In an extract from the Preqin Hedge Fund Spotlight | May 2015, Joseph McGee takes a look at the ‘USD1bn Club’, a group of the world’s largest hedge fund managers, and identifies the traits and characteristics that are unique to this distinguished group which controls a vast proportion of industry capital.

Over the past year, hedge fund industry assets have increased, surpassing the USD3tn mark as of December 2014. One notable group active in this space is managers with at least USD1bn in assets under management (AUM) – the ‘USD1bn Club’ – comprised of some of the largest hedge fund managers in the world. Being in the Club captures the attention of many institutional investors, but is no easy feat; many have steadily grown their assets over many years, withstanding both turbulent and stagnant periods and delivering returns to investors. New entrants to the Club have demonstrated superior performance to accumulate their assets or have shown credentials from previous firms to attract large amounts of capital.

Preqin’s Hedge Fund Analyst shows that there are currently over 570 managers worldwide with at least USD1bn in hedge fund AUM, an increase of 63 managers from last year, representing a significant proportion (92%) of total industry capital. Here, we take a look at the USD1bn Club of hedge fund managers and identify the characteristics and attributes of what it takes to reach, and remain at, the top of the hedge fund industry.

The Composition of the USD1bn Club

The recent growth in industry assets has been particularly noticeable among the largest hedge fund managers. Several of the top 10 largest managers by AUM have experienced significant changes in AUM over the past 12 months. Bridgewater Associates is currently the largest hedge fund manager globally and increased its assets from over USD154bn in March 2014 to almost USD170bn in March 2015. Among other leading managers, the biggest mover was Man Investments, where a number of major acquisitions such as Numeric Investors (in June 2014) and NewSmith (February 2015) boosted the firm’s hedge fund assets from just over USD28bn in March 2014 to USD50bn in March 2015. Not all managers have seen assets increase however, such as BlueCrest Capital which fell out of the USD20bn+ bracket, partly due to spinning out its BlueTrend funds as Systematica Investments in January 2015.

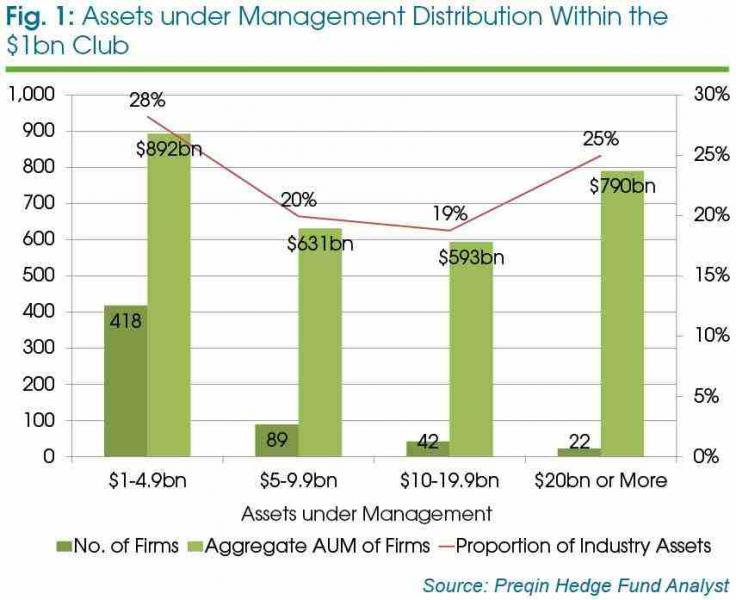

In order to get a more complete picture of the USD1bn Club, it is necessary to look closer at its overall composition, both in terms of membership and strategies. Fig. 1 shows how assets are distributed between the larger and smaller members of the USD1bn Club. The vast majority of members manage between USD1bn and USD4.9bn, while on the larger end of the scale, 22 firms manage over USD20bn in hedge fund assets. Aggregate capital is heavily distributed at each end of the scale: firms in the USD1-4.9bn category have USD892bn in aggregate assets under management (28% of the industry) and firms managing over USD20bn have USD790bn (25%). The median assets under management for a USD1bn Club firm is USD2.4bn, reflecting the heavy concentration of firms in the USD1-4.9bn segment.

