The hedge fund industry’s narrative around democratised technology suggests smaller managers should now compete on equal footing with established giants. Allocators aren’t buying it, and their cheque-writing behaviour proves the point.

According to our latest hedge fund allocator survey, 45% of allocators acknowledge that smaller managers now offer technology capabilities comparable to large institutions. Cloud-based systems, institutional-grade analytics and sophisticated compliance tools that once required massive capital outlays are available on subscription. The technological moat has been filled.

But here’s where theory meets reality: amongst managers themselves, only 45% report that improved technology has meaningfully narrowed the capability gap with the largest asset managers over the past 18-24 months. Just 27% say winning new institutional mandates has become easier, whilst 63% report fundraising remains as tricky as it was 18 months ago. Another 10% find it more challenging than ever before.

“The technology conversation is largely a red herring,” says a chief investment officer at a European pension fund, speaking on background. “We expect managers of any size to have proper systems. What we’re evaluating is whether they can generate genuine alpha. The operational infrastructure is table stakes, not a reason to allocate.”

This is the uncomfortable truth emerging from the data: operational competence has become an entry requirement rather than a competitive advantage. Allocators now assume emerging managers will demonstrate technological sophistication. They simply don’t reward it with faster capital deployment.

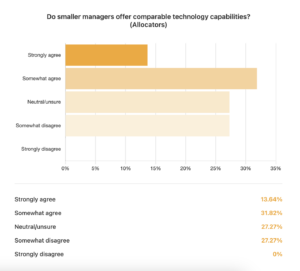

The perception gap matters too. Whilst some allocators acknowledge technological convergence, more than a quarter remain neutral or unsure whether smaller managers truly match larger peers’ capabilities. Another 27% actively disagree with the premise. Even as managers invest heavily in their technology stacks, allocators question whether these improvements translate into genuine operational parity.

The fundraising environment’s resistance to change reflects deeper structural realities that technology cannot address. Institutional allocators prioritise organisational stability, team depth and track record longevity. These attributes remain closely correlated with scale and tenure. A sophisticated risk management system doesn’t substitute for a chief risk officer with two decades’ experience, nor do automated workflows replace the institutional memory of a firm that has navigated multiple market cycles.

The data suggests managers may be solving the wrong problem. They’ve invested in closing the technology gap, whilst allocators have moved on to evaluating what that technology enables: consistent alpha generation, robust risk management in stressed markets, and the kind of organisational resilience that only comes with time.

For emerging managers, the implications are stark. Technological sophistication is necessary but insufficient. The capital allocation decision still hinges on investment performance, team quality, and institutional credibility. These factors remain frustratingly resistant to technological shortcuts. The technology gap may be narrowing, but the trust gap persists.