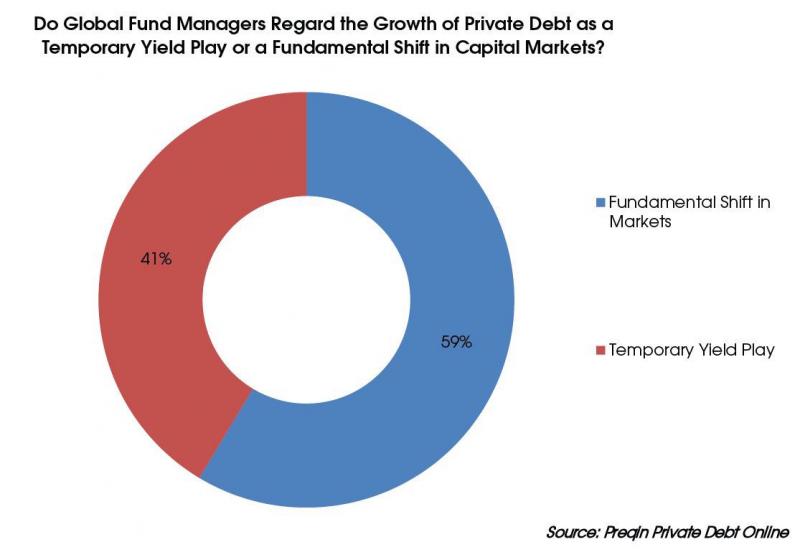

In the midst of a shifting market environment, alternative fund managers are experiencing a surge of demand for primary financing activity. The increasing demand for private debt investment products and, as a result, the increase in private debt holdings, has raised questions as to whether we are seeing a fundamental shift in markets, or if this is a temporary yield play. A temporary yield play can be defined as a short-term strategy employed by fund managers to generate profit for clients, with no plans to extend the strategy past a short-term view.

Preqin’s recent global private debt fund manager survey reveals that 59% of respondents have acknowledged a fundamental shift in this space. With the regulatory environment constricting bank lending activity, a gap has emerged in the market for loans, creating additional opportunities for private debt firms. Preqin interviews and survey data suggests this evolution of the lending industry will see the use of private funds fuel additional economic growth, in tandem with private equity and corporate bonds. The increased role of regulators has helped to define, and has provided the structure for, private debt funds, enabling them to have a broader appeal and larger scale. The growth of outsourcing and transparency in the space has made these funds an attractive option for investors, with the ability to limit downside risk. The evolution of the alternative asset management industry has created an instrument that could be primed to fill the private debt space by using the private equity model, and has the potential to act as a fixed income alternative for institutional portfolios. As a result, the markets continue to rebalance as lending regulations on banks and their disintermediation takes hold, allowing for the growth of this new asset class.

Another scenario revolves around the idea that the increase in assets committed to private debt investments is a result of a temporary yield play. Together with the federal banks holding low-yield environments and fund managers’ strong balance sheets, many view the recent activity as a temporary move. Given that these types of funds can offer attractive risk-adjusted returns, capital may be attracted to the space for the short-term profit opportunity rather than a long-term view of viability for private debt.

An area once dominated solely by banks, the private debt space is now shared with fund managers, backed by ample investor capital. A tangible shift in capital market activity has occurred, with regulatory directives suggesting a shift in favour of a more transparent lending model, leading to an increase in fund manager activity within primary financing.

Ron Wexler

Click here to find out more about Preqin’s Private Debt Online service.