Strategy Preferences of the USD1bn Club

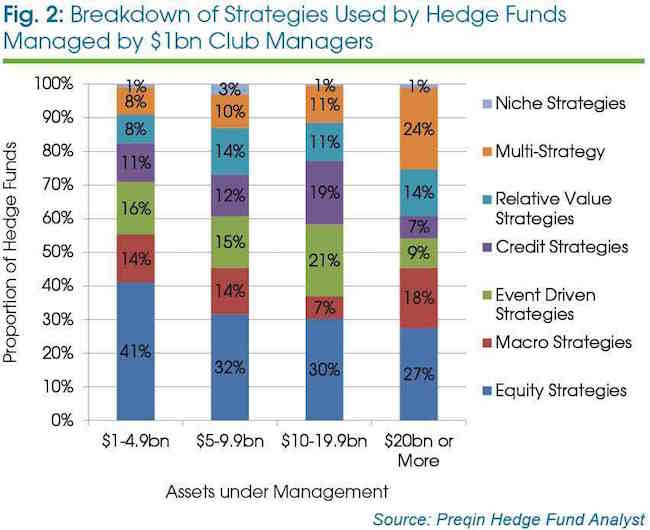

There are also significant differences within the USD1bn Club between the larger and smaller fund managers in terms of the range and number of strategies they employ. Smaller managers in the Club are more likely to offer equity strategies (as shown in Fig. 2) than all other AUM segments. This may reflect the difficulties in scaling core equity strategies funds without affecting performance.

Macro strategies and multi-strategy hedge funds are more common among the offerings of the largest fund managers. Eighteen percent of funds offered by managers with over USD20bn in AUM employ macro strategies. Multi-strategy funds have become more prominent among firms with over USD20bn, rising to 24% of funds from 20% last year. This in part can be explained by investor interest in the strategy’s recent performance: in the 12 months to April 2015, the Preqin Multi-Strategy benchmark gained 8.47%, compared with 7.20% for all hedge funds.

Furthermore, larger hedge fund managers tend to have the infrastructure and internal resource to construct more complex and multi-layered strategies. With the expertise and experience in the space, such managers can profit from utilizing a multi-strategy approach that can provide further diversification within a single-manager structure, offer more scope to generate absolute returns and reflect the greater scalability of these funds. The model of multi-strategy investing is followed by firms such as Millennium Management, where capital is allocated across a range of separate trading teams with centralized risk controls, reducing the reliance on a single strategy to produce consistent returns and also reducing the risk of concentrated positions moving markets.

The largest fund managers are more likely to offer a range of strategies to their investors, and this can play a key part in providing managers with the consistency of performance that allows them to grow their assets. Forty-one percent of managers with over USD20bn in assets offered four or more strategies, compared to only 11% of managers with USD1-4.9bn in assets. By contrast, over half of fund managers with USD1-4.9bn in assets only offered a single core strategy to their investors.

Previous Experience and Age Help to Break into USD1bn Club

A number of new firms launched over the past year have reached USD1bn or more in assets. 2014 saw the likes of Darsana Capital Partners, Finepoint Capital, Hitchwood Capital Management, Shellback Capital, Three Bays Capital, Thunderbird Partners and Two Creeks Capital Management all launch debut funds that have grown to over USD1bn in AUM. A number of firms are reported to be targeting a similar result in 2015, including former Brevan Howard partner Chris Rokos’s Rokos Capital Management and former Eton Park Capital Management partner Isaac Corre’s Governors Lane. A common feature of all of these new launches is that the founders were all senior employees at other USD1bn Club hedge fund firms, suggesting the importance that investors attach to a background at a leading firm. In some cases, such as ex-Ziff Brothers employee David Fear’s Thunderbird Partners, the managers were able to attract the backing of their former employers, which can help accelerate the growth of assets in a firm’s early stages.

