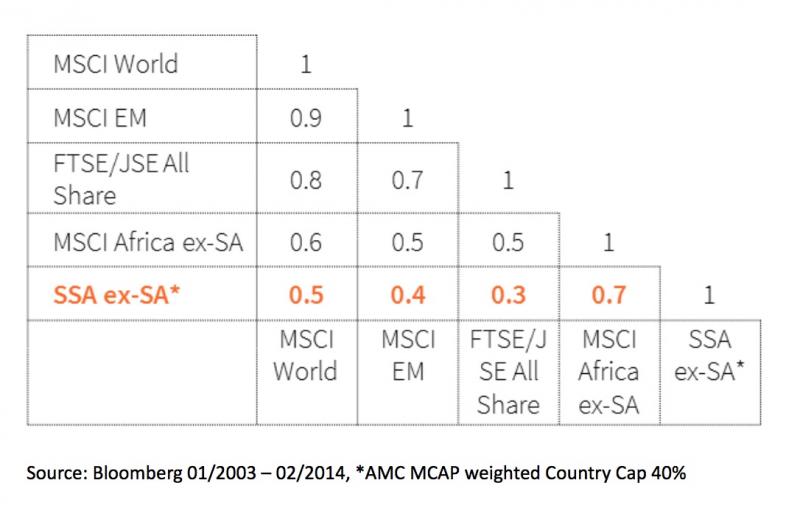

The low correlation between SSA equities and other regions helps fund managers reduce volatility of returns and increases the potential investor pool.

Access to the equity markets is non-trivial. There are 29 exchanges (including the BVRM with the 'Francophone 8' French-speaking countries of West Africa). Custody is difficult in several countries and it is not possible to borrow or short stocks. FX hedging can be cumbersome. Investors have historically had the choice between a handful of funds and a few ETFs which in particular tend to have a disproportionately large weighting to South African or MENA equities where volumes are more easily achieved for the manager, but obviously don't reflect 'pure SSA'.

Whilst the opportunity for meaningful growth in the Sub-Sahara ex-SA public equity markets is significant, it is not a market for novices and it is best navigated in partnership with an experienced investment team with a strong track record and a good understanding of the distinct nuances of the economic and business environment of each country in the Frontier Africa markets.