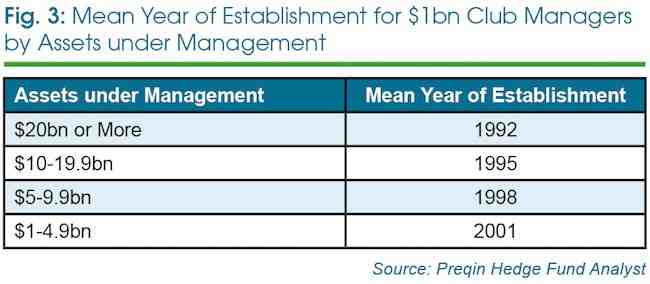

The two largest recent launches were both spinouts from other USD1bn Club firms: Systematica Investments taking control of funds it had managed for BlueCrest Capital with USD8.5bn in assets, and DW Partners leaving Brevan Howard Capital Management with USD6bn. While spinning out allows fund managers to bring a track record and some of their existing assets to the new firm, even these managers will likely require more time to become one of the largest firms. As Fig. 3 shows, the largest firms are on average several years older than smaller firms in the USD1bn Club. The series of recent fund launches in the USD1-4.9bn category means that the age difference between the largest and smallest firms is increasing. The mean year of establishment for firms with USD1-4.9bn in assets changed to 2001 from 1997 last year, reflecting an increase in new fund managers breaking into this category. By contrast, the mean year of establishment for firms with over USD20bn in assets changed to 1992 from 1991 over the same period.

New York and London Accommodate the Concentration of USD1bn Club Managers

Even as the overall membership and assets managed by the USD1bn Club have grown, there has been a notable concentration of members in the two financial centres of New York and London. New York in particular has seen the number of hedge fund managers with at least USD1bn in assets increase from 174 to 202 last year, while the combined assets managed by these firms has increased from USD938bn to USD1,052bn. The number of firms with at least USD1bn in assets has also grown in London, from 80 last year to 83 at present, representing an increase from USD346bn to USD363bn in aggregate AUM over the same period.

Connecticut is home to 38 hedge fund firms in the USD1bn Club, totalling USD407bn in AUM, up from USD400bn last year. The proximity of towns in this state, such as Greenwich and Westport, to the financial hub of New York, combined with the state’s historically lower tax rates, has made this an attractive destination for hedge fund managers. The presence of several of the largest managers in Fig. 1, such as Bridgewater Associates (USD170bn), AQR Capital (USD65bn), Viking Global Investors (USD30bn) and Lone Pine Capital (USD29bn) help explain the high density of AUM in the state.

The USD1bn Club remains overwhelmingly concentrated in North America, with 380 fund managers managing USD2,136bn in this region. This is followed by Europe, which accommodates 130 fund managers in the USD1bn Club and manages a total of USD598bn. Fewer members are based in the Asia-Pacific (45) and Rest of World (16) regions, managing an aggregate USD121bn and USD51bn in assets respectively. Asia-Pacific also has the lowest average AUM per fund manager at USD2.7bn, reflecting the challenges of raising assets even for the largest fund managers in this location. Members of the USD1bn Club are spread over 31 countries worldwide, an increase on 25 last year, showing the increasing dispersion of some of the largest fund managers in the world.

Outlook

The USD1bn Club is a notable group of hedge fund managers with a set of unique and desirable characteristics that make them some of the most prominent managers in the industry today, and who will continue to attract the attention of investors in the space. Even within this group, however, there are significant differences between the larger and smaller fund managers. The largest fund managers are more likely to offer a range of core strategies and show a preference for multi-strategy and macro strategy funds. All USD1bn Club firms are concentrated in the main hedge fund centres of New York and London, with a large proportion hailing from North America as a whole.

USD1bn Club members are also likely to be older or at least able to clearly demonstrate a strong track record at a previous firm, showing their ability to navigate through various market cycles and periods in the effort to attract and retain investor capital, as was the case for some new entrants.

This is an extract from the Preqin Hedge Fund Spotlight | May 2015. To read the full spotlight newsletter, containing performance benchmarks, industry news and more, click